The Influence of Attitudes, Perception of Control and Internal Control System on Whistleblowing Intention with Legal Protection as a Moderation Variable (study on PT Kereta API Indonesia)

Dona Primasari

Jenderal Soedirman University, Indonesia

E-mail: dona.primasari@unsoed.ac.id

ORCID iD: https://orcid.org/0000-0003-0519-1451

Lego

Waspodo

Lampung University, Indonesia

E-mail: legowaspodo@yahoo.com

Muhammad Thareq Ilhami

KAP Kanaka Puradiredja Suhartono

(Nexia KPS) Public Accounting Firm, Indonesia

E-mail: thareqilhami@gmail.com

Annotation. This study aims to determine, analyze, and test the effect of attitudes, perceptions of control, and internal control systems on whistleblowing intentions with legal protection as a moderating variable. This type of research is survey research with a quantitative approach. The population in this study were employees who worked at PT Kereta Api Indonesia Daop 5 Purwokerto. The sample selection used purposive sampling method. The results of this study indicate that: 1) Attitude has a significant effect on the intention to take whistleblowing action. 2) Perceived control has no effect on the intention to take whistleblowing action on employees PT Kereta Api Indonesia Daop 5. 3) The internal control system has no effect on the intention to take whistleblowing action. 4) Legal protection cannot moderate the effect of attitudes on intentions to take whistleblowing actions. 5) Legal protection cannot moderate the influence of perceptions of control on the intention to take whistleblowing actions. 6) Legal protection cannot moderate the influence of the internal control system on the intention to take whistleblowing action.

Keywords: Attitude, Perceived Control, Internal Control System, Whistleblowing Intention, Legal Protection.

JEL Code: M41, M42,D22

Copyright © 2022 Dona

Primasari, Lego Wasapodo, Muhammad Thareq Ilhami. Published by Vilnius University Press. This is

an Open Access article distributed under the terms of the Creative Commons

Attribution Licence, which permits unrestricted use, distribution, and

reproduction in any medium, provided the original author and source are

credited.

Submitted on

14.12.2022

Introduction

A whistleblower is a prosocial behavior that is useful for helping other parties in making an organization or company healthy. Whistleblowers have certain motivations to disclose facts, such as religiosity, wanting to help organizations from losses, and creating a good organizational environment and culture. Although it cannot be denied that individual interests play a role in strengthening the reasons for prospective whistleblowers to disclose cases of fraud (Sagara, 2013). The whistleblower phenomenon arises when there are reports from employees who are suspected of making mistakes at work that need to be followed up by making disclosures in the public interest.

Individuals to become a whistleblower is not an easy thing. In general, someone who comes from an internal organization will face an ethical dilemma in deciding whether to disclose fraud or let it remain hidden. Some people view whistleblowers as traitors who violate organizational loyalty and norms, others view whistleblowers as heroic protectors because they are considered to have done extraordinary things, to prevent even greater losses. (Rothschild, Miethe, 1999). Such a view influences potential whistleblowers in a dilemma and hesitates in choosing an attitude which results in reducing the intention to take whistleblowing action (Bagustianto, 2015). Efforts need to be made to overcome these views and stigma, namely by creating a whistleblowing system that functions to assist individuals in disclosing fraud.

Fraud cases at PT Kereta Api Indonesia indicates that organizational management is still a mess and needs to be fixed in order to avoid similar incidents. Therefore, it is necessary to have a whistleblower to assist companies in disclosing cases of fraud within the company. PT Kereta Api Indonesia as a State-Owned Enterprise (BUMN) has implemented a whistleblowing system based on Minister of BUMN Regulation PER-13/MBU/10/2015 dated 08 October 2015 concerning guidelines for managing the reporting system for alleged violations in companies belonging to the Ministry of BUMN.

This study aims to try to reduce the errors of previous observations through research design to arrive at new conclusions. This research will also explore the whistleblowing phenomenon by measuring a person's intention to act whistleblowing, as well as solving, explaining and predicting the meaning of problems in whistleblowing behavior and then concluding whether the phenomenon can be controlled through several interventions or not. So that solutions and suggestions, both practical and theoretical, will be useful in the development of whistleblowing, especially at PT Kereta Api Indonesia.

This research uses Theory of Planned Behavior (TPB) which is a development of Theory of Reasoned Action (TRA) initiated by Fishbein and Ajzen in 1975. TRA explains that a person's intention towards behavior is formed by two main factors: subjective norms and attitudes toward behavior. Whereas in TPB one more factor is added, namely perception of behavior control (Ajzen, 2010). Ajzen says TPB has been widely accepted as a tool for analyzing the difference between attitudes and intentions and as intentions and behavior. Theory of Planned Behavior explains that the intention to behave in an individual is influenced by individual factors and situational factors.

1. Literature review and hypothesis development

1.1 Literature review

Theory of Planned Behavior. Theory of Planned Behavior (TPB) is a development of Theory of Reasoned Action (TRA) which was put forward by Fishbein and Ajzen in 1975. Ajzen's said TPB has been widely accepted as a tool for analyzing differences between attitudes and intentions as well as intentions and behavior. Whistleblowing research based on the Theory of Planned Behavior has been previously used by Park and Blekinsopp (2009) in their research entitled “Whistleblowing as planned behavior – A survey of South Korean police officers” conducting tests to determine whether TPB can be used as a model and is suitable to be applied to explain whistleblowing intentions. The conclusion in this study is that TPB explains that attitudes, perceptions of control, and subjective norms together form individual intentions and behaviors to become whistleblowers.

Whistleblowing. Whistleblower is an employee or community member who reports fraudulent practices that occur within the company or government, where the report is expressed directly by internal parties or external parties who are aware of fraudulent practices (Susmanschi, 2012).

Attitude. Attitude according to Park, Blenkinsopp (2009) explains the number of beliefs an individual has about the consequences of whistleblowing, the individual will evaluate the action as favorable or unfavorable. So that individuals who have decided to become a whistleblower have a certain amount of confidence that a whistleblowing action is an action that has positive consequences. Saud (2016) in his research shows that attitude has a significant positive effect on whistleblowing intentions. This means that individuals have positive beliefs about the act of reporting fraud so that these individuals tend to react with a positive attitude. Damayanthi, Sujana, Herawati 's (2017) research is also in line with stating that there is a positive influence between attitudes on a person's intention to do whistleblowing. Meanwhile, in the research conducted by Mayasari, Setiyanto, Irawati (2018) and Suryono, Chariri (2016) it was stated that there was no influence on attitudes towards intentions by individuals to carry out whistleblowing.

Perception of Control. Ajzen (1991) explains that perception control is a control over behavior that is generated by the individual's perception of the behavior to be performed, because the individual feels very confident that he has his own control over the perception of that behavior. Damayanthi, Sujana, Herawati (2017) revealed that the perception of control has a positive and significant influence on the intention to do whistleblowing. In Mayasari, Setiyanto, Irawati's research (2018) it was stated that there was an influence of perceived behavioral control on the intention to carry out internal whistleblowing. Meanwhile, the research by Park and Blekinsopp (2009) shows that the perceived variable of behavior control has no effect on external whistleblowing intentions. Dewi (2016) in her research stated that perceptions of behavioral control have no effect on intention to do whistleblowing.

Internal Control System. The internal control system is a system that controls an organization so that it is in line with the goals of the organization, and the internal control system also helps in delegating tasks and authorities, and finally one of the functions of internal control is protecting assets (Mulyadi, 1999). Wardana, Sujana, Wahyuni's (2017) research on Internal Control has a positive effect on fraud prevention. According to research by Purpasari, Suwardi (2012) shows that there is an interaction between individual morale and internal control. In conclusion, the level of morale possessed by an individual is influenced by the existing control system when the system is good and proper, the individual's morale also improves. However, Fikar's research (2013) states that the whistleblowing system is still not optimal for the effectiveness of internal control. This is because some Pertamina personnel still have a culture of not wanting to get involved and a culture of reluctance to report superiors, co-workers and parties who have a certain closeness because they are considered a form of unethical action.

Legal Protection. According to Soekanto (1984) legal protection is an effort to provide assistance and fulfillment of rights in order to bring a sense of security to witnesses and victims. The ideal legal protection is to provide rewards, treatment, and protection from all accusations as compensation for what has been disclosed by the whistleblower, whether he is one of the perpetrators or not (Nixson et. al, 2013). Abdullah, Hasma's research (2017) states that legal protection can moderate independent variables such as the seriousness of fraud and professionalism. However, with legal protection, someone has the courage to report fraudulent acts. In Azhari, Nuryanto's (2019) research explains that the emergence of whistleblowers is significant for disclosing cases of fraud or corruption in Indonesia and the high level of legal protection creates the courage of individuals to whistleblowing.

1.2 Hypothesis Development

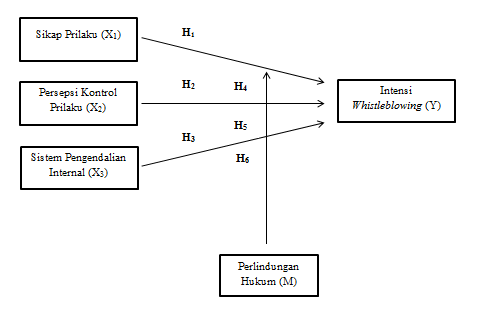

H₁: There is a positive effect of attitude on the intention to do whistleblowing.

H₂: There is a positive effect of perceived control on the intention to do whistleblowing

H₃: There is a positive influence of the internal control system on the intention to do whistleblowing

H₄: There is a positive influence of attitude towards the intention to do whistleblowing with Legal Protection as a moderating variable

H₅: There is a positive influence of perceived control on the intention to do whistleblowing with legal protection as a moderating variable

H₆: There is a positive influence of the Internal Control System on the intention to do whistleblowing with Legal Protection as a moderating variable.

2. Research methods

This research is a survey research with a quantitative approach. The object of research is employees of PT Kereta Api Indonesia Daop 5. The data used is primary data. The population in this study are employees of PT Kereta Api Indonesia Daop 5 Purwokerto, sample research using purposive sampling method.

Table 1. Variable operational definitions

Variable |

Variable concepts |

Indicator |

Whistleblowing intention (Y) |

Saud, Fauzi (2019) in which a questionnaire asks respondents to assess cases of fraud both small and large, after which respondents are asked to report the case or not, if reporting whether to company or outside the company. |

1. Report anonymously 2. Report with identity (measured based on the Park, Blenkinsopp, 2009) |

Attitude (X1) |

Attitude is an individual's assessment of behavior that is assessed based on how much they agree or disagree with the actions shown (Ajzen, 1991). |

1. Behavioral belief 2. Evaluation of important (Park, Blenkinsopp, 2009, which has been adapted by Winardi, 2013) |

Perceived control (X2) |

Perceived control is behavior control generated by individual perceptions to show the desired behavior, the behavior that the individual will do will receive support or resistance (Ajzen, 1991). |

1. Control believe 2. Perceived power (Park, Blenkinsopp, 2009, which has been adapted by Winardi, 2013) |

Internal control system (X3) |

Effective internal control in a company is one that is able to organize the organization with appropriate separation of structures of responsibilities, and is able to secure assets. Internal controls create healthy work practices and ensure the quality of employees properly. |

1. Control environment 2. Risk assessment 3. Control activities 4. Information and communication 5. Monitoring and enforcement of rules (Wardana I Gede ari kusuma, Sujana, Wahyuni, 2017) |

Legal protection (M) |

Legal protection for whistleblowers in Indonesia is regulated in Law no. 31 of 2014 concerning Protection of Witnesses and Victims. Legal protection consists of 5 indicators adapted to Tatawi's statement (2015) |

1. Respect for human dignity 2. A sense of security 3. Justice 4. Not discriminatory 5. Legal certainty (Tatawi, 2015) |

Analysis Techniques

Data there is more than one independent variable so that technical data analysis in this study uses multiple regression analysis and moderation:

Y = β0 + β1X1 + β2X2 + β3X3 + e (1)

Y = β0 + β1X1 + β2X2 + β3X3 + β4|X1 – M| + β5|X2– M| + β6|X3– M| (2)

Information:

Y = Whistleblowing intention

β0 = Constant

β1 β2 β3 = Coefficient of regression direction

X1 = Attitude

X2 = Perception of control

X3 = Internal control system

M = Moderation of legal protection

e = Error Term, namely the level of error in the estimator in the study.

3. Results and discussion

The following table shows the results of multiple regression analysis:

Table 2. Multiple linear regression test results

Dependent Variable |

Regression Coefficient |

Tcount |

Sig. |

X1 |

.539 |

3.128 |

0.003 |

X2 |

-.226 |

-1.821 |

0.074 |

X3 |

-.169 |

-.974 |

0.334 |

Constant |

2.143 |

0.000 |

1.000 |

Adj R Square |

0.189 |

||

Fcount |

5.206 |

||

Ftable |

2.79 |

||

Sig. F |

0.003 |

Based on the results of the table above, the regression equation is obtained as follows:

Y = 2.143 + 0.539X1 – 0.226X2 – 0.169X₃ + e3.1 Hypothesis test (t test)

a. First hypothesis testing

The β value obtained from multiple regression analysis for variable X1 shows the number 0.539, which means that attitude has a positive effect on whistleblowing intention at PT employees. KAI Daop 5 Purwokerto. The results of hypothesis testing in table 2 show t count 3.128 < t table 1.67 with a Sig value. 0.03 < α 0.05 which means that Ho1 is rejected and Ha1 is accepted, it can be concluded that the first hypothesis (H1), namely attitude has a positive effect on whistleblowing intentions of employees of PT Kereta Api Indonesia Daop 5 is supported.

b. Second hypothesis testing

The β value obtained from multiple regression analysis for variable X2 shows the number -0.226, which means that the perception of control has a negative effect on whistleblowing intention at PT Kereta Api Indonesia Daop 5. The results of testing the hypothesis in table 2 show t count -1.821 < t table 1.67 with a value of Sig. 0.074 > α 0.05, which means that Ho2 is accepted and Ha2 is rejected, so that the second hypothesis (H2) which states that perception of control has no effect on whistleblowing intentions of PT Kereta Api Indonesia Daop 5 is not supported.

c. Third Hypothesis Testing

The β value obtained from multiple regression analysis for variable X3 shows the number -0.169, which means that the internal control system has a negative effect on whistleblowing intention at PT employees. KAI Daop 5 Purwokerto. The results of hypothesis testing in table 2 show t count -0.975 < t table 1.67 with a Sig value. 0.334 > α 0.05 which means that Ho3 is accepted and Ha3 is rejected, so for the third hypothesis (H3) which states that the internal control system has no effect on whistleblowing intentions at PT Kereta Api Indonesia Daop 5 Purwokerto is not supported for the 4th, 5th, 6th hypothesis carried out with a moderation test. The following shows the results of the moderation test method.

Table 3. Moderation test results

hypothesis |

Adjusted |

Significance test |

Significance test |

Information |

||

F |

Sig |

t |

Sig |

|||

H4 |

||||||

Attitude, P. Law, Attitude*P. Law – Intention Whistleblowing |

0.136 |

3.837 |

0.015 |

has an influence |

||

Attitude |

2.034 |

0.047 |

has an influence |

|||

Legal protection |

.047 |

0.963 |

No influence |

|||

Attitude* Legal Protection |

.640 |

0.525 |

No influence |

|||

H5 |

||||||

Perception of Control, P. Law, Perception of Control*P. Law – Intention Whistleblowing |

0.144 |

2.857 |

0.046 |

has an influence |

||

Perception of Control |

-1.582 |

0.120 |

No influence |

|||

Legal protection |

2.333 |

0.024 |

has an influence |

|||

Control Perception*P. Law |

-.360 |

0.720 |

No influence |

|||

H6 |

||||||

Perception of Control, P. Law, Perception of Control*P. Law – Intention Whistleblowing |

0.037 |

1.686 |

0.182 |

No influence |

||

Perception of Control |

.462 |

0.646 |

No influence |

|||

Legal protection |

1.149 |

0.256 |

No influence |

|||

Control Perception*P. law |

-.482 |

0.632 |

No influence |

|||

3.2 Discussion

1. The influence of attitudes on whistleblowing intentions

The results above indicate that H1, namely attitude has a positive effect on employee intentions to carry out whistleblowing is accepted. The results of the analysis prove that the more self-belief that the actions to be taken will have positive consequences and on how much the individual agrees or disagrees with an act of fraud.

When attitudes affect whistleblowing intentions, it can be stated that it is in accordance with the theory used in this study, namely the theory of planned behavior (Ajzen, 1991). Why does the theory of planned behavior apply because when individuals have the strongest beliefs in assessing good or negative behavior, after that individuals tend to choose attitudes that behave positively.

The results of this study are in line with Saud's (2016) previous research which stated that attitudes have a significant positive effect on whistleblowing intentions. The results of these findings are also the same as Damayanthi, Sujana, Herawati's (2017) research who conducted an empirical study on university students, concluding that there is a positive and significant effect on attitudes towards the intention to disclose whistleblowing. However, this study is not in accordance with the results of Suryono (2016) which explains that attitude does not have a strong positive influence on the intention of civil servants to carry out whistleblowing. Mayasari, Setiyanto, Irawati (2018) that attitude does not have a positive influence on whistleblowing intentions.

2. The effect of perceived control on whistleblowing intentions

The results of the study do not support the second hypothesis that the control perception variable (X2) has a positive effect on employee intentions to do whistleblowing. When employees of PT Kereta Api Indonesia Daop 5 Purwokerto feels that the factors that support taking action on reports are few and there are more inhibiting factors, so that person has fears of getting retaliation or obstacles from the organization.

The theory of planned behavior in research is not suitable to be applied to employees of PT Kereta Api Indonesia Daop 5 because they cannot fully control their behavior under the control of these individuals, because they feel many threats when reporting fraudulent acts.

The results of this study are in line with Dian (2016) who proves that perceived behavioral control has no effect on intention to do whistleblowing. Another research that is in line is research conducted by Iskandar, Saragih (2018) which states that the lower the level of perceived control over perceived behavior, the stronger the intention of ASN to carry out whistleblowing. There is also research that is not in line with this study conducted by Winardi (2013) which proves that the perceived control variable has a significant influence on whistleblowing intention. Likewise, Mayasari, Setiyanto, Irawati's (2018) research proved that there was a positive influence between perceptions of control and whistleblowing intentions.

3. The influence of the internal control system on whistleblowing intentions

The results of the study do not support the third hypothesis that the internal control system variable (X3) has a positive effect on employee intentions to do whistleblowing. In other words, the better the internal control system, the less fraud will occur. PT Kereta Api Indonesia Daop 5 itself has created a whistleblowing system as a form of internal control system.

These results are inconsistent with the theory of planned behavior (Ajzen, 1991) which explains situational factors or environmental factors that support individuals and provide a sense of security, so that individuals have the intention to behave. When this happens, employees who have the intention to report the fraudulent act are not helped due to environmental factors that do not support it

The results of this study are in accordance with Shintadevi's (2015) research which explains the effectiveness of internal controls does not affect the tendency of accounting fraud. Rahayu, Prabowo (2018) show that the control environment has a negative influence on financial statement fraud, which means that the better the internal control system will reduce the risk of fraud cases occurring. This study obtained different results from Fikar (2013) who argued that the internal control system had a positive effect, as well as research by Puspasari, Suwardi (2012) which had a positive effect

4. The ability of legal protection to moderate the influence of attitudes towards whistleblowing intentions

The research results do not support the fourth hypothesis that the legal protection variable (Xm) is able to strengthen the influence of attitudes towards whistleblowing intentions. These results are in accordance with the majority of respondents' answers on the whistleblowing intention variable who answered negatively or did not report. Another indication is that employees of PT Kereta Api Indonesia Daop 5 has not considered whether or not there is legal protection because they are not sure that they will get a sense of security and protection.

This is not in accordance with the theory of planned behavior (Ajzen, 1991), which is the determinant of attitudes toward behavioral intentions. PT Kereta Api Indonesia Daop 5 employees, which is a state civil apparatus (ASN), has a negative belief in the enactment of a legal protection system that can increase individual and group courage against disclosing facts, because they see and hear from other people's experiences that legal protection in Indonesia is still a selective logging system and is still weak, so the courage and individual intent to report fraud is minimal.

The results of this study are in line with Dewi, Dewi, Sujana (2018) stating that Article 10 Paragraph (2) of Law No. 13 of 2006 is contrary to whistleblowers, because this article does not fulfill the principle of protecting a whistleblower, because those who report are still subject to punishment. However, in contrast to Effendy, Nuraini (2019) explaining that there is a positive effect of legal protection on whistleblowing intentions.

5. The ability of legal protection to moderate the influence of perceptions of control on whistleblowing intentions

The results of the study do not support the fifth hypothesis that the legal protection variable (Xm) is able to strengthen the effect of perceived control on whistleblowing intentions. Because they have the belief that legal protection is an inhibiting factor, due to the weak legal protection for ASN who work directly under government agencies, if they decide to report fraud, the possibility that will occur is to take very high risks, both external and internal.

This is inconsistent with the theory of planned behavior (Ajzen, 1991), namely the perception of control over behavioral intentions. Perceived behavior is shown when the individual has the perception that the behavior to be performed is easy or difficult.

This is in line with Abdullah, Hasma's (2017) research which applied legal protection as a moderating variable, explaining that legal protection is not an urgent matter to be considered for auditors to take whistleblowing action. However, in contrast to Effendy, Nuraini (2019) explaining that there is a positive effect of legal protection on whistleblowing intentions.

6. The ability of Legal Protection to moderate the influence of the internal control system on whistleblowing intentions

The research results do not support the sixth hypothesis that the legal protection variable (Xm) is able to strengthen the influence of the internal control system on whistleblowing intentions. Whistleblowing system which is a tool used by PT Kereta Api Indonesia Daop 5 as internal control has not run optimally and the procedural flow is unclear, so employees become confused when they find indications of fraud, because the existing protection system does not guarantee a sense of security and peace for these employees.

This is not in accordance with the theory of planned behavior (Ajzen, 1991), namely in situational or surrounding factors, meaning that when the individual's work environment and the surrounding environment help and do not hinder, the intention to report fraud will increase.

This research is in line with Herman's (2013) research which states that the internal control system has a negative effect on fraud prevention, meaning that the better the internal control, the less the risk of fraud. In Abdullah, Hasma's research (2017) that legal protection has a negative effect because legal protection for reporters has not yet been realized. However, in contrast to Effendy (2019) explaining that there is a positive effect of legal protection on whistleblowing intentions.

Conclusions and Implications

Conclusions

Based on the research results that have been described, the following conclusions can be drawn:

1. Attitude has a significant effect on the intention to take whistleblowing action on employees of PT. Indonesian Railway Daop 5 Purwokerto.

2. Perceived control has no effect on the intention to take whistleblowing action on employees of PT Kereta Api Indonesia Daop 5 Purwokerto.

3. The internal control system has no effect on the intention to take whistle-blowing action on employees of PT Kereta Api Indonesia Daop 5 Purwokerto.

4. Legal protection cannot moderate the influence of attitudes towards the intention to take whistleblowing actions on employees of PT Kereta Api Indonesia Daop 5 Purwokerto.

5. Legal protection cannot moderate the influence of perceptions of control on the intention to take whistleblowing actions on employees of PT Kereta Api Indonesia Daop 5 Purwokerto.

6. Legal protection cannot moderate the influence of the internal control system on the intention to take whistleblowing actions on employees of PT Kereta Api Indonesia Daop 5 Purwokerto.

Implications

Based on the results of the analysis, discussion and conclusions, theoretical and practical implications can be put forward as follows:

a) Based on the results of the research, it is necessary to have an operational framework for a whistleblowing system and Good Corporate Governance (GCG) to create a culture of having to report when there is suspicion of fraud, so that it supports and supports individual and situational factors for individuals according to the theory of planned behavior.

b) Attitudes that influence whistleblowing intentions can be further enhanced through training of employees regarding organizational ethics, as well as socialization regarding the dangers caused by fraud cases, and education regarding procedures for carrying out proper whistleblowing actions and their benefits is necessary. Through these educational efforts, it is hoped that employees will have awareness of the impact of fraud and increase good responses to whistleblowing actions.