(5)

(5)Ekonomika ISSN 1392-1258 eISSN 2424-6166

2024, vol. 103(4), pp. 112–128 DOI: https://doi.org/10.15388/Ekon.2024.103.4.7

Cordelia Onyinyechi Omodero

Covenant University, Ota, Nigeria

Email: onyinyechi.omodero@covenantuniversity.edu.ng

ORCID ID: https://orcid.org/0000-0002-8758-9756

Abstract. A strong monetary policy is critical to the overall health of an economy. Again, funding availability for firms is crucial and acts as a spur for well-designed monetary policy. The implications are far-reaching and have an impact on government revenue collection, which helps to enhance social welfare since providing basic social amenities is an essential component of effective governance, particularly in Sub-Saharan Africa (SSA). Thus, the purpose of this study is to investigate the impact of monetary policy on tax revenue growth in SSA. The investigation makes use of data from the World Bank Development Indicators and the International Monetary Fund spanning the years 1990–2022. The study also uses the autoregressive distributed lag (ARDL) approach to investigate the short- and long-run relationships between monetary policy instruments and tax revenue growth. Monetary policy methods employed include monetary authority credit to the private sector, domestic credit to the private sector, and wide money supply, while the tax revenue growth proportion to GDP is used. According to the findings, both the monetary authority and domestic credit to the private sector have considerable negative influences on tax revenue growth, whereas wide money has an encouraging but small effect. The consequence is that the private sector in SSA is underfinanced, making it harder for the government to collect substantial tax income to meet social duties. The paper recommends that the government and monetary authorities in SSA should adopt stronger monetary policies that promote private sector business growth, which, if implemented, will result in tax revenue increase.

Keywords: Monetary policy, Central Banks, tax revenue, money supply, private sector credit

_______

Received: 22/05/2024. Revised: 13/09/2024. Accepted: 26/10/2024

Copyright © 2024 Cordelia Onyinyechi Omodero. Published by Vilnius University Press

This is an Open Access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

_______

Financial regulation has a substantial impact on emerging nations’ revenue growth by affecting loan cost and accessibility, price increases control, and payment consistency (Bondarchuk & Raboshuk, 2020; Twinoburyo & Odhiambo, 2018). In all industrialized nations, the most important feature of the financial system is price stabilization, which is attained when volatility in prices of goods and services is controlled and constant for a lengthy period of time (Fourcans & Vranceanu, 2007; Li et al., 2010). For instance, pricing equilibrium is seen as a prerequisite for strong job creation and economic expansion (Angeriz & Arestis, 2007). Sound monetary administration strives to provide macroeconomic equilibrium, maintain an equitable distribution of money, cut prices, and achieve increased revenue and improvement in the economy (Akalpler & Duhok, 2018; Criste & Lupu, 2014). One of the primary issues that governments in Sub-Saharan Africa (SSA) have is raising enough tax money to meet Sustainable Development Goals (SDG) 3 and 10, which aim to increase the well-being of persons and eliminate societal inequality. Improvement of social welfare and provision of basic social amenities is the total package of a good governance in SSA.

A well-designed monetary strategy is intended to increase government revenue through tax receipts from businesses and people, particularly in rising economies. Tax income is the lifeblood of all economies, and it can only be sustained by proper Central Bank policies that encourage corporate growth, which leads to sufficient tax revenue collection and economic prosperity. This important aim can only be met if the monetary sector offers appropriate credit for private sector development of businesses and there is enough wide money in circulation to facilitate financing of production and product distribution services. For example, the money supply is an important monetary policy component influencing the United Kingdom growth and prosperity (Agbonlahor, 2014). Unrestricted access to domestic finance from banks leads to corporate growth. Job creation, greater tax revenue, and economic expansion will all be the outcome of corporate growth. As a result, a well-designed monetary policy has a multiplier impact across all sectors of the economy.

Prior to the 1990s, regulators for banks in most Sub-Saharan African nations was weak, resulting in several financial collapses (Thamae et al., 2023). Bank regulations in lower-income and middle-income countries in Sub-Saharan African nations have become progressively stricter as time went by due to constraints on obstacles to entrance, ownership arrangements, and other prudential guidelines. Despite the fact that constraints on bank ownership models and capitalization necessities changed the regulatory setting, the prudential measures were also implemented (Thamae et al., 2023). As put forward by Twinoburyo and Odhiambo (2018), implementing financial regulations in SSA states has challenges such as adhering to regulatory requirements and satisfying customers and investors. Since the late 1980s, numerous nations have implemented reforms to the finance industry, including significant changes to banking regulations and administrative structures (Thamae et al., 2023). Although there are numerous advantages of implementing monetary reforms in SSA countries, failures have hindered their ability to improve their economic structures. Given the widespread use of digital technology in most economies, Li et al. (2024) believe that central banks must evaluate and alter their monetary policy goals and instruments in order to migrate to the contemporary setting and maximize the well-being of society.

While numerous studies argue that monetary policy is a primary driver of economic growth and development (Akalpler & Dohok, 2018; Islam et al., 2021; Ndife, 2020; Sule, 2022), others (Ovat et al., 2022; Zuniga & Senbet, 2022) use statistical data to demonstrate its negative consequences. After reviewing various prior studies in this field, it is clear that there is a scarcity of research examining the impact of monetary policy on tax revenue growth. This study is particularly significant in Sub-Saharan Africa, where governments rely heavily on tax revenue due to the current constraint of oil reserves. All mechanisms to promote tax revenue growth in Sub-Saharan Africa are being used; thus, Central Bank monetary policies must not be disregarded in this process. As a result, the general goal of this research is to establish the impact of monetary authority credit to the private sector, money supply, and domestic credit to the private sector on tax revenue growth.

The study wishes to achieve the following definite aims.

i. To determine the extent to which money sector credit to private sector affect tax revenue generation in Sub-Saharan Africa.

ii. To examine the effectiveness of domestic credit to private sector in achieving tax revenue growth in Sub-Saharan Africa.

iii. To evaluate the importance of broad money to tax revenue collection in Sub-Saharan Africa.

In order to achieve the above specific objectives, the study has made the following null assumptions.

H01 Money sector credit to private sector does not affect tax revenue generation in Sub-Saharan Africa.

H02 Domestic credit to private sector is not significantly effective in achieving tax revenue growth in Sub-Saharan Africa.

H03 Broad money is not substantially important to tax revenue collection in Sub-Saharan Africa.

Domestic credit to the private sector refers to money provided to the private sector by commercial banks and other financial institutions in the form of loans, the acquisition of nonequity bonds, trade credits, and other receivables from consumers that create a repayment obligation (The World Bank, 2024). Financial policy plays an important role in determining investments. The quantity of capital invested is determined by financial policy measures such as commercial bank interest rates on loans and easy credit availability (Mehar, 2023). The extension of credit to the business community boosts the liquidity of the markets, which is vital in determining investment decisions. In reality, the efficacy of monetary regulation is dependent on the use of domestic credit to the private sector to boost economic and commercial activity (Mehar, 2023). Mehar (2011) outlined various processes that have rendered financial policy to a problematic tool for managing the global economy. In accordance to this strategy, the most significant regressive choice is the interest rate disparity. If manufacturers employ debt finance to finance their manufacturing operations and inventory holdings, greater interest costs might cause price increases. Interest on loans from commercial lending institutions to meet working capital needs can be incorporated into the overall expenses of manufacturing, which is a form of inflation caused by cost-push factors (Mehar, 2018). As a result, private enterprises will face a difficulty to pay debt service commitments, perhaps leaving no taxable profit to be remitted to the government. Empirical research confirms that the variety of enterprises employing banking institutions to fund their investments, as well as the amount of broad money, impact the size of lending to the entrepreneurial community (Mehar, 2021).

Domestic financing available to the business community consists of financial backing offered to the commercial enterprises in the form of advances, nonequity securities purchases, trade credits, and other accounts receivable that create an entitlement for reimbursement. Some nations consider credit to state enterprises among their legitimate claims (World Bank, 2022). For the sake of this study and its context, Monetary Sector Credit to the Private Sector might be defined as monies provided by the World Bank, the International Monetary Fund (IMF), and sovereign central banks. It differs from domestic credit to the private sector in that domestic credit is provided by commercial banks and other lending domestic financial institutions operating within a country. Monetary Sector Credit to Private Sector as a percentage of GDP was recorded at 14.095% in 2022 for Nigeria as a nation in Sub-Saharan Africa. This represents a rise above the prior figure of 13.449% for 2021. Nigeria Financial Sector Loan to Commercial Sector as a percentage of gross domestic product (GDP) information is reviewed annually, with an average of 7.811% from December 1960 to December 2022 and 63 occurrences. The statistics peaked at 19.626% in 2009 and dropped to an unprecedented low of 3.697% in 1960 (World Bank, 2022).

The central bank divides the supply of money into two categories: narrow funds and expansive monies. The term narrow money (M1) refers to the cash in circulation and current accounts holdings with banks for business. The term broad money refers to the overall amount of money in the country’s economy, encompassing narrow money, savings, time deposits, and foreign currency deposits (Central Bank of Nigeria, 2006). Overflow circulating cash occurs when the quantity of cash circulating exceeds the economic system’s entire production. Excessive liquidity in the economy disrupts equilibrium between prices, resulting in inflation and increased costs for products. Broad money is a notion that describes the manner in which money moves in a financial system. The design is described as the most complete means of determining the size of a nation’s liquidity, which includes every kind of asset that consumers and companies may use for transactions or maintain as investments for a short period of time, such as cash, deposits in bank accounts, and everything with a monetary value. Broad money consists of coins and banknotes, as well as bank accounts and deposit. Treasury securities and gilts are examples of widespread finance. These forms of money are referred to as ‘close to monies’ since they are less accessible compared to banknotes and quick savings accounts. Investments like long-term dated stocks and bonds are excluded from expansive liquidity. Since these may be exchanged, they are not considered wide money given that they are classified as investments instead of money (Economics, 2024).

Broad money refers to M2, M3, and M4. Wide currency is more volatile than narrower conceptions. According to Ionescu et al. (2023), money is intrinsic, suggesting that its availability is dictated by the need for credit and bank operations. This indicates that modifications in the broader framework, such as borrowing costs or the state of the economy, will affect the amount of cash in circulation. Central banks employ the money supply as an intentionally designed instrument to control economic activity (Ionescu et al., 2023).

Tax revenue is referred to as the amount of money derived from earnings and profits taxes, payouts for social security, taxes on products and services, salary taxes, holdings of property and inheritance taxes, and other sources (OECD, 2024). Taxation is the primary means by which governments produce public money, which allows them to make expenditures in human resources, amenities and the supply of goods and services to their citizens and enterprises (World Bank, 2024). However, various crises have lowered developing nations’ earnings while boosting expenditures in the past few years (World Bank, 2024). It is important to note that monetary policy fluctuations may be one of the issues and crises reducing the government’s tax revenue collection, particularly policies governing the amount of credit available for the operation of private businesses from which the government expects to collect sufficient tax revenues.

Monetary policy is a type of macroeconomic plan in which the central bank influences economic activity by modifying the amount of money supply, interest rate levels, exchange rates, and other factors. Its purpose is to produce steady and sustained revenue growth by managing the amount of cash available and interest rates (Su, 2023). The central bank may impact the rate of interest, lending conditions, and the availability of cash through financial regulation adjustments, regulating business activity and investments and promoting the growth of the economy (Jahufer & Hanainy, 2023). By controlling the pace of inflation and fostering an optimal financing setting, monetary guidelines may offer commercial predictable and stable conditions, boost business venture capital and creativity, and support long-term expansion of the economy (Gamboa-Estrada, 2020). However, a liquidity threat could be inevitable when the banking institution is unable to lend to the private sectors. A liquidity threat is the possibility that a banking institution may be incapable of taking out adequate money or transform sufficient securities to cash promptly without experiencing significant loss of value to satisfy its temporary spending requirements (Marthinsen & Gordon, 2024). Transmission takes place when liquidity concerns at one or more large banking organizations escalate, contributing to market values for assets to decline and instability to go up, which leads to widespread (domestic or worldwide) challenges that diminish credit, lowers real gross domestic product, and elevate underemployment and monetary dysfunction (Marthinsen & Gordon, 2024).

Keynesian monetary policy hypothesis. Keynes (1973) argued for low-interest-rate policies.

As liquidity grows, interest rates decline. Lower borrowing costs will increase investments due to capital’s optimal performance. Keynesians argue that broad-based monetary stimulation lowers the rate of interest by increasing loanable funds in the banking sector.

Lower interest rates lead to increased expenditure on investment and interest-sensitive consumer products, which boosts government income (Antonio, 2019). The Keynesian hypothesis questioned the premise that revenue and commodity prices are directly proportional (Keynes, 1973). In accordance with the Keynesian position, financial regulation has a significant impact on how the economy functions. Based on this perspective, modifications to the amount of cash in circulation can affect factors over time such as interest rates, exchange rates, inflation, and overall consumer demand, job creation, productivity, and earnings (Antonio, 2019). As confirmed by Wang et al. (2024) monetary policy appears to have a primary impact on the Real Estate Investment Trusts (REITs) market, especially during economic crises, and determines the long-term risks associated with the US REITs business at both the collective and sector-specific bases. Thus, it is expected that during an economic downturn, monetary policies should address possible liquidity issues in the banking sector, promote commercial lending to enhance market liquidity, and provide finance accessibility for small-, micro-, and medium-sized companies (Boiko et al., 2022; Bašić & Ćurić, 2021; Lebedeva & Shkuropadska, 2023).

Tosun and Selim (2024) investigated the implications of monetary strategies undertaken by wealthy nations and emerging nations’ autonomy of central banks on their commercial instability. The study found that restrictive monetary policies undertaken by nations with advanced economies, as well as changes in central bank governors, lead to increased financial fragility for both categories. Nevertheless, the alteration in authorities amplifies the beneficial impact of restrictive monetary policy on financial stability.

Sule (2022) investigated how monetary policy tools influence revenue growth in Nigeria. The study found that monetary policy’s currency supply flexibility was unequal, resulting in limited access to finance for essential firms and hindering growth. Zuniga and Senbet (2022) analyzed South Korea monetary system from 1980 and 2017. The research effort assessed the efficiency of the banking system in two time frames: 1980–1999, while the Central Bank of Korea primarily utilized broad money supply (M2), and 2000–2017, when rates of interest were the main monetary policy mechanism. The study found that monetary intervention based on interest rates was more successful in boosting business investment than M2. Ovat et al. (2022) used yearly data from 2006 to 2020 to assess the impact of the central bank’s monetary policy rate on the growth of the Nigerian economy. The research results demonstrated that central bank interest rates exerted a detrimental and substantial influence on economic expansion.

Islam et al. (2021) investigated the link between monetary easing and economic development in Bangladesh and the United Kingdom. The results of the research revealed that monetary laws had a long-term impact on economic expansion in both nations. Long-run indices showed that the cash supply had a helpful long-term influence on GDP growth in both nations. In contrast to the UK, the exchange rate has a negative impact on Bangladesh’s growth in commerce. The bank rate appears to support economic growth in the UK. The results further demonstrated that rising loan interest rates exerted a negative impact on economies of both nations.

Tan et al. (2020) investigated the effects of fiscal and monetary measures on economic development in Malaysia, Singapore, and Thailand between 1980:Q1 and 2017:Q1. The primary results of the research show that interest rates had a detrimental influence on financial growth across the three specific nations used in the study. Ndife (2020) examined how monetary regulation affects Nigeria’s growth in the economy. The investigation applied data on the prime rate of borrowing, maximal financing velocity, and interbank demand rate as financial policy parameters, whereas GDP at present values was used to estimate expansion in the economy. The analysis revealed that only the maximum loan rate had a substantial impact on the growth of the economy in Nigeria.

Chris-Ejiogu et al. (2019) discovered that the ARDL regression evaluation revealed that the interest rate used for monetary policy had a beneficial correlation with real GDP, which was unfamiliar considering its final influence on prime interest rates, which affects productive business activity. Alqahtani et al. (2019) employed nonstructural VAR analyses to evaluate the influence of two newly created US central bank unpredictability indexes comprising the US Baker, Bloom, and Davis (BDD) monetary policy uncertainty (MPU) and Husted, Rogers, and Sun (HRS) MPU on the Gulf Cooperation Council. The findings indicated that the two MPUs had a minor but considerable influence on several Gulf Cooperation Council economies. The HRS MPU had more of an effect than the BBD MPU.

Akalpler and Duhok (2018) explored the link between monetary policy and economic development in Malaysia. The research discovered an advantageous correlation between revenue growth and interest rates. There was also a beneficial connection between economic expansion and the quantity of cash supply. Twinoburyo and Odhiambo (2018) examined the influence of the banking system on financial growth in Tanzania from 1975 to 2013. The paper investigates this relationship using two financial policy proxies, notably the amount of cash supply and the interest rate. The empirical findings from the research demonstrated that monetary guidelines had no permanent effect on the growth of the economy. The short-term outcomes corroborated the principle of monetary neutrality when interest rates were employed as a surrogate. Measuring monetary policy through money supply resulted in an adverse association with GDP growth.

Akinjare et al. (2016) assessed the impact of monetary regulations on Nigeria’s growth in GDP. The findings revealed that interest rates, currency rates, and money supply have a substantial influence on the economy, however price increases is not a pertinent statistical driver in determining the trajectory of the economy in Nigeria. Eminike (2016) examined the connection between monetary regulations and entrepreneurial loans. The interconnected analysis findings showed a long-term association between monetary regulation and loans to the business community. Long-run factor measurements of stability indicated a cointegration even with fundamental breakdowns. Correction of errors model outcomes indicated that modifications to loans have a satisfactory and large immediate impact on financial policy modifications.

Development accounting outcomes demonstrate how lending improvements affect financial policy. The causality analysis by Granger study shows a one-way relationship between credit and financial regulation.

Fasanya et al. (2013) had shown that the inflation rate, exchange rate, and foreign reserve constituted vital monetary policy measures that promoted economic expansion in Nigeria.

Equations 1–5 highlights the model chosen for the present investigation.

Y = β0 + βX1 + βX2 + βX3 + μit (1)

where:

Y = tax revenue,

X1 – X3 = monetary policy tools,

β = coefficient,

μit = error term.

Equation 1 can be clearly functional in this investigation, as demonstrated in Equation 2 below:

TXRV = β0 + β1 MCPS + β2 DCPS + β3 BSM2 + μit (2)

where:

TXRV = Tax revenue generated in sub-Saharan Africa (SSA);

MCPS = Monetary Sector Credit to Private Sector in SSA;

DCPS = Domestic Credit to Private Sector by Banks in SSA

BSM2 = Broad money M2 % of GDP;

β0 = Coefficient of the parameter estimate;

β1 – β3 = Intercept;

μit = Error term.

To assess the variables’ short- and long-term associations, the study applied a limits testing approach to cointegration developed by (Pesaran et al., 2001). This strategy can produce superior results since it eliminates the difficulties connected with the sequence of integration revealed in the Johansen cointegration study. It is suitable for usage with small sample numbers and can estimate both short- and long-term outcomes simultaneously. Two important camera range properties justify the existence of cointegration. They are identified as I(0) and I, correspondingly (1). The first is the limit that is lower, while the second is the maximum limit. If the F-statistic is above the uppermost benchmark stage, the null assumption of no a long-term association is rejected, independent of the series’ connection sequence. Nonetheless, once a test statistic is smaller than the lower critical value, the research is unable to invalidate the null hypothesis; when it is located between the lower and upper critical boundaries, the conclusion is considered to be unclear (Pesaran et al., 2001). To determine whether or not there is a long-run link between the variables, the bound test hypotheses are shown in Equations 3 and 4 below:

H₀: δ₁ = δ₂ = δ₃ = δ₄ = 0 (There is long-run relationship in the series) (3)

H1: δ₁ ≠ δ₂ ≠ δ₃ ≠ δ₄ ≠ 0 (No long-run relationship exists in the series) (4)

The ARDL model measurement is presented in Equation 5 below:

(5)

where: Ø indicates the short run coefficents, ∆ denotes the first differenced operator, t represents time, and µt denotes the white-noise error term.

|

Variable code |

Description and measurement |

Data collection period |

Source |

|

TXRV |

Tax revenue in SSA and collected in billions of USD |

1990–2022 |

WDI & OECD |

|

MCPS |

Monetary Sector Credit to Private Sector collected in billions of USD |

1990–2022 |

WDI & IMF |

|

DCPS |

Domestic Credit to Private Sector by Banks collected in billions of USD |

1990–2022 |

WDI & IMF |

|

BSM2 |

Broad money M2 as a % of GDP |

1990–2022 |

WDI & IMF |

Section 4 presents the findings of the analysis conducted in this study. The descriptive analysis in Table 2 describes the nature of the datasets used in this study. The goal is to guarantee that datasets are normally distributed. Kurtosis and the Jarque–Bera value are two instruments utilized for this confirmation. The kurtosis results range from 2 to 3, implying that the datasets for all variables are normally distributed. The Jarque–Bera results also serve to establish that the dataset’s distribution is normal, as all of the p-values are greater than the 0.05 significance level.

|

TXRV |

MCPS |

DCPS |

BSM2 |

|

|

Mean |

2.626 |

3.295 |

3.784 |

3.502 |

|

Median |

2.721 |

3.296 |

3.819 |

3.505 |

|

Maximum |

3.336 |

3.434 |

4.027 |

3.723 |

|

Minimum |

1.374 |

3.135 |

3.472 |

3.194 |

|

Std. Dev. |

0.584 |

0.078 |

0.151 |

0.145 |

|

Skewness |

-0.486 |

-0.295 |

-0.177 |

-0.456 |

|

Kurtosis |

2.152 |

2.569 |

2.160 |

2.383 |

|

Jarque-Bera |

2.291 |

0.734 |

1.142 |

1.665 |

|

Probability |

0.318 |

0.693 |

0.565 |

0.435 |

|

Sum |

86.67 |

108.7 |

124.9 |

115.6 |

|

Sum Sq. Dev. |

10.92 |

0.198 |

0.728 |

0.671 |

|

Observations |

33 |

33 |

33 |

33 |

Correlation matrix |

||||

|

TXRV |

1.000 |

|||

|

MCPS |

0.196 |

1.000 |

||

|

DCPS |

-0.011 |

0.723 |

1.000 |

|

|

BSM2 |

0.783 |

0.478 |

0.001 |

1.000 |

The correlation matrix included in Table 2 shows the relationship among the variables. The monetary sector credit to the private sector (MCPS) has a very weak relationship with tax revenue collection (TXRV) in Sub-Saharan Africa. The domestic credit to the private sector (DCPS) has a very weak and negative relationship with TXRV but the broad money supply has a strong positive relationship with the TXRV.

|

Variable type |

ADF-Statistic |

Critical value @ 5% |

P-value |

Order of Integration |

|

TXRV |

-5.372 |

-2.960 |

0.000 |

I(1) |

|

MCPS |

-3.805 |

-2.957 |

0.007 |

I(0) |

|

DCPS |

-5.322 |

-2.968 |

0.000 |

I(1) |

|

BSM2 |

-6.665 |

-2.960 |

0.000 |

I(1) |

An unstable time series has a continuously varying average, a variance, or combination of the two. A regression analysis involving fluctuating time series might produce erroneous or meaningless results (Granger & Newbold, 1974; Yule, 1926). It suggests that there may be a correlation of statistical significance even though there should not be such (Emenike, 2016). When doing a regression evaluation, it is important to test for the stationary nature of datasets or their level of incorporation. The result in Table 3 shows that the series are stationary at both order 1 and zero (0). The significance is that the use of ARDL is necessary when this scenario occurs (Pesaran et al., 2001). Thus, the use of ARDL in this work is justified because that series are stationary at level and first difference.

|

F-Statistic Value |

Significance |

I0 Bound |

I1 Bound |

|

0.335 |

10% |

2.72 |

3.77 |

|

5% |

3.23 |

4.35 |

|

|

2.5% |

3.69 |

4.89 |

|

|

1% |

4.29 |

5.61 |

The bound test suggested by Pesaran et al. (2001) is performed in Table 4, which demonstrates that the F-statistic value is less than both the upper and lower boundaries. In this scenario, it becomes apparent that there is no long-term association. As a result, the null hypothesis of a long-term relationship is rejected.

|

Lag |

LogL |

LR |

FPE |

AIC |

SC |

HQ |

|

0 |

9.328 |

NA |

0.040 |

-0.381 |

-0.190 |

-0.322 |

|

1 |

29.04 |

32.39* |

0.011* |

-1.717* |

-1.479* |

-1.645* |

|

2 |

29.04 |

0.001 |

0.011 |

-1.646 |

-1.361 |

-1.558 |

|

3 |

29.28 |

0.349 |

0.012 |

-1.591 |

-1.258 |

-1.489 |

|

4 |

29.39 |

0.166 |

0.013 |

-1.528 |

-1.147 |

-1.412 |

|

5 |

29.400 |

0.010 |

0.014 |

-1.457 |

-1.029 |

-1.326 |

The lag selection test results are displayed in Table 5, indicating that all of the criteria picked lag 1. However, the decision to choose lag 1 is based on the AIC choice of lag, which corresponds to the selection of other lag criteria.

Table 6 shows the particular influence of each predictor on tax revenue collection in Sub-Saharan Africa. The monetary sector lending to the private sector (MCPS) has a significant and negative impact (p-value of 0.03 and t-statistic of -0.078) on tax revenue collection in Sub-Saharan Africa. The similar finding is evident in the broad money supply (BSM2), with a p-value of 0.02 below 0.05 and a t-statistic of -0.65, indicating a negative intangible effect on tax revenue. Thus, we reject the H01 which states that monetary sector lending to the private sector does not significantly affect tax revenue growth. This conclusion is consistent with the findings of (Ovat et al., 2022; Zuniga & Senbet, 2022). Domestic credit to the private sector (DCPS) has a favorable effect but it is inconsequential. In this case, we fail to reject H02 which assumes that domestic credit does not majorly affect tax revenue generation. The findings are highly supported by the works of (Ovat et al., 2022; Sule, 2022), but Islam et al. (2022) and Ndife (2020) provide contradicting results. Furthermore, the broad money supply is negatively determining the decrease in tax revenue collection in Sub-Saharan Africa. H03 cannot be declined. The Durbin–Watson value of about 2 shows the lack of autocorrelation. The standard error of regression has also proven that the projection is right, as the figure of 0.106 is significantly lower than the value of 1.

|

Dependent Variable: D(TXRV) |

||||

|

Variable |

Coefficient |

Std. Error |

t-Statistic |

Prob. |

|

D(TXRV(-1)) |

0.015 |

0.195 |

0.081 |

0.936 |

|

D(MCPS(-1)) |

-0.036 |

0.466 |

-0.078 |

0.038* |

|

D(DCPS(-1)) |

0.041 |

0.297 |

0.138 |

0.891 |

|

D(BSM2(-1)) |

-0.286 |

0.438 |

-0.652 |

0.021* |

|

C |

0.059 |

0.023 |

2.582 |

0.015 |

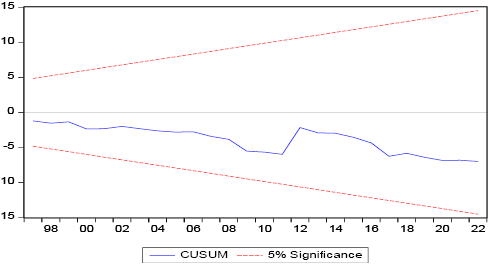

Figures 1 and 3 confirm that the model used in this study is robust and reliable in all material standard. The appearance of the blue line at the middle of the two dotted red lines in the CUSUM test of stability in Figures 1&3 confirms that the model is stable.

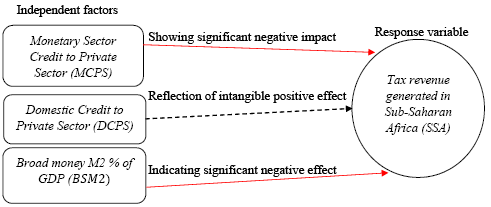

Figure 2 is a diagrammatic reflection of the results displayed in Table 6. From the diagram, the study indicates that the monetary sector credit to private sector and broad money supply have substantial adverse effects on tax revenue generation in SSA. This is reflected with a red arrow touching the dependent factor. However, the domestic credit to private sector appears positive but insignificant and it is shown with a black dotted arrow. These outcomes are robust and require relevant policy decision to improve tax revenue mobilization in the SSA. The Central Banks of countries in the SSA will need to improve the quantity of money in circulation to foster private sector operations. Private sectors also depend on availability of credits to expand their economic activities. This is enabled by improving monetary policy guidelines on cash reserves and enabling credit flow from Central Banks to domestic banks, thereby putting aside all restriction that prevent private sector access to funds.

|

Test |

Statistics |

P-value |

|

Serial correlation LM test |

1.392 |

0.249 |

|

Ramsey RESET test |

0.163 |

0.873 |

|

Heteroskedasticity test |

0.344 |

0.845 |

Furthermore, the diagnostic tests performed in this investigation, as indicated in Table 7, reveal no serial correlation or heteroskedasticity. If the p-values are less than the 5% significance level, serial correlation and heteroskedasticity will occur. In this case, both are of greater value than 0.05. As a result, the null hypothesis of serial correlation and heteroskedasticity is rejected. Table 6 shows that the Durbin–Watson result indicates no serial association.

The study looks at how monetary policy might help enhance tax revenue growth in Sub-Saharan Africa. It spans the years 1990 to 2022 and uses tax income as a response variable, with broad money supply by Central Banks in Sub-Saharan African nations and private sector credits serving as predictor factors. The overall finding is that monetary policy in Sub-Saharan Africa does not encourage tax revenue growth, but rather has a negative impact on it due to a lack of access to financing by the private sector, which utilizes the money for business and, in turn, pays taxes to the government. The amount of tax that the government of Sub-Saharan Africa may collect from enterprises and those who work for these firms is determined by the level of company expansion caused by money availability and supply. The policy issue is that Sub-Saharan Africa’s governments and monetary authorities must implement ways to boost tax revenue growth through free credit and tax breaks. Borrowing constraints that restrict access to money will be removed. The negative effect of domestic credit indicates that private sectors are underfinanced in the regions where they operate and do not get external help from monetary authorities outside their territory. It is critical that the different governments in Sub-Saharan Africa respond to this difficulty in order to allow the private sector to operate smoothly while also increasing government income.

Originality statement. Assessment of financial strategies in SSA is critical, and empirical works in this subject area is still very scarce in SSA. Thus, the study aims to promote equitable development and monetary policies, geared at stimulating the private sector financial health and equal opportunity of individuals make this work very unique. The major limitations of this study include data constraints and access to key personnel of Central Banks of countries in SSA, for the purposes of obtaining oral evidences to support our findings.

Agbonlahor, O. (2014). The impact of monetary policy on the economy of the United Kingdom: A Vector Error Correction Model (VECM). European Scientific Journal, 10(16), 19-42. https://core.ac.uk/download/pdf/236408521.pdf.

Akalpler, E., & Duhok, D. (2018). Does monetary policy affect economic growth: evidence from Malaysia. Journal of Economic and Administrative Sciences, 34(1), 2-20. https://doi.org/10.1108/JEAS-03-2017-0013.

Akinjare, V., Babajide, A.A., Isibor, A.A., Okafor, T. (2016), Monetary policy and its Effectiveness on economic development in Nigeria. International Business Management, 10(22), 5336-5340. http://dx.doi.org/10.3923/ibm.2016.5336.5340.

Alqahtani, A.S.S., Ouyang, H., & Saleh, S (2019). The impact of United States monetary policy Uncertainty on the Gulf Cooperation Council stock markets. Investment Management and Financial Innovations, 16(1), 128-143. http://dx.doi.org/10.21511/imfi.16(1).2019.10.

Angeriz, A., & Arestis, P. (2007). Monetary policy in the UK. Cambridge Journal of Economics, 31(6), 863–884. http://www.jstor.org/stable/23601862.

Antonio, P.M. (2019). Monetary policy instruments and convergence of its objectives: Case of Angola. Journal of Economics and Public Finance, 5(2), 161-182. http://dx.doi.org/10.22158/jepf.v5n2p161

Bašić, D., & Ćurić, P. (2021). Adaptability of securitization model to conditions of volatile Financial structure. ECONOMICS - Innovative and Economics Research Journal, 9(1), 205–220. https://doi.org/10.2478/eoik-2021-0012.

Boiko A., Umantsiv Y., Cherlenjak I., Prikhodko, V., & Shkuropadska, D. (2022). Policy measures For economic resilience of Visegrad Group and Ukraine during the pandemic. Problems and Perspectives in Management, 20(2), 71-83. http://dx.doi.org/10.21511/ppm.20(2).2022.07.

Bondarchuk, V., & Raboshuk, A. (2020). The impact of monetary policy on economic growth in Ukraine. Ekonomista, 1(1), 94-115. https://journals.pan.pl/Content/116613/PDF/EKON_2020-01_05-Bondarchuk-Raboshuk.pdf.

Central Bank of Nigeria (2006). How does the monetary policy decisions of the central bank of Nigeria affect you? Part one. Monetary Policy Series CBN/MPD/Series/02/2006. https://www.cbn.gov.ng/Out/EduSeries/Series2.pdf.

Chris-Ejiogu, D.U.G., Emmanuel, D.B., & Kalu Awa, S. (2019). Effect of Fiscal and Monetary Policy Instruments on Economic Growth of Nigeria from 1985-2016. International Journal of Contemporary Research and Review, 10(10), 21635–21655. https://doi.org/10.15520/ijcrr.v10i10.763.

Criste, A., & Lupu, I. (2014). The Central Bank Policy between the Price Stability Objective and Promoting Financial Stability. Procedia Economics and Finance, 8(1), 219-225. https://doi.org/10.1016/S2212-5671(14)00084-7.

Economics (2024). Broad money definition. Retrieved on April 18, 2024 from: https://www.economicshelp.org/blog/glossary/broad-money/.

Emenike, K.O. (2016). How does monetary policy and private sector credit interact in a developing

Economy? Intellectual Economics, 10(1), 92–100. http://dx.doi.org/10.1016/j.intele.2017.03.001.

Fourcans, A., & Vranceanu, R. (2007). The ECB monetary policy: Choices and challenges. Journal of Policy Modeling, 29(2), 181-194. https://doi.org/10.1016/j.jpolmod.2006.12.004.

Fasanya, I.O., Onakoya, A.B.O., & Agboluaje, M.A. (2013). Does monetary policy influence Economic growth in Nigeria? Asian Economic and Financial Review, 3(5), 635-646. https://archive.aessweb.com/index.php/5002/article/view/1037.

Gamboa-Estrada, F. (2020). The determinants of private capital flows in emerging economies: The role of Fed’s unconventional monetary policy. Contemporary Economic Policy, Western Economic Association International, 38(4), 694-710. https://doi.org/10.1111/coep.12474.

Ionescu, R.V., Fortea, C., Zlati, M.L., & Antohi, V.M. (2023). Studying Differing Impacts of Various Monetary Aggregates on the Real Economy. International Journal of Financial Studies, 11(4), 1-22. https://doi.org/10.3390/ijfs11040140

Islam, M.S., Hossain, M.E., Chakrobortty, S., & Nishat, S.E. (2021). Does the monetary policy Have any short-run and long-run effect on economic growth? A developing and a developed country perspective. Asian Journal of Economics and Banking, 6(1), 26-49. https://doi.org/10.1108/AJEB-02-2021-0014.

Jahufer, A., & Hanainy, M. F. (2023). Effects of Monetary Shocks in Sri Lankan Economy. Iranian Economic Review, 27(3), 1103-1133. https://doi.org/10.22059/ier.2022.85442.

Keynes, J.M. (1973). The General Theory of Employment, Interest and Money. London: MacMillan. https://www.scirp.org/reference/referencespapers?referenceid=1954699.

Lebedeva, L., & Shkuropadska, D. (2023). Turnover in EU monetary policy in a crisis. ECONOMICS – Innovative and Economics Research Journal, 11(1), 177 – 194. Doi: 10.2478/eoik-2023-0011.

Li, J., Wang, T., & Su, Z. (2024). Optimal monetary policy under digital technology shock. Technological Forecasting and Social Change, 200(1), 1-6. https://doi.org/10.1016/j.techfore.2023.123133.

Li, Y.D., Iscan, T.B., & Xu, K. (2010). The impact of monetary policy shocks on stock prices: Evidence from Canada and the United States. Journal of International Money and Finance, 29(5), 876-896. https://doi.org/10.1016/j.jimonfin.2010.03.008.

Marthinsen, J.E., & Gordon, S.R. (2024). Synthetic Central Bank Digital Currencies and systemic Liquidity risks. International Journal of Financial Studies, 12(1), 1-17. https://doi.org/10.3390/ijfs12010019.

Mehar, A. (2011). How monetary policy affect poverty: nexus and consequences. South Asian Journal of Management Sciences, 5(1), 1-10. http://sajms.iurc.edu.pk/issues/2011a/Spring2011V5N1P1.pdf.

Mehar, A. (2018). Impact of monetary policy on growth and poverty: Drastic consequences Of government intervention. Journal of Modern Economy, 1(1), 1—16. DOI: 10.28933/jme-2018-01-2801. https://escipub.com/Articles/JME/JME-2018-01-2801.

Mehar, M.A.K. (2021). Bridge financing during covid-19 pandemics: Nexus of FDI, external Borrowing and fiscal policy. Transnational Corporations Review, 13(1), 109–124. https://doi.org/10.1080/19186444.2020.1866377.

Mehar, M.A. (2023). Role of monetary policy in economic growth and development: from Theory to empirical evidence. Asian Journal of Economics and Banking, 7(1), 99-120. https://doi.org/10.1108/AJEB-12-2021-0148.

Ndife, C.F. (2020). Impact of monetary policy on economic growth of Nigeria. African Scholar Publication & Research International, 18(7), 384–393. https://www.africanscholarpublications.com/wp-content/uploads/2021/01/AJMSE_Vol18_No7_Sept_2020-23.pdf.

Ovat, O.O., Ishaku, R.N., Ugbaka, M.A., & Ifere, E.O. (2022). Monetary policy rate and economic Growth in Nigeria. International Journal of Economics and Financial Issues, 12(3), 53–59. https://doi.org/10.32479/ijefi.12868.

OECD (2024). Tax revenue (indicator). DOI: 10.1787/d98b8cf5-en (Accessed on 21 April 2024).

Su, C. (2023). Research on the Impact of Monetary Policy on the Economic Cycle and Its Control Strategies. Proceedings of the 2023 2nd International Conference on Economics, Smart Finance and Contemporary Trade (ESFCT 2023), Advances in Economics, Business and Management Research 261, https://doi.org/10.2991/978-94-6463-268-2_51.

Sule, A. (2022). Pass-Through effect of monetary policy tools on economic growth in Nigeria. Journal of Public Affairs, 22(3), e2588. https://doi.org/10.1002/pa.2588.

Tan, C-T., Azali, M., Muzafar, S.H., & Lee, C. (2020). The impacts of monetary and fiscal policies On economic growth in Malaysia, Singapore and Thailand. South Asian Journal of Macroeconomics and Public Finance, 9(1), 114-130. DOI: 10.1177/2277978720906066.

Thamae, R.I., Odhiambo, N.M., & Khumalo, J.M. (2023). Bank regulation in the selected sub-Saharan African countries: Dynamics and trends. Journal of Central Banking Theory and Practice, 2023(1), 175 – 198. https://doi.org/10.2478/jcbtp-2023-0008.

Tosun, B., & Selim, B. (2024). Financial fragility in developing countries: An analysis in the Context of monetary policy and central bank independence. Journal of Central Banking Theory and Practice, 2024(1), 89 – 116. https://doi.org/10.2478/jcbtp-2024-0005.

Twinoburyo, E. N., & Odhiambo, N.M. (2018). Can monetary policy drive economic growth? Empirical evidence from Tanzania. Contemporary Economics, 12(2), 207-222. https://doi.org/10.5709/ce.1897-9254.272.

Wang, S., Gupta, R., Bonato, M., & Cepni, O. (2024). The effect of conventional and Unconventional monetary policy shocks on US REITS moments: Evidence from VARS with Functional shocks. The Journal of Real Estate Finance and Economics https://doi.org/10.1007/s11146-024-09978-z.

World Bank (2024). Domestic credit to private sector (% of GDP). Retrieved on April 13, 2024. From:https://databank.worldbank.org/metadataglossary/jobs/series/FS.AST.PRVT.GD.ZS#:~:text=Long%20definition,establish%20a%20claim%20for%20repayment.

World Bank (2022). Nigeria NG: Monetary Sector Credit to Private Sector: % of GDP. Retrieved On April 18, 2024 from: https://www.ceicdata.com/en/nigeria/bank-loans/ng-monetary-sector-credit-to-private-sector--of-gdp.

World Bank (2024). Taxes and government revenue. Retrieved on April 21, 2024 from:https://www.worldbank.org/en/topic/taxes-and-government-revenue.

Zuniga, M.C., & Senbet, D. (2022). Does the effectiveness of monetary policy depend on the Choice of policy instrument? Empirical evidence from South Korea. Journal of Central Banking Theory and Practice, 2023(2), 239 – 265. https://doi.org/10.2478/jcbtp-2023-0021.