(1)

(1)Ekonomika ISSN 1392-1258 eISSN 2424-6166

2025, vol. 104(1), pp. 70–87 DOI: https://doi.org/10.15388/Ekon.2025.104.1.4

Chakir El Mehdi

Mohammed V University of Rabat, Morocco

Faculty of Legal, Economics and Social Sciences – Salé

Email: chakirelmehdi@yahoo.fr

ORCID ID: https://orcid.org/0009-0001-0696-5669

Soussi Noufail Outmane

Mohammed V University of Rabat, Morocco

Faculty of Legal, Economics and Social Sciences – Salé

Email: soussioutmane@gmail.com

ORCID ID: https://orcid.org/0000-0002-0269-7935

Abstract. This study explores perceptions of public debt management among Debt Management Offices (DMOs) in low- and middle-income countries. Based on a survey conducted in October 2023 covering 27 countries, it examines DMOs’ views on the relationship between public debt and economic growth, the practices shaping these perceptions, and the key variables influencing debt dynamics through regression modelling.

The study findings highlight that DMOs generally perceive debt as negatively impacting growth, with perceptions shaped more by professional experience than internal economic studies. Four critical variables – debt cost, economic growth, primary deficit, and governance – emerge as key influences. Notably, DMOs conducting in-house studies show more cautious assessments than those relying solely on experience or external studies. These insights provide a nuanced understanding of debt dynamics, incorporating the subjective yet practical perspectives of debt managers.

Keywords: perception of debt, public debt management, low- and middle-income countries, debt management offices, regression model.

___________

Received: 01/08/2024. Revised: 22/11/2024. Accepted: 05/01/2025

Copyright © 2025 Chakir El Mehdi, Soussi Noufail Outmane. Published by Vilnius University Press

This is an Open Access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

Public debt management has become a critical concern for governments worldwide. With debt levels reaching a record $91 trillion by the end of 2022, equivalent to 92% of the global GDP (World Bank, 2023), effective management is essential so that to maintain financial stability and support economic development. Public debt management not only affects a government’s ability to fund public services and stimulate growth but also influences long-term financial and economic security.

Understanding the perceptions of debt management agencies is crucial, as these bodies act as key advisors to governments and shape the strategic options available to policymakers (Chavanne, 2022). Although final decisions on public debt are inherently political, they are profoundly influenced by the analyses and recommendations of these administrative bodies. The perceptions held by debt managers about debt levels, economic priorities, and risk factors are therefore not only informative but also impactful. The understanding of these views provides insight into how public debt strategies are formed and implemented, thereby highlighting the indirect yet substantial influence of debt management offices on national economic decisions.

Decisions are shaped by both rational factors and cognitive influences (Schinckus, 2009), drawing on perceptions formed from the available information and knowledge (Renaut, 2006). Key questions remain: What is the perception of debt managers regarding the impact of public debt on economic growth? What are the perceived main elements influencing the debt dynamic?

These questions remain largely unexplored in the existing literature, thus making this article a new contribution to the field. As an exploratory study, it opens the way for further research and future developments to deepen our understanding of debt managers’ perceptions and their implications for public debt management.

To address these questions, this study employs a mixed-methods approach, combining a survey conducted in October 2023 with statistical and econometric analyses. By integrating descriptive insights and regression modelling, the paper provides a comprehensive understanding of DMOs’ perceptions and the variables shaping their views on public debt dynamics.

The paper is divided into four main sections. The first section outlines the theoretical and empirical framework, based on a comprehensive literature review. The second section details the methodology used in the study. The third section presents the main findings, including an attempt to model DMOs’ perceptions of the factors influencing public debt dynamics. Finally, the fourth section summarises the main conclusions and offers practical recommendations to assist governments and DMOs in refining their debt management policies and practices.

The management of public debt is a political choice that is unique to each country (Blancheton, 2019). It is guided by public debt management policy, which reflects the government’s priorities in fiscal policy (whether expansionary, austere, or balanced) and forms a core part of a broader economic strategy. In the field of debt management, while data and analysis are of great importance, the interpretation of these figures is significantly influenced by the perspectives of the individuals (Bearfield et al., 2024) and institutions involved, particularly in the absence of consensus on definitions such as debt sustainability (Laskaridis, 2021), sustainable levels, and optimal debt-to-GDP ratios (Pescatori, 2014). Without clear standards, these interpretations frequently rely on subjective perceptions as much as on objective, quantitative elements.

Debt Management Offices (DMOs) are the bodies responsible for public debt management. The function of DMOs depends on each country’s legal framework, which defines their specific responsibilities. While the specific responsibilities of DMOs may vary from one country to another, there are certain core principles that are common to all of them. As stated by the International Monetary Fund (IMF Staff, 2002), the responsibility of formulating debt management strategies and presenting them to political authorities for approval falls upon the shoulders of DMOs. The key roles of a DMO include the formulation of strategies based on risk and cost analysis, the financing of government needs, the execution of related transactions, and the consolidation and monitoring of debt operations (IMF, 1997).

Most DMOs are organised into three segments – front, middle and back offices – each with specialised functions. While typically located within the Ministry of Finance, some DMOs operate autonomously and may also provide advice to governments and produce public debt reports, depending on the legal framework and level of development of the country.

The concept of Evidence-Based Policymaking (EBPM) advocates for the utilisation of data-driven decision-making processes, as opposed to the reliance on political beliefs (Demir, 2020). The aim of EBPM is to ground policy in evidence and rational analysis, while countering partisan or arbitrary decisions that might negatively impact the State’s welfare and global interests (Carney, 2016). This is highly relevant in public debt management, where quantitative data align well with the principles of evidence and transparency.

However, it is evident that academic research is not yet fully integrated into the policy-making process (Landry et al., 2003). Nevertheless, only a small proportion of academic insights inform policy, despite the recent growth in the use of EBPM, particularly in Europe, Australia, and the United States. These developments have been driven by the frequency of crises and a desire to depoliticise public action.

In the context of public debt management, perceptions play a pivotal role in influencing strategic decision-making processes. Nobel Laureate Daniel Kahneman (2011) reveals the pervasive influence of intuitive impressions on our thinking and behaviour, and the profound impact of cognitive biases on every decision, with important implications for business strategy and economic decision-making. Hoogduin, Öztürk, and Wierts (2010) analyse the behaviour of public debt managers and explore how their actions interact with macroeconomic policies, while emphasising the significant role they play in ensuring consistency between the fiscal and monetary objectives. Gigerenzer and Gaissmaier (2011) highlight that decision-makers frequently rely on heuristics – cognitive shortcuts that simplify complex decisions – to navigate environments characterised by uncertainty or incomplete information. While these heuristics facilitate decision-making, they also influence the perception of risks and opportunities, thereby affecting the strategic directions pursued by debt management entities. This approach is particularly pertinent for debt management offices, where managers, frequently operating with incomplete data or information and economic uncertainty, are therefore required to rely on their own perceptions to inform their recommendations to government authorities. Gigerenzer and Gaissmaier’s insights demonstrate how heuristics-driven perceptions can indirectly influence economic policy decisions through the advice provided to governments, by emphasising the significance of understanding debt managers’ perceptions within this field.

Notwithstanding the insights offered by the literature review, the specific area of focus of this research remains underexplored in the currently existing studies. While a substantial body of empirical research rooted in macroeconomic econometric models has extensively analysed the impact of debt on economic growth (Gómez-Puig et al., 2018) and the determinants of debt dynamics (Cifuentes-Faura, 2024), these studies largely prioritise quantitative data and statistical interpretations. They often overlook the qualitative dimensions, such as the subjective perspectives of debt managers (Schalck, 2019), which can significantly influence policy decisions.

This research seeks to address this gap by incorporating a qualitative perspective to complement the established empirical findings. To enhance clarity and foster a deeper discussion, we shall briefly present a comparative analysis between data derived from the subjective perceptions of Debt Management Offices and econometric findings on public debt and economic growth. To ensure a comprehensive approach, the following part of the literature review will delve into specific econometric studies that have shaped our understanding of the relationship between public debt and economic growth.

For centuries, policymakers, executives, and economists have debated the evaluation of public debt and its effects on economic growth. Theoretical literature generally suggests a negative relationship between public debt and economic growth, with neoclassical growth models indicating that debt issuance to finance consumption or capital goods often slows growth. Modigliani (1936), building on Buchanan (1958), argued that national debt diminishes the private capital stock, reducing future income flows and potentially burdening future generations. While the long-term intergenerational effects remain debated, debt’s legacy – either positive or negative – depends on the applied economic theory (Keynesian or neoclassical) and influences the income redistribution predictably.

The U-shaped curve concept, describing a non-linear relationship between debt and growth, is widely acknowledged. Reinhart and Rogoff (2010) highlighted a critical 90% debt-to-GDP threshold, beyond which, debt harms growth, shaping fiscal correction policies during the financial crisis. However, their findings have been contested due to issues like sample heterogeneity. Ghosh et al. (2013), Law et al. (2021), and Makhoba et al. (2022) demonstrated that this tipping point varies based on the structural characteristics of specific countries. Markus and Rainer (2016) further emphasised that institutional features like fiscal flexibility and efficiency influence fiscal uncertainty and investment climates, contributing to the heterogeneity in how high public debt levels affect long-term growth.

The direction of the causal relationship between debt and growth has also been debated. In contrast to Reinhart and Rogoff’s view, Nersisyan and Wray (2011) argue that it is not the absolute level of public debt above a certain threshold that negatively affects growth, but rather the context of declining growth in which a weak GDP growth generates deficits and thus increases debt (Panizza, 2018).

Despite the abundance of empirical studies aiming to measure the actual impact of public debt on economic growth, the results do not provide a clear consensus. In addition to that, the influence of political and human decision-making based on perception (Cohen, West, and Aiken, 2003) adds another layer of complexity.

Given the multitude of empirical studies, and the complexity of the process of debt management, it is essential to survey those directly involved in daily debt management and responsible for it, notably, the DMOs.

To investigate debt managers’ perceptions of the impact of debt on economic growth, a quantitative study was conducted. A questionnaire with multiple sections addressing our research objective was constructed.

The sample is constituted by countries that are characterised by comparable economic issues and/or similar debt management challenges. The selection criteria were based on the World Bank’s classification of countries by income, focusing on lower-middle-income and low-income countries. A preliminary selection was then conducted based on an in-depth analysis of the economic characteristics of the aforementioned countries. European countries were excluded due to significant economic divergences and the implementation levels of their DMOs. The final sample was randomly selected by using a statistical sampling formula, with a 95% confidence interval and a 5% margin of error, resulting in an expected response count of 68 (Royer and Zarlowski, 2014).

(1)

A total of 27 responses were received ‘Tab. II’, providing a solid analysis base. Accordingly, the actual margin of error for this study is 14.75% at a 95% confidence level. It is recommended that the results should be projected to the entire population of lower-middle-income and low-income countries, with due consideration of the actual margin of error. The respondents, representing DMOs of the sampled countries, were managers or officials with comprehensive knowledge of their offices’ various functions.

The questionnaire was structured by using the hourglass technique. For this study, only parts 3 and 5 were utilised, consisting of 27 questions pertaining to the economic approach to debt management (Q23 to Q49), and 13 questions on the respondent demographics, including their country profile (Q74 to Q86) were also considered (Flower Floyd, 2009).

To ensure a uniform and unbiased understanding of the key concepts, certain definitions were clarified for the respondents. To prevent the occurrence of anchoring effects, which are often observed in online questionnaires, the response options were randomly displayed for all questions with more than four answer choices:

• Number of Observations: 27

• Number of Variables: 40

This study employed the use of Sphinx Declic software to design and distribute the questionnaire for 55 days and to analyse the results. Distribution was facilitated through personal emails and messaging apps, allowing us to reach DMO managers directly and streamline the data collection process. The questionnaire was written in French and in English in order to accommodate the official languages of the target countries. The questionnaire was pre-tested with four professionals working in a DMO, and an academic researcher, individually in face-to-face sessions. The purpose of this intermediate step was to assess the comprehension and the relevance of the questions and proposed answers, to measure the response time, and to evaluate the scope of the subject studied. The main objective of this step was to minimise potential biases such as the halo effect and contamination bias.

The respondents to the survey were predominantly managers or officials within DMOs, with a wide range of experience: 26% had less than four years of experience, 37% had between four and nine years, and 22% had over 15 years of experience. The majority held advanced qualifications, with 67% holding Master’s degrees, and 96% of the surveyed individuals occupied management roles. The responding countries varied in economic size, with 33% having a GDP below $15 billion, and 19% exceeding $120 billion. The size of the DMOs also differed, with 30% having fewer than 10 employees, while 26% operated with over 50 staff members. These characteristics highlight the diversity of the sample and its representation of DMOs operating in various economic contexts.

In an explanatory model, we seek to quantify the perceived influence of DMOs in terms of certain variables on debt dynamics. To ascertain the notion of perception, we posed the following scaled question: “In your country, how do you assess the sensitivity of debt to the factors that impact it?” We selected this variable as the primary measure of DMOs’ perception, which is explained by a set of explanatory variables, rated on the same scale by the respondents. We will adopt an econometric approach based on a multiple linear regression model. The multiple regression model is as follows:

(2)

(2)

where:

I is the dependent variable;

β0 is the constant term;

X_1, X_2,…, X_p are the independent variables (factors affecting debt dynamics);

β1, β2,…, βp are the coefficients estimating each variable’s contribution;

ε is the error term.

Once the model has been developed, we will assess the model’s robustness and parameter estimates by using statistical indicators, such as R², Fisher’s F-test, and Student’s t-test, as recommended by econometric texts on model validation (Wooldridge, 2019; Greene, 2018). This approach aligns with the exploratory objectives in which the model is developed not primarily to infer causality, but rather to achieve the best possible prediction of the dependent variable. As is common in such frameworks, the inclusion of variables is justified by empirical evidence on their predictive capacity rather than causal inference (Shmueli, 2010; Harrell, 2015).

In exploratory theoretical frameworks, regression analyses are frequently used without a strict focus on causal interpretation. The primary objective is instead to maximise the predictive accuracy of the dependent variable. In line with econometric practice, a minimum subset of independent variables is often selected to achieve the best possible fit of the model, while balancing simplicity and predictive power (Burnham and Anderson, 2002; Akaike, 1973). This approach allows empirical studies to assess the actual impact of these variables on public debt levels (for example, inflation rates, interest rates, and economic growth) even if they do not directly measure the perception of their influence on debt dynamics (Baum et al., 2013).

The selection of variables was informed by existing literature, particularly by studies by the International Monetary Fund (IMF), which emphasise factors like debt cost, initial debt stock, primary deficit, and economic growth. Other studies that informed the selection of variables include those by Reinhart and Rogoff (2010) on inflation, Olivier Blanchard (2019) on national savings, and Butkus (2018) on the balance of trade. These studies guide our choice of variables, by grounding the model in well-established empirical insights.

PERD = f(DC, PD, GDP, GOV, DS, NS, BOT, INF) (3)

where:

‘PERD’ captures DMOs’ rating of debt sensitivity to these factors, while DC reflects the perceived impact of debt cost. ‘PD’ measures the influence of the primary deficit, and ‘GDP’ captures the role of economic growth. ‘GOV’ indicates the governance quality’s effect, ‘DS’ measures the initial debt stock’s impact, ‘NS’ reflects national savings, ‘BOT’ refers to the balance of trade, and ‘INF’ represents inflation, with all components rated consistently by DMOs. Each component is rated by DMOs on a scale of 1 to 5, where ‘1’ indicates a ‘very low impact’, and ‘5’ represents a ‘very strong impact’. These ratings reflect the perceived impact of each factor on public debt, as assessed by DMOs, rather than the actual quantitative variable.

Before evaluating the perception of DMOs regarding the influence of public debt on economic growth, it was essential to gain insight into the prevailing practices within DMOs. These practices encompass an economic approach to debt management, the production of economic studies on the impact of debt on economic growth within the DMOs, and a subjective evaluation of this impact.

Given the divergent results of empirical studies, the DMO representatives were asked to provide their general perception of the debt/economic growth relationship and this same relationship within the specific context of their country.

A substantial majority (93%) of the DMO representatives surveyed concur that a causal link exists between debt levels and economic growth. This viewpoint is in accordance with the preceding empirical findings. The remaining 7% of the respondents indicated that they do not perceive a link between debt and growth. Furthermore, they proposed an optimal debt level for their respective countries, which exceeded the IMF’s recommended level by exceeding the 80% level. This high-risk appetite is contrary to the recommendations of the International Monetary Fund, particularly for countries with low or developing economies.

In terms of country-specific perceptions, 74% of the respondents indicated that they believe that their country’s current debt level has an impact on economic growth. This is, the obtained value is approximately 20% less than the general perception. This suggests that some countries have not yet reached the critical threshold identified by these experts and still have scope for manoeuvre before reaching the base of the U-curve. Of the 74% who perceive a correlation between debt and economic growth, 56% view this association as a hindrance to growth. This indicates that the prevailing level of public debt is detrimental to the country’s economic growth. A number of factors may account for this, including the absence of a leveraging effect of public debt, a high debt stock and/or high costs absorbing a significant portion of operational expenses, the diversion of debt from investment and the failure to generate the anticipated positive externalities. An alternative explanation for this result is that it reflects the cautious approach characteristic of DMO professionals, particularly with regard to cost and risk management. This could influence their perception of the debt/growth link.

DMO representatives evaluate the influence of debt on economic growth in both the general context and their respective countries, with the assessment falling within the medium to high range, as illustrated in Fig. 1. This is indicative of an impact rating between medium and high. A highly significant positive correlation between the two variables, with a p-value of less than 0.01, demonstrates the rationality and consistency in responses to both questions.

A differentiated view of the impact of debt on economic growth is held by DMOs, contingent on its origin. A majority (59%) of the respondents indicated that external debt has a more significant impact on the country’s economic growth (Gaiya et al., 2024). The potential risks associated with this type of debt are well documented. While external debt may initially appear to be an attractive financing source for countries, primarily due to generally lower costs than domestic financing (concessional financing), a smaller crowding-out effect on private sector financing, and a lower inflation risk, these benefits are offset by exchange rate risks, dependence on external financing, impact on reserve assets, and sovereignty, among others. These factors affect the country’s economy and growth. The aforementioned arguments provide insight into the prevailing sentiment regarding the impact of external debt among the sample countries.

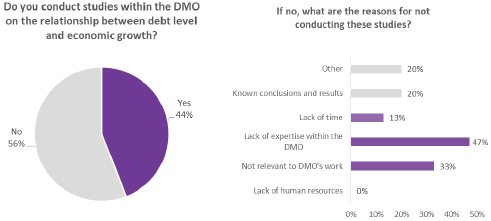

It is important to highlight that 44% of the sample reported never having read, consulted, or utilised a study specific to their own country, which would have enabled them to form a well-founded opinion on the debt/growth impact. This is especially common (50%) among DMO representatives from countries with a GDP below $15 billion. Their perceptions are largely based on professional experience and the adaptation of findings from studies not specific to their country. This observation highlights the need to explore research practices within DMOs further.

The practice of conducting economic studies – especially those investigating the link between debt and economic growth – remains uncommon among DMOs. In fact, 56% of the countries surveyed reported that their DMOs do not perform such studies (see Fig. 2). The main reasons cited are a lack of expertise within the DMO (47%) and limited interest in the DMO’s work (33%). While the shortage of expertise, often due to insufficient human resources in both quantity and skill, which is especially manifested in low-income countries’ public administrations, seems a reasonable challenge, the lack of interest poses additional questions. Many DMOs and their teams do not recognise the objectives or benefits of these studies. Additionally, 56% of the respondents whose DMOs do not conduct these studies reported that they are instead undertaken by another department within the Ministry of Finance. As previously noted, DMOs are responsible for both the strategic and operational management of public debt. However, their advice and decision-making for policymakers are significantly shaped by the leadership’s focus, especially regarding the economic perspective on debt management.

While the overall relationship between conducting studies on debt levels and economic growth and a country’s GDP level is not statistically significant, two distinct groups of countries emerge. The first group includes countries with very low GDP and those with strong GDP levels above $60 billion, categorised as low and high GDP groups. The second group consists of countries with intermediate GDPs, ranging between $15 billion and $60 billion. In this intermediate group, the relationship between debt studies and GDP level is significant, with a p-value of 0.0, supporting the alternative hypothesis and indicating a meaningful relationship between these variables, as outlined in Table I.

|

What is your country’s GDP level for the most recent closed year in billions of US Dollars? |

Do you conduct studies within the DMO on the relationship between ‘debt level and economic growth’? |

|||

|

Yes |

No |

|||

|

N |

% |

N |

% |

|

|

Low and high GDP countries |

6 |

32% |

13 |

68% |

|

Less than 15 billion USD |

3 |

33% |

6 |

67% |

|

Between 60 and 120 billion USD |

2 |

40% |

3 |

60% |

|

More than 120 billion USD |

1 |

20% |

4 |

80% |

|

Middle-GDP countries |

6 |

75% |

2 |

25% |

|

Between 15 and 30 billion USD |

4 |

80% |

1 |

20% |

|

Between 30 and 60 billion USD |

2 |

67% |

1 |

33% |

|

|

|

|||

Countries with low GDPs often face a marked shortage of resources within their public administration, partially explaining the limited engagement in debt and economic growth studies. In contrast, countries with GDPs over $60 billion typically have more structured finance ministries, complete with specialised departments dedicated to conducting and disseminating such studies. This trend aligns with the increased demand for hyper-specialisation in finance ministries as the country size and its complexity grow. For example, 80% of countries with GDPs exceeding $120 billion do not conduct these studies within their DMOs, instead relying on a specialised department within the Ministry of Finance.

Countries with intermediate GDP levels ($15 billion to $60 billion) show a stronger inclination to conduct studies on debt and economic growth. In these nations, which generally have more resources than lower-GDP countries, there is a conscious effort to add new functions, such as debt studies, to provide sufficient data and analysis. This reflects their priority of debt management for economic growth and transition toward a higher GDP status. Among these countries, more than 75% engage in such studies, while only 25% do not.

Notably, among the DMOs that conduct these studies (comprising 44% of the sample), 67% perform regular reporting and monitoring. This indicates that DMOs see value in these studies, with 63% of the respondents expressing satisfaction with the monitoring processes, thereby showing that these DMOs have effectively integrated this practice into their operations.

|

Mean |

Min |

Max |

Std. Dev. |

Skewness |

Kurtosis |

Std. Dev. Index |

|

|

Dependent |

|||||||

|

PERD |

3.963 |

3 |

5 |

0.706 |

0.046 |

-1.069 |

0.36 |

|

Explanatory |

|||||||

|

DC |

4.037 |

2 |

5 |

0.898 |

-0.375 |

-1.068 |

0.349 |

|

PD |

3.889 |

2 |

5 |

1.013 |

-0.431 |

-1.041 |

0.444 |

|

GDP |

3.704 |

2 |

5 |

0.775 |

0.047 |

-0.718 |

0.26 |

|

GOV |

3.963 |

2 |

5 |

1.126 |

-0.554 |

-1.213 |

0.506 |

|

DS |

3.296 |

1 |

5 |

0.912 |

-0.289 |

-0.034 |

0.216 |

|

NS |

3.185 |

1 |

5 |

1.21 |

-0.341 |

-1.01 |

0.381 |

|

BOT |

3.444 |

1 |

5 |

1.188 |

-0.205 |

-1.176 |

0.367 |

|

INF |

3.815 |

2 |

5 |

1.039 |

-0.239 |

-1.29 |

0.468 |

Hypothesis tests are necessary for the different variables in the model. The impact of debt cost, primary deficit, and initial debt stock should positively influence the debt growth and thus its sensitivity to these same factors. National savings, trade balance, economic growth, and inflation positively impact debt and contribute to its management. The expected sign for this group of variables is negative; see Table III.

|

Variables |

Measures |

Coef. |

Expected Signs |

|

Perception of debt cost impact |

Rating on a scale of 5 (very low to very high) |

β1 |

Positive (+) |

|

Perception of primary deficit |

β2 |

Positive (+) |

|

|

Perception of economic growth impact |

β3 |

Negative (-) |

|

|

Perception of governance impact |

β4 |

Negative (-) |

|

|

Perception of initial debt stock impact |

β5 |

Positive (+) |

|

|

Perception of national savings impact |

β6 |

Negative (-) |

|

|

Perception of balance of trade impact |

β7 |

Positive (+) |

|

|

Perception of inflation impact |

β8 |

Negative (-) |

The validation tests for the model estimations are of great importance in order to validate the hypotheses underlying the use of the multiple linear regression model. In order to ensure the robustness of the results obtained, it is essential to verify the absence of correlation between the explanatory variables and to validate the Fisher’s and Student’s tests.

|

PERD |

DC |

PD |

GDP |

GOV |

DS |

NS |

BOT |

INF |

|

|

PERD |

- |

||||||||

|

DC |

0.67 |

- |

|||||||

|

PD |

0.532 |

0.385 |

- |

||||||

|

GDP |

0.401 |

0.237 |

0.152 |

- |

|||||

|

GOV |

-0.292 |

-0.265 |

-0.105 |

0.295 |

- |

||||

|

DS |

-0.102 |

-0.014 |

-0.005 |

-0.252 |

-0.438 |

- |

|||

|

NS |

-0.082 |

-0.042 |

0.08 |

0.102 |

0.288 |

0.088 |

- |

||

|

BOT |

-0.025 |

-0.052 |

-0.277 |

0.274 |

0.329 |

-0.126 |

0.101 |

- |

|

|

INF |

0.148 |

0.296 |

0.126 |

0.263 |

-0.006 |

0.101 |

0.028 |

0.568 |

- |

It is imperative that explanatory variables should be non-collinear. The correlation matrix above Table V indicates a weak link between the variables. The standardised Cronbach’s alpha is low (0.48), which indicates that the conditions of independence of the explanatory variables are well satisfied.

The analysis of the relationship between the perception of public debt sensitivity to influencing factors and the unitary assessment of each factor’s impact reveals four key variables influencing the explanatory variable at the 5% threshold. These are, in the order of impact, the debt cost (interest rate), economic growth, primary deficit, and governance; see Table IV.

The specified model explains 69.86% of the variance in the dependent variable. The model quality indicators are indicated in Table V.

|

Coef. |

Student statistic |

Std. Coef. |

Contribution |

VIF |

|

|

Constant |

1.796* |

1.914 |

|||

|

DC |

0.346** |

2.788 |

0.44 |

20.236 |

0.246 |

|

PD |

0.284* |

2.082 |

0.312 |

14.359 |

0.209 |

|

GDP |

0.271** |

2.515 |

0.389 |

17.881 |

0.23 |

|

GOV |

0.163* |

1.424 |

0.275 |

12.635 |

0.185 |

|

DS |

-0.02 |

0.246 |

-0.035 |

-1.6 |

0.165 |

|

NS |

-0.083 |

0.692 |

-0.107 |

-4.939 |

0.169 |

|

BOT |

-0.177 |

1.412 |

-0.26 |

-11.972 |

0.184 |

|

INF |

-0.223* |

2.041 |

-0.356 |

-16.378 |

0.207 |

|

R |

0.84*** |

||||

|

R² |

0.69 |

||||

|

Fisher |

5.21*** |

Based on the above results, the model estimation can be derived as follows:

PERD = 1.796 + 0.346* DC + 0.284 * GDP + 0.271 * PD + 0.163 * BOT – 0.02 * NS – 0.083 * DS – 0.177 * INF – 0.223 * GOV (4)

Based on these observations, there is a strong correlation between four variables and the perception of debt sensitivity by DMOs. The hypotheses concerning the signs of the coefficients β are verified for six out of eight variables. However, the direction of the correlation for economic growth and initial debt stock is not confirmed. This discrepancy may be due to sluggish growth in several countries in the sample, which does not allow for a decrease in the debt ratio or significantly impact it. Indeed, the slowdown in the global economic growth, particularly in the sample countries, may have influenced the DMOs’ responses, suggesting that the threshold at which economic growth reduces debt sensitivity is not or is no longer being reached. For the remaining influential variables, the regression results provide nuanced insights into the determinants of public debt sensitivity and align with a substantial body of empirical literature. For instance, the confirmation of the role of the debt cost and the primary deficit corroborates findings by Reinhart and Rogoff (2010), Debrun (2019) and Goodwin et al. (2022), emphasising their critical impact on debt accumulation. The primary deficit is the first budgetary aggregate directly linked to the creation of new debt (Goodwin et al., 2022). Indeed, primary financing needs in State budgets, voted during annual budget or generated during the current year’s budget execution, are covered by issuing new debts (domestic and external).

DMOs are aware of the importance of debt management, as they are on the front line in daily debt management and provide their expertise and advice to the political authorities in place. Consequently, they place considerable importance on governance. At this level, debt governance should be understood in a broad sense. This includes a direct link through the legal and regulatory framework in place, transparency and ethical rules, mandates granted to DMOs, and an indirect link through the efficiency of investments financed by debt. This aligns with the results of Betin and Fournier (2018), who demonstrated that government effectiveness, as measured by a general perception indicator, is the main factor of sovereign default (Bolton et al., 2023).

However, other variables that the respondents did not perceive as significantly contributing to public debt sensitivity are aggregates which do not have a direct and intuitive link to public debt, despite substantial macroeconomic evidence suggesting otherwise. In particular, the respondents did not identify variables such as national saving and the trade balance, which have been highlighted as influential in studies such as Blanchard (2019) and Butkus et al. (2018). This discrepancy invites a deeper investigation into why these variables are undervalued in the perceptions of DMOs. Possible reasons could include limited access to or use of advanced economic analysis by certain DMOs, differences in the prioritisation of immediate versus long-term fiscal factors, or a mismatch between theoretical models and practical debt management frameworks. These gaps underscore the importance of bridging empirical research and practical governance to improve the identification and recognition of critical determinants of debt sensitivity.

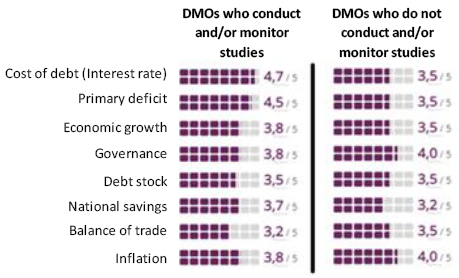

It is of importance to note a significant disparity in the perception of the impact of certain variables between DMOs who conduct economic studies and follow academic research and those who do not incorporate these mechanisms. The ratings given by the latter are slightly below the sample’s average and significantly lower than those of DMOs conducting economic studies; see Fig. 3. As the perception of elements depends on the stimuli received and interpreted by individuals and organisations, it can be posited that the greater is the number of DMOs who conduct, follow, or utilise economic studies, the more they consider that elements affecting public debt to be impactful. This is particularly evident in the case of debt cost, primary deficit, economic growth, and national savings. A number of different interpretations can be made to explain this result. These include the pervasive principle of prudence that underlies most studies, which is also recommended by the World Bank and IMF (Guidelines for Public Debt Management, 2002). Another interpretation is that economic studies provide DMOs on the country’s overall macroeconomic situation, which allows for a more inclusive risk approach.

The findings from this study highlight crucial policy implications, especially emphasising the need for policymakers to carefully consider the subjective assessments of Debt Management Offices (DMOs) when designing debt management strategies. Given that DMOs possess specialised expertise and direct oversight in debt operations, their perspectives inevitably shape the debt policy. However, the study reveals that these assessments are largely grounded in experience and practical knowledge rather than systematic research or data-driven analysis. This reliance on subjective judgment can introduce variability and potential bias, which, if unchecked, might influence national debt strategies in ways that could affect long-term economic stability.

Policymakers, therefore, must be vigilant and critically aware of the subjective nature of DMOs’ assessments. While DMOs’ expertise is invaluable, an over-reliance on personal judgment could skew decision-making, especially in contexts where comprehensive empirical analysis is lacking. To mitigate this, it is essential to strengthen Evidence-Based Policy-Making approaches within DMOs, while fostering a systematic reliance on empirical data to guide debt management decisions. Such an approach would enable debt strategies to be more resilient, thus reducing the likelihood of decisions shaped by individual perceptions and biases, which, although unavoidable to some degree, should be minimised. By embedding EBPM practices, DMOs can anchor their assessments in rigorous data, creating a more balanced approach that would combine professional judgment with solid empirical foundations.

Furthermore, the study identifies a perceptual divergence among DMOs which reveals potential inconsistencies in debt management approaches, despite similar economic conditions across low- and lower-middle-income countries. Although countries in these income brackets share many common debt challenges, the study shows that DMOs’ perceptions vary significantly. This discrepancy highlights the risk of disparate policy applications in countries where the IMF and World Bank often implement relatively uniform strategies and solutions. Given that these countries are typically treated as a cohesive group, it is critical that their debt policies are informed by a unified understanding of debt dynamics which transcends individual biases within DMOs.

The findings from this exploratory study provide an initial overview of perceptions within public debt management entities in a sample of low- and lower-middle-income countries regarding the economic approach to debt and the relationship between debt and economic growth. Conducted among 27 countries classified by the World Bank as low- or lower-middle income, our study has confirmed that there is a cautious perception within DMOs of the link between debt and economic growth, with a perceived negative impact. This perception is primarily based on the experience and practice of debt managers rather than on studies conducted within the DMOs, as evidenced by the low rate of utilisation or exploitation of such studies by DMOs.

However, the elements considered as impacting the debt dynamics of countries are the main points we find in most empirical studies on the subject. Indeed, four variables strongly explain the DMOs’ perception of debt dynamics: the cost of debt, economic growth, the primary deficit, and governance. There is a notable gap between the perception of DMOs that conduct or follow studies on debt and economic growth within their organisations and those who do not perform such studies. The former group tend to be more cautious in their assessments, whereas the latter group tends to be more permissive.

This study represents a preliminary step that should be enriched by further research based on the results obtained. It also presents certain limitations that future research should address to enhance robustness and depth.

Firstly, as an exploratory quantitative study, this research captures broad trends in DMOs’ perceptions but lacks the detailed contextual understanding that qualitative methods could provide. Future studies could benefit from incorporating qualitative approaches, such as individual interviews or focus groups, to delve into the reasoning behind certain responses. Engaging directly with the respondents would allow researchers to explore the motivations and contexts influencing their views, thereby uncovering the logic and orientation driving their assessments of debt thresholds and economic growth impacts. This approach would also help clarify any ambiguities in the interpretation of survey questions, particularly where responses may vary according to distinct national or institutional contexts.

Secondly, an expansion of the sample size to include more countries would improve the robustness of the findings, by enhancing both the representativeness and generalisability of the results. A larger sample would reduce the margin of error, ideally reaching the target of a 5% margin of error, thereby enabling the study to approach a level of exhaustiveness that would strengthen its contributions to the field. Such an expanded sample would also allow for more reliable cross-regional comparisons, helping to determine whether DMOs’ perceptions differ systematically across varying economic contexts and institutional frameworks.

Akaike, H. (1973). Information theory and an extension of the maximum likelihood principle. In Proceedings of the Second International Symposium on Information Theory, 267-281. https://doi.org/10.1007/978-1-4612-1694-0_15

Baum, A., Checherita-Westphal, C., & Rother, P. (2013). Debt and growth: New evidence for the euro area. Journal of International Money and Finance, 32, 809-821. https://doi.org/10.1016/j.jimonfin.2012.07.004

Bearfield, C. X., van Weelden, L., Waytz, A., & Franconeri, S. (2024). Same data, diverging perspectives: The power of visualizations to elicit competing interpretations. IEEE Transactions on Visualization and Computer Graphics, 30(6), 2995–3007. https://doi.org/10.1109/TVCG.2024.3388515

Blanchard, O. (2019). Public debt and low interest rates. American Economic Review, 109(4), 1197-1229. https://doi.org/10.1257/aer.109.4.1197

Blanchard, O., Gopinath, G., & Rogoff, K. (2021). Discussion on public debt and fiscal policy. IMF Economic Review, 69, 258-274. https://doi.org/10.1057/s41308-020-00116-2

Blancheton, B. (2019). Prendre la mesure de la dette publique. Dans La dette publique : Ses mécanismes, ses enjeux, ses controverses (pp. 17-38). Paris : La Découverte.

Bolton, P., Gulati, M., & Panizza, U. (2023). Sovereign debt puzzles. Annual Review of Financial Economics, 15, 239-263. https://doi.org/10.1146/annurev-financial-111620-030025

Buchanan, J. M. (1958). Public principles of public debt. Homewood, Illinois.

Burnham, K. P., & Anderson, D. R. (2002). Model Selection and Multimodel Inference: A Practical Information-Theoretic Approach. Springer. DOI: https://doi.org/10.1007/b97636​

Butkus, M., & Seputiene, J. (2018). Growth effect of public debt: The role of government effectiveness and trade balance. Economies, 6(4), 62. https://doi.org/10.3390/economies6040062

Cairney, P. (2016). Chapter 2. In The politics of evidence-based policy making (pp. 13–50). Palgrave Pivot London. https://doi.org/10.1057/978-1-137-51781-4

Chavanne, D. (2022). Debt perceptions: fairness judgments of debt relief for individuals and countries. Behavioral Public Policy, 6(2), 283-302. https://doi.org/10.1017/bpp.2019.21

Cifuentes-Faura, J., & Simionescu, M. (2024). Analyzing the importance of the determinants of public debt and its policy implications: A survey of literature. Public Finance Review, 52(3), 345-375. https://doi.org/10.1177/10911421231215019

Cohen, J., Cohen, P., West, S. G., & Aiken, L. S. (2003). Applied multiple regression/correlation analysis for the behavioral sciences (3rd ed.). Lawrence Erlbaum Associates Publishers.

Debrun, X., Ostry, J., Willems, T., & Wyplosz, C. (2019). Public debt sustainability. International Monetary Fund.

Demir, F. (2020). Evidence-Based Policy-Making: Merits and Challenges. In: Farazmand, A. (eds) Global Encyclopedia of Public Administration, Public Policy, and Governance. Springer, Cham. https://doi.org/10.1007/978-3-319-31816-5_3901-1

Fournier, J. M., & Bétin, M. (2018). Limits to government debt sustainability in middle-income countries. OECD Economics Department Working Papers, 1493. OECD Publishing. https://doi.org/10.1787/deed4df6-en

Gaiya, B. A., Akintola, A. A., & Akpan, U. (2024). External debt, institutions, and economic growth: New evidence from emerging markets and low-income countries. Journal of Social and Economic Development. https://doi.org/10.1007/s40847-024-00363-3

Ghosh, A., Kim, J., Mendoza, E., Ostry, J., & Qureshi, M. (2013). Fiscal fatigue, fiscal space and debt sustainability in advanced economies. Economic Journal, 123(566), F4-F30.

Goodwin, N., Harris, J. M., Nelson, J. A., Rajkarnikar, P. J., Roach, B., & Torras, M. (2022). Deficits and debt. In Macroeconomics in context (4th ed., pp. 29). Routledge. https://doi.org/10.4324/9781003251521

Gómez-Puig, M., & Sosvilla-Rivero, S. (2018). Public debt and economic growth: Further evidence from the euro area. Acta Oeconomica, 68(2), 209-229. https://doi.org/10.1556/032.2018.68.2.2

Harrell, F. E. (2015). Introduction. In Regression modeling strategies. Springer Series in Statistics. Springer, Cham. https://doi.org/10.1007/978-3-319-19425-7_1

Hoogduin, L., Öztürk, B., & Wierts, P. (2010). Public debt managers’ behaviour: Interactions with macro policies. (DNB working paper; No. 273). De Nederlandsche Bank. https://doi.org/10.3917/reco.626.1105

International Monetary Fund. (1997). Coordinating public debt and monetary management. International Monetary Fund. https://doi.org/10.5089/9781557755551.071

International Monetary Fund Staff. (2002). Guidelines for Public Debt Management. Joint Publication of IMF and World Bank.

Jean-Marc Fournier & Manuel Bétin (2018). “Limits to government debt sustainability in middle-income countries,” OECD Economics Department Working Papers 1493, OECD Publishing. DOI: 10.1787/deed4df6-en

Laskaridis, C. (2020). More of an art than a science: The IMF’s debt sustainability analysis and the making of a public tool. Œconomia, 10-4 | 2020, 789-818. https://doi.org/10.4000/oeconomia.9857

Law, S. H., Ng, C. H., Kutan, A. M., & Law, Z. K. (2021). Public debt and economic growth in developing countries: Nonlinearity and threshold analysis. Economic Modelling, 98, 26-40. https://doi.org/10.1016/j.econmod.2021.02.004

Makhoba, B. P., Kaseeram, I., & Greyling, L. (2022). Asymmetric effects of public debt on economic growth: Evidence from emerging and frontier SADC economies. Cogent Economics & Finance, 10(1). https://doi.org/10.1080/23322039.2022.2046323

Modigliani, F. (1961). Long-run implications of alternative fiscal policies and the burden of the national debt. Economic Journal, 71(284), 730-755.

Panizza, U. (2018). Nonlinearities in the relationship between finance and growth. Comparative Economic Studies, 60, 44-53. https://doi.org/10.1057/s41294-017-0043-3

Panizza, U., & Presbitero, A. F. (2014). Public debt and economic growth: Is there a causal effect? Journal of Macroeconomics, 41, 21-41.

Pescatori, A., Sandri, D., & Simon, J. (2014). Debt and growth: Is there a magic threshold? IMF Working Paper, WP/14/34. International Monetary Fund.

Presbitero, A. F. (2012). Total public debt and growth in developing countries. The European Journal of Development Research, 24(4), 606-626.

Reinhart, C. M., & Rogoff, K. S. (2010). Growth in a time of debt. American Economic Review, 100(2), 573-578.

Renaut, A. (2006). Chapitre 2. La perception. Dans J. Billier, P. Savidan & L. Thiaw-Po-Une (Dir.), La Philosophie (pp. 42-56). Paris: Odile Jacob.

Schalck, C. (2019). Investigating shifts in public debt management behaviour in France. Economics Bulletin, 39(2), 1656-1665.

Schinckus, C. (2009). La finance comportementale ou le développement d’un nouveau paradigme. Revue d’Histoire des Sciences Humaines, 20, 101-127. https://doi.org/10.3917/rhsh.020.0101

Shmueli, G. (2010). To explain or to predict? Statistical Science, 25(3), 289-310. https://doi.org/10.1214/10-STS330

Wooldridge, J. M. (2019). Introductory econometrics: A modern approach. Cengage Learning.

World Bank. (2023). International Debt Report 2023.