Ekonomika ISSN 1392-1258 eISSN 2424-6166

2025, vol. 104(2), pp. 111–128 DOI: https://doi.org/10.15388/Ekon.2025.104.2.7

Ugur BELLIKLI

Giresun University, Alucra Turan Bulutcu Vocational High School, Türkiye

Email: ugur.bellikli@giresun.edu.tr

ORCID: https://orcid.org/0000-0002-4571-6200.

Abstract. The aim of this study is to examine the impact of leverage and debt cost which were substantiated as the factors of financial constraints, and the interest coverage ratio which was substantiated as financial distress of Turkish firms listed on the BIST MAIN Index on events after the reporting period. To achieve this aim, panel data analysis was conducted on 112 companies listed in the relevant index between 2014 and 2023. The dependent variable is disclosure after the reporting period, while the independent variables are leverage, cost of debt (financial constraints), and the interest coverage ratio (financial distress). The research findings show that high debt levels (particularly short-term debt) and financial distress increase the number of events after the reporting period. The findings can be interpreted as suggesting that Turkish firms experiencing financial constraints and distress may be more likely to engage in creative accounting practices to enhance the appearance of their financial statements.

Keywords: Accounting disclosure, events after the reporting period, financial constraints and distress.

__________

Received: 18/12/2024. Revised: 01/03/2025. Accepted: 22/03/2025

Copyright © 2025 Ugur Bellikli. Published by Vilnius University Press

This is an Open Access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

The aim of general-purpose financial reporting is to provide financial information about the reporting entity to help the current and potential investors, lenders, and other creditors make resource allocation decisions (CFFR, 1.2). Accurate interpretation of financial statements is the main way for external investors, creditors, as well as any other stakeholders, to gain insights into a company. These reports are relied upon by users to assess a company’s financial health, profitability, and growth potential. This reliance enables users to make informed investment decisions, compare the company’s performance with its competitors, and evaluate the value of their investments. Therefore, the accuracy and reliability of the financial information in the reports will – both directly and indirectly – impact on the decisions of these users.

On the other hand, events after the reporting period (the balance sheet date) refer to those events, which, whether favorable or unfavorable to the entity, occur between the end of the reporting period and the date the financial statements are approved for issuance (IAS 10.3). According to the relevant accounting standard, events occurring after the reporting period are classified into two categories: (1) adjusting events versus (2) non-adjusting events. An event is considered an adjusting event if evidence of its occurrence after the balance sheet date is identified and presented; otherwise, it is classified as a non-adjusting event (IAS 10.3). If events occur after the balance sheet date, they must be disclosed with accompanying explanations at the end of the entity’s balance sheet. Disclosures made after the reporting period may reveal that some financial information in previous statement(s) was inaccurate. Consequently, these disclosures can cast doubt on the reliability of the financial statements. Correcting such accounting errors may change investors’ views on the company’s past performance or future expectations. Low-quality information has the potential to mislead investors and impede the efficient allocation of resources in capital markets (Martínez-Sola et al., 2024).

Compared to other countries, Türkiye’s adoption level of IFRS is close to that of developed economies. However, some countries, such as EU member states, have implemented IFRS for a longer period, which has led to differences in practical applications. Notably, countries like the United States apply their own standards instead of IFRS. Türkiye’s alignment with IFRS is strategically important for attracting global investments and increasing transparency in international financial reporting. The disclosure of events after the reporting period increased in the late 1990s and became widespread in the early 2000s. In Türkiye, there has been a significant rise in their frequency, especially after the adoption of accounting standards in 2006, which aimed to align with the global accounting practices. The increasing number of disclosures regarding events after the reporting period has raised concerns among regulators, legal authorities, creditors, auditors, and investors about the quality of the accounting information (Olusola and Abdulasisi, 2020).

These disclosures, whether correcting intentional or unintentional errors, have led investors to question the reliability of financial statements. Studies suggest that post-reporting disclosures can serve as earnings management tools (Martínez-Sola et al., 2024). In Türkiye, COVID-19 caused revenue losses, bankruptcy risks, and liquidity issues, raising short-term debts. While the Government support offered temporary relief, fixed asset values declined, inventory management became difficult, and the supply chains were disrupted. Many businesses increased borrowing and reassessed their risk management and insurance strategies. In short, these situations may increase the number of events after the reporting period in financial reporting because they financially constrain and distress businesses.

Extensive studies have been conducted on the impact of disclosures regarding events after the reporting period, especially concerning the firm value of publicly traded companies. A significant portion of these studies provide evidence that such disclosures are not well received by investors. Additionally, studies have examined the impact of disclosures of events after the reporting period on the credibility of companies. These studies have empirically shown that such disclosures increase companies’ costs. The studies in question report that disclosures of events after the reporting period increase the cost of equity, negatively impact the cost of bank loans, and may compel companies to rely on the secondary credit market (Hribar and Jenkins, 2004; Graham et al., 2008; Park and Wu, 2009). Previous research has explored the impact of such disclosures on debt costs (Richardson et al., 2002), while an opposing perspective has emerged in the international literature (Martínez-Sola et al., 2024). However, this topic has not yet been addressed in Türkiye. In particular, the impact of the borrowing costs and leverage ratios on the disclosure of events after the reporting period presents an important research topic. This study empirically investigates the existence of such a relationship, particularly in Türkiye, where the global accounting standards are still relatively newly adopted.

This study aims to examine how financial constraints and distress influence companies’ disclosures of events after the reporting date. The key research questions in this context include: What is the relationship between the debt levels and the post-reporting event disclosures? Do companies with high leverage, especially those with a significant short-term debt, disclose more events? Additionally, does financial distress impact the disclosure of events after the reporting period?

The present study contributes to the accounting literature by exploring whether high borrowing costs and debt levels drive companies to disclose post-reporting events. It offers empirical insights into how firms aim to present more acceptable financial statements to creditors. The study examines the relationship between leverage ratios and post-reporting disclosures, suggesting that highly indebted firms, particularly those with a high short-term debt, may disclose more events so that to improve their financial appearance. A low interest coverage ratio may signal aggressive accounting practices. Unlike research on developed common-law countries, this study focuses on Türkiye, where investor protections are weaker (Im et al., 2024). Since 2013, Türkiye’s financial sector has faced volatility due to U.S. monetary shifts (Çekin, 2019), thereby increasing reliance on accounting data and the likelihood of financial manipulation.

The next section of the study discusses the literature on financial constraints and distress, and, based on its findings, research hypotheses shall be developed. In the following section, the study’s sample, the variables used in the research, and the empirical results shall be presented. The study concludes with a section discussing the research results.

The disclosures after the reporting period are essentially aimed at correcting the inaccuracies of the information on which financial statement users rely in their decision-making process in order to protect them (Ahmadi et al., 2013). However, this situation not only impacts the reliability of financial statements, but can also negatively affect the reputation of the company management.

Initially, some earlier studies were focusing on examining the effects of events after the reporting period on the stock market, particularly by focusing on analyzing their impact on the stock price depreciation, the cost of capital, and the cost of equity (Hribar and Jenkins, 2004; Efendi et al., 2007; Hennes et al., 2008; Burks, 2010; Bardos and Mishra, 2014; Chen et al., 2014; Hu et al., 2024). Empirical evidence presented in these studies suggests that the disclosure of events occurring after the reporting period leads to a decline in the firm value, higher capital costs, and a negative impact on the stock prices. It has also been stated that a company’s disclosure of events after the reporting period can lead to financial distress, thereby harming its corporate reputation (Wu et al., 2016). On the other hand, there are also studies providing evidence on the effects of events after the reporting period on borrowing costs. One of these studies compared loan applications made to banks before and after the disclosure of events after the reporting period. It was found that, compared to applications initiated before the disclosures, loan applications submitted after the disclosures were offered higher interest rates, shorter terms, increased collateral requirements, and more restrictive covenants in the loan agreements (Graham et al., 2008). It has also been stated that the information asymmetry created by the disclosure of events occurring after the reporting period prompts banks to establish stricter conditions in loan agreements, as it increases the risk of default.

In line with the literature presented above, this study aims to contribute a new perspective to the relationship between the disclosure of events after the balance sheet date and the corporate finance. In contrast to the literature studies, this research does not focus on the financial outcomes of disclosing events after the balance sheet date; instead, it examines the relationship between disclosures versus financial constraints and distress. It is hypothesized that companies with a history of financial constraints are more likely to disclose events occurring after the balance sheet date (Campa and Camacho-Minano, 2015). Additionally, studies have shown that companies frequently disclosing events after the balance sheet date tend to have a greater need for external financing compared to those which do not disclose events occurring after the balance sheet date as frequently (Richardson et al., 2002). In the light of these explanations, it can be suggested that when companies find themselves under financial pressure, this may lead to an increase in the number of disclosures of events after the reporting period, potentially resulting in aggressive accounting practices. It is also worth noting that there is empirical evidence from studies suggesting that such pressures on company management lead to inflating earnings as well as earnings management practices (García Lara et al., 2009; Jones, 2011; Beneish et al., 2012; Farrell et al., 2014; Campa and Camacho-Minano, 2015; Bowen et al., 2018; Kurt, 2018; Reinhart, 2022; He and Ren, 2023; Butkevičius, 2020).

Another factor placing financial pressure on firms is uncertainty, and particularly economic policy uncertainty. A study conducted in the United States examined the relationship between the quality of financial reporting of publicly traded companies and economic policy uncertainty. Empirical evidence indicates that the relationship between these two variables is positive, and this relationship is more pronounced in financially constrained and distressed companies (Bermpei et al., 2022). Additionally, studies on the effects of uncertainty and economic policy uncertainty on asset pricing, options contracts, capital investments, corporate cash flows, corporate renewal investments, and accounting conservatism perceive these factors as financial pressure on companies (Drechsler, 2013; Neamtiu et al., 2014; Bloom, 2014; Goodell et al., 2021; Cui et al., 2021; Cui et al., 2023; Atasel et al., 2020). Considering previous studies and the statements made, it is believed that financial constraints will encourage companies to disclose after the reporting period more frequently. It can be stated that the likelihood of this argument being validated is particularly high among companies suffering from high borrowing costs (in terms of both short-term and total debts). It can be stated that a financially constrained and distressed company may resort to aggressive accounting practices in order to improve its financial appearance and thereby avoid difficulties in securing external financing. This situation may result in the disclosure of events occurring after the balance sheet date. Based on the presented literature, two hypotheses have been proposed to test the impact of financial constraints and distress on the likelihood of disclosing events after the balance sheet date.

First, the likelihood of a financially constrained firm, due to a high leverage ratio, reorganizing its financial statements has been analyzed. Indeed, previous empirical evidence has shown that a high leverage ratio poses a significant risk of bankruptcy, which is likely to lead to financial distress (Wu et al., 2016; Zhang et al., 2018). Therefore, this study has chosen the leverage ratio to represent financial constraints or distress. Credit obligations to banks and financial institutions constitute another aspect of this study. Companies with a high tendency to disclose post-reporting events have a greater bank credit debt than those with lower disclosure rates. Firms with higher debt levels are more likely to report such events, engage in earnings management, and seek low-cost external financing to manipulate earnings (Richardson et al., 2002). Similarly, these companies often have higher unpaid debt, rely on external financing, and hold significant cash or similar assets (Efendi et al., 2007).

Another relevant aspect is the role of financial covenants in limiting companies’ borrowing capacity or maintaining a balanced debt-to-equity ratio. For this reason, companies with high leverage ratios are more likely to manipulate their accounting figures so that to avoid breaching these covenants. Empirical studies providing evidence on this topic have shown that debt covenants influence accounting policy choices, with the companies that breach these covenants tending to adopt income-increasing accounting practices (Badertscher and Burks, 2011). Companies with high leverage ratios are believed to be more likely to make discretionary accounting adjustments, thus increasing the likelihood of post-reporting event disclosures.

As previously noted, as the amount of short-term debt in a company increases, the financing risk also progressively rises. Therefore, it has been investigated whether companies with a habit of reporting events after the reporting period are primarily those with high levels of short-term debt (Butkevičius, 2020). The shorter is the debt maturity, the greater is the likelihood of these companies facing refinancing risk, in addition to potential covenant breaches; therefore, their probability of repeated disclosures is expected to be higher. Additionally, a high level of short-term debt in a company negatively impacts its credit rating, which, in turn, increases its borrowing costs and restricts access to refinancing options.

Another dimension of financial constraints is the cost of borrowing. Borrowing costs are one of the barriers to the sustainability and increase of external financing. It is argued that companies with a greater need for external financing in capital markets are more likely to engage in misleading reporting with the objective to reduce their borrowing costs (Burns and Kedia, 2006). Since manipulation in earnings with the intent to borrow at a lower cost may be a primary objective for financially constrained companies, this can lead to aggressive accounting practices, which, in turn, may result in the disclosure of events occurring after the reporting date (Richardson et al., 2002).

Accounting consistency means the use of the same methods unless necessary, with any changes disclosed. Firms may accept higher interest rates to stay within debt covenants (Jin et al., 2023). Financially constrained firms may adjust policies to avoid covenant breaches and secure financing. Highly leveraged firms are more likely to disclose post-reporting events due to the need for restructuring.

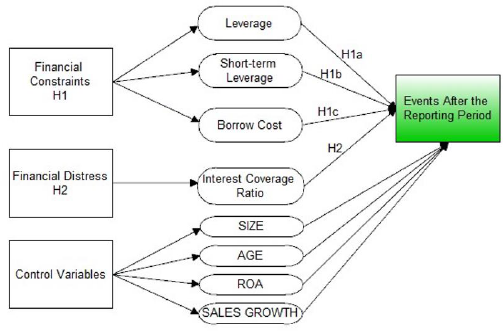

Within the framework of all the aforementioned points, financial constraints have been formulated as three sub-hypotheses:

H1a: The high level of total leverage increases the number of events after the reporting period.

H1b: The high level of short-term leverage increases the number of events after the reporting period.

H1c: The high level of borrowing cost increases the number of events after the reporting period.

The second hypothesis examines the link between financial distress and post-reporting disclosures. Financial distress manifests through high debt, costly borrowing, losses, or bankruptcy risks. Struggling firms are more likely to manipulate earnings. While complex indexes exist, this study uses a simpler, literature-based approach (Campa and Camacho-Minano, 2015). A key distress indicator is a firm’s inability to cover interest expenses with operating profits, which can lead to delays, defaults, or bankruptcy. Thus, the second hypothesis is outlined as:

H2: The low level of interest coverage ratio (financial distress) increases the number of events after the reporting period.

The initial sample included 2,030 firm-years from 203 companies listed on the BIST MAIN index, covering a 10-year period. The aim was to collect firm data from audited financial statements on Türkiye’s Public Disclosure Platform. However, banks and financial institutions were excluded due to the different reporting methods they employ. To create balanced panels, only the years 2014–2023 were considered, thus excluding all firms established after 2014. Firms with extreme values were also removed. After these adjustments, the final dataset consisted of 1,120 observations from 112 firms over 10 years.

This section of the study addresses the research variables, their definitions, and how these variables are measured. The disclosure of events after the reporting period was taken as the dependent variable. This dependent variable is represented as a dummy variable (assigned a value of ‘1’ if the firm made disclosures after the reporting period in the relevant year, and ‘0’ otherwise).

Based on the literature discussed in the previous section, the explanatory variables which were thought to have an impact on the dependent variable include leverage, short-term leverage, borrow cost, and financial distress, which is also represented by a dummy variable.

The control variables used in the research are also based on various characteristics of the firms. Considering previous literature, it has been shown that active profitability, size, the firm’s age, and its annual growth are significant factors between the firms that frequently disclose events after the reporting period versus those which do not (Olusola and Abdulasisi, 2020). Indeed, similarly, it has been determined that there are differences in profitability, growth, and size between firms with a frequent habit of disclosing events after the reporting period and those not manifesting such a trend (Mehanna and Soliman, 2023). Additionally, Alyousef and Almutairi (2010) have proven that firms that disclose events after the reporting period more frequently are more likely to be smaller, older, and more profitable.

In accordance with the explanations above and the hypotheses established in the related literature section, the research model in the study has been constructed as shown in Figure 1.

In the study, the definitions and measurement methods of the variables specified in the research model are presented in Table 1.

|

Variables |

Definitions |

Measurements |

|

DISC |

Disclosure of Events after the Reporting Period. |

If the company disclosed an event after the reporting period, it is assigned a value of ‘1’; otherwise, ‘0’ is assigned. |

|

LEVE |

Total Leverage |

Total liabilities/Equity. |

|

STLEVE |

Short Term Leverage |

Short-term liabilities/Equity. |

|

BC |

Borrow Cost |

Financial expenses/Long-term creditors+Financial debts. |

|

FD |

Financial Distress |

Takes the value ‘1’ if the firm’s operating profit is lower than its interest expenses and ‘0’ otherwise. |

|

SIZE |

Firm Size |

Log(Total assets). |

|

AGE |

Firm Age |

Log(Years since the company was founded). |

|

ROA |

Return on Asset |

Operating income/Total assets. |

|

SG |

Sales Growth |

The percentage change in sales between the current year and the previous year. |

The aim of this research is to investigate whether financial constraints and distress affect firms’ disclosure of events after the reporting period. To achieve this aim, four separate panel regression models have been developed, as outlined below.

DISCit=β0+β1LEVEit+β2SIZEit+β3AGEit+ β4ROAit+ β5SGit+ λt +Is +еit (1)

DISCit=β0+β1STLEVEit+β2SIZEit+β3AGEit+ β4ROAit+ β5SGit+ λt +Is +еit (2)

DISCit=β0+β1BCit+β2SIZEit+β3AGEit+ β4ROAit+ β5SGit+ λt +Is +еit (3)

DISCit=β0+β1FDit+β2SIZEit+β3AGEit+ β4ROAit+ β5SGit+ λt +Is +еit (4)

λt, representing time effects, is composed of year-specific dummy variables that fluctuate over time but stay constant for all firms within each time period. Is stands for the industry classification of the firm, and eit refers to the error term. In the methodology section of the study, the methodology developed by Martínez-Sola et al. (2024) for companies in Spain has been adopted as is. This choice is made on the grounds of the fact that Spain and Türkiye have similar accounting regulations based on international standards. Even though their economic structures differ, with Spain relying more on the service sector and Türkiye on the industry and exports, nevertheless, both countries are facing the same challenges, like high debt and financial instability.

Before conducting descriptive statistics and hypothesis tests, it is crucial to test the stationarity of the panel dataset. Panel unit root tests are essential for determining the trend or stationarity properties in time series data. These tests ensure the validity of independence and stability assumptions, thereby improving the reliability of model predictions. There is no cross-sectional dependence in the research model (see Friedman Test in Table 7), and first-generation tests have been used. The Levin, Lin Chu (LLC) and Harris-Tzavalis (HT) unit root tests, suitable for N (cross-sectional) and T (time) dimensions, were used. The results are provided in Table 2.

|

Unit-Root Tests |

Statistics/ |

LEVE |

STLEVE |

BC |

SIZE |

AGE |

ROA |

SG |

|

LLC |

Statistics |

-39.1477 |

-39.5461 |

-3.3e+02 |

-33.5977 |

-62.2401 |

-19.2022 |

-29.7488 |

|

p-Value |

0.0000 |

0.0000 |

0.0000 |

0.0000 |

0.0000 |

0.0000 |

0.0000 |

|

|

HT |

Statistics |

-0.1968 |

-0.2534 |

0.0503 |

0.2094 |

0.0874 |

0.1845 |

-0.0911 |

|

p-Value |

0.0000 |

0.0000 |

0.0000 |

0.0000 |

0.0000 |

0.0000 |

0.0000 |

When the results of the panel unit root test have been examined, it can be stated that the series forming the panel data set are stationary, and the analysis results to be obtained will be reliable.

|

Variables |

Disclosure Firms |

Non-Disclosure Firms |

Difference of Means |

t-statistics/ z-statistics |

|

LEVE |

3.0434 |

2.2640 |

-0.7794 |

-0.65 |

|

STLEVE |

2.0048 |

1.9551 |

-0.0498 |

-0.06 |

|

BC |

0.4832 |

0.5048 |

0.0215 |

0.11 |

|

FD |

0.3658 |

0.2825 |

-0.0833*** |

-1.37 |

|

SIZE |

8.4768 |

8.4353 |

-0.0415** |

-1.10 |

|

AGE |

1.4763 |

1.4813 |

0.0051 |

0.37 |

|

ROA |

0.0458 |

0.0797 |

0.0339* |

5.05 |

|

SG |

41.8953 |

45.5178 |

3.6225 |

0.41 |

|

Obs. |

451 |

669 |

When Table 3 is examined, it is found that the disclosure firms are facing more serious financial distress compared to those experienced by non-disclosure firms, which means that their operating income is insufficient to cover their interest expenses. It has also been determined that the profitability of non-disclosure firms is higher compared to disclosure firms. In addition, we observe that disclosure firms have a larger total assets size. On the other hand, it has been observed that disclosure firms are financially more constrained, which means they have higher leverage ratios (especially total leverage) and lower growth rates compared to non-disclosure firms. The most interesting feature of the descriptive statistics is that, contrary to expectations, disclosure firms have a lower cost of debt compared to those of non-disclosure firms, although the difference is very small. No statistically significant difference was found for this variable, and most variables showed no significant differences. This may be due to the small sample size, which reduces the statistical power of mean difference tests.

A sectoral analysis was conducted to provide more detailed insights. The results of the sector-based analysis are presented in Table 4.

|

Sector |

Total Firms |

5+ Disc. |

5- Disc. |

Total Observations |

Accounting Disclosures |

Disclosures By Sector |

|

Manufacturing |

60 |

22 |

38 |

600 |

247 |

41.67% |

|

Financial Institutions |

19 |

9 |

10 |

190 |

92 |

48.42% |

|

Hotels and Restaurants |

7 |

2 |

5 |

70 |

22 |

31.43% |

|

Technology |

5 |

1 |

4 |

50 |

7 |

14.00% |

|

Wholesale and Retail Trade |

4 |

1 |

3 |

40 |

10 |

25.00% |

|

Electricity, Gas, and Water |

4 |

3 |

1 |

40 |

21 |

52.50% |

|

Construction and Public Works |

4 |

2 |

2 |

40 |

16 |

40.00% |

|

Information and Communication |

3 |

0 |

3 |

30 |

8 |

26.67% |

|

Others |

6 |

4 |

2 |

60 |

28 |

46.67% |

When examining Table 4, it can be observed that the sectors with the highest reporting frequency of events after the reporting period during the years covered by the study can be listed in the following order: (1) Electricity, Gas, and Water, (2) Financial Institutions, and (3) Others. However, it should be noted that these results may be misleading due to the limited number of the observation values. When these sectors are disregarded, and, considering the large number of observations, it is notable that the sector with the highest reporting habit of events after the balance sheet date is the manufacturing sector. Additionally, it is observed that the number of firms included in the analysis by sector and the number of events reported by these firms after the balance sheet date in the years covered by the study are categorized into two groups: those reporting events for more than 5 years and those reporting events for less than 5 years.

Before proceeding with the analysis of the logit regression Equations 1–4, the correlation between the independent variables was tested. The results of analysis are presented in Table 5.

|

LEVE |

STLEVE |

BC |

FD |

SIZE |

AGE |

ROA |

SG |

|

|

LEVE |

1.0000 |

|||||||

|

STLEVE |

0.9679 |

1.0000 |

||||||

|

BC |

0.0003 |

0.0053 |

1.0000 |

|||||

|

FD |

0.0263 |

0.0127 |

0.0484 |

1.0000 |

||||

|

SIZE |

0.0359 |

0.0510 |

-0.0275 |

-0.0155 |

1.0000 |

|||

|

AGE |

0.0090 |

-0.0100 |

-0.0839 |

0.0553 |

0.3084 |

1.0000 |

||

|

ROA |

-0.0577 |

-0.0675 |

-0.1870 |

-0.5534 |

0.0398 |

0.0814 |

1.0000 |

|

|

SG |

-0.0152 |

-0.0167 |

-0.0046 |

-0.0199 |

0.0666 |

-0.0390 |

0.1264 |

1.0000 |

It can be observed that there are no large and statistically significant relationships indicating multicollinearity problems in Table 5. Only a high and positive correlation between the total leverage and the short-term leverage has been observed; however, since both variables are not included in the model simultaneously, this will not pose a problem.

In this part of the study, panel regression Equations 1 to 4 will be utilized to analyze the effect of financial constraints and distress on the disclosure of subsequent events following the reporting period. Before proceeding with the estimation of the models, it is essential to identify the appropriate estimators in panel data analysis based on the structure of the data. In the study, various tests were conducted to determine the most appropriate estimator among the classical pooled Ordinary Least Squares (OLS), Fixed Effects, and Random Effects models. Initially, the F (Chow) test was carried out, followed by the Breusch-Pagan (1980) test. Based on the outcomes of these tests, the Hausman test was then performed. The selected estimation method is presented in Table 6 (Bellikli and Dastan, 2021; Bellikli, 2024).

|

Models |

1 |

2 |

3 |

4 |

|

Firm Effect |

59.88 (0.00) Yes |

60.37 (0.00) Yes |

58.26 (0.00) Yes |

59.18 (0.00) Yes |

|

Time Effect |

0.11 (0.37) No |

0.11 (0.37) No |

0.12 (0.36) No |

0.13 (0.35) No |

|

Hausman |

2.15 (0.83) |

4.46 (0.49) |

4.16 (0.53) |

2.29 (0.81) |

It has been determined that the random effects model is valid for all models in the study based on the test results, and that a firm effect has been included in the models.

After selecting the estimators, diagnostic tests were performed to check for issues like heteroscedasticity, autocorrelation, and cross-sectional dependence. The Levene-Brown Forsythe (LBF) test detected heteroscedasticity, while the Durbin-Watson (DW) test and the Baltagi-Wu LBI test were used for autocorrelation. The Friedman test assessed cross-sectional dependence. The results are shown in Table 7.

|

Models |

1 |

2 |

3 |

4 |

|

|

Heteroscedasticity (LBF Test) |

W0** W50** W10** |

6.9367 1.3085 5.1068 |

6.9367 1.3074 5.1075 |

6.9167 1.3240 5.1040 |

7.0770 1.3273 5.1916 |

|

Autocorrelation |

Bhargava DW* Baltagi-Wu LBI* |

1.8450 2.0732 |

1.8439 2.0720 |

1.8452 2.0722 |

1.8447 2.0718 |

|

Cross-Sectional Dependence |

Friedman |

16.8450 (1.0000) |

16.1550 (1.0000) |

15.3500 (1.0000) |

18.8640 (1.0000) |

Based on the test results, it was determined that only the issue of heteroscedasticity exists in all models. In the panel data analysis, the reliability of the results depends on the fulfillment of basic econometric assumptions. In the panel data analysis, addressing econometric issues identified through assumption testing requires the application of robust estimators. Thus, the heteroscedasticity issue in all models was resolved by using the Huber, Eicker, and White (HEW) robust estimator, and robust standard errors were obtained. The research equations for Models 1 to 4 were solved by using the Huber, Eicker, and White (HEW) robust estimator, and the results are presented in Table 8.

Models 1 to 3 analyze the impact of financial constraints, including the total leverage, the short-term leverage, and the borrowing cost, on post-reporting period disclosures. The effect of the total leverage and the short-term leverage on events after the reporting period is positive and statistically significant. These results are consistent with studies in the literature which show that those firms which frequently report events after the reporting period tend to have higher leverage levels compared to those firms which do not report such events (Burns and Kedia, 2006; Zhang et al., 2018). The findings suggest that companies with high total leverage and short-term leverage ratios may intentionally manipulate their financial information in order to present a more favorable financial position and secure external financing. Additionally, it can be stated that the findings are related to the result that firms with a greater need for external financing may resort to incorrect reporting in order to present a better financial condition (Efendi et al., 2007). The legal actions that lenders may take, such as an early termination of loan agreements and increases in the interest rates, can impact the reporting of the subsequent events. These factors may influence the decision to disclose events occurring after the reporting period.

|

Models/ Variables |

1 DISC1 |

2 DISC2 |

3 DISC3 |

4 DISC4 |

|

LEVE |

0.0094** (0.0062) |

|||

|

STLEVE |

0.0110** (0.0070) |

|||

|

BC |

-0.0033 (0.0023) |

|||

|

FD |

0.0115*** (0.0402) |

|||

|

SIZE |

0.0410 (0.0339) |

0.0404 (0.0340) |

0.0432 (0.0339) |

0.0428 (0.0342) |

|

AGE |

-0.0682 (0.1100) |

-0.0660 (0.1099) |

-0.0694 (0.1097) |

-0.0667 (0.1090) |

|

ROA |

-0.6252* (0.1374) |

-0.6271* (0.1374) |

-0.6698* (0.1437) |

-0.6153* (0.1617) |

|

SG |

0.0001 (0.0002) |

0.0001 (0.0002) |

0.0001 (0.0002) |

0.0001 (0.0002) |

|

Constant |

0.1872 (0.2651) |

0.1912 (0.2659) |

0.1885 (0.2668) |

0.1795 (0.2691) |

|

R2 |

0.0664 |

0.0572 |

0.0766 |

0.0716 |

|

Observation |

1.120 |

1.120 |

1.120 |

1.120 |

Another result in Table 8 which merits specific discussion is the negative relationship between the debt cost and the reporting of subsequent events. However, this relationship is not statistically significant. Firms with high debt costs may report subsequent events more frequently in order to secure cheaper external financing, which can lead to aggressive accounting practices. However, the results obtained show that, for the Turkish firms included in the study, the cost of debt does not have a significant effect on the disclosure of subsequent events. These results do not align with the existing literature (Richardson et al., 2002). Perhaps the reason for this could be the need to consider the borrowing costs in conjunction with the different conditions in Türkiye, such as inflation, exchange rates, and interest rate spirals.

The findings have confirmed Hypothesis 1a and Hypothesis 1b. However, Hypothesis 1c could not be confirmed. Moreover, our findings are consistent with the previous literature, which suggests that firms facing financial constraints tend to engage in earnings management practices, which, in turn, may increase the disclosure of events after the reporting period (Farrell et al., 2014; Kurt, 2018; Bowen et al., 2018; He and Ren, 2023; Martínez-Sola et al., 2024). Financial market pressures stemming from such constraints may drive firms to present a healthier financial picture, which can, in turn, influence their disclosure of events after the reporting period (Bermpei et al., 2022).

Finally, it has been empirically proven that financial distress has a significant and statistically meaningful effect on the disclosure of events after the reporting period. Financially distressed firms may adopt aggressive accounting practices in order to avoid situations like bankruptcy, which could increase the frequency of disclosure of events after the reporting period. The results of this study are consistent with the previous research findings which confirm that firms experiencing financial distress are more likely to report events occurring after the reporting period (Burns and Kedia, 2006; Rezaee et al., 2021; Martínez-Sola et al., 2024). These empirical findings validate Hypothesis 2, and the results are supported by empirical findings suggesting that companies facing financial distress, particularly those facing a risk of bankruptcy, are more likely to engage in earnings manipulation so that to avoid or delay insolvency (García Lara et al., 2009; Jones, 2011; Beneish et al., 2012; Campa and Camacho-Minano, 2015; Reinhart, 2022).

The only statistically significant and negative result concerning the control variables in relation to the reporting of events after the reporting period is profitability. No statistically significant results have been obtained for any of the other control variables. The findings suggest that firms with higher profitability are less likely to report events after the reporting period, and these results are consistent with some studies presented in the existing literature (Scholz, 2014).

The disclosure of events after the reporting period entails the adjustment of financial statements, and it has become a frequently researched area in the accounting literature. A review of the literature reveals that studies focusing on specific country cases often examine how events disclosed after the reporting period impact the stock market performance of companies. This study focuses on Türkiye as a case study and examines the impact of financial constraints and distress on events after the reporting period disclosures by using data from firms operating across various sectors. This approach aims to contribute to the limited literature by adopting a reverse perspective, in contrast to most studies that examine the impact of events after the reporting period on a firm’s financial position.

The study has found that firms with high levels of debt, particularly short-term debt, and those experiencing financial distress are more likely to disclose the subsequent events. Firms experiencing financial constraints and distress may, under the pressure of the market forces, resort to aggressive accounting practices. This drives them to manage their accounts and make more disclosures of the subsequent events. It is possible to draw some general inferences from this study. Financial constraints may lead companies to the use of more discretionary accruals during capital increases and external financing activities. In addition, the increase in the company’s publicly traded stock prices reduces the cost of capital and facilitates equity financing. A high level of accruals can improve the appearance of earnings, which may reduce potential concerns of the company’s creditors. In other words, all these factors are likely to contribute to the success of future financing, as they may help build investor confidence in the company’s management.

The results obtained in this study are consistent with the previous literature which has empirically demonstrated the use of events after the reporting period for earnings management (Li et al., 2024). This may lead to a decrease in the reliability of their financial statements.

Even unintentional errors in post-reporting disclosures can raise concerns about a firm’s reliability. Creditors may view the company as a riskier undertaking, which would lead to higher interest rates or even outright loan refusals. This study offers practical insights for banks, institutional investors, and individual investors in Türkiye, thereby helping them assess the lending risks, set loan rates, and helping them make informed investment decisions based on a firm’s disclosure frequency.

Another implication of the findings from this study is of relevance for company management. Companies may be inclined to revise their financial statements in order to borrow at a lower cost. However, this will gradually lead companies into a vicious cycle, as empirical results from the previous literature also show that events after the reporting period tend to increase the borrowing costs (Graham et al., 2008; Park and Wu, 2009). However, according to the research results in this study, it has been found that the borrowing costs have no significant impact on events after the reporting period for Turkish companies within the sample. The previous literature and the findings of this study have proven that companies reporting events after the reporting period are more likely to face greater financial constraints. In short, while everything may seem positive in the short term for a company using events after the reporting period, especially regarding the aspect of its earnings management practices, in the long run, this situation will only worsen the company’s already poor financial condition. To restore the company’s reputation through post-reporting period disclosures, actions such as changing the management, focusing on corporate governance, adhering to accounting conservatism, and strengthening the internal controls are recommended, as suggested by the previous literature (Wu et al., 2016).

It is also important to address the limitations of the study in detail. Firstly, the study focuses on a specific time period. Additionally, the research is limited to a relatively small sample of Turkish companies, which may not fully represent the broader corporate landscape in Türkiye. As a result, the findings and interpretations should be evaluated within this narrow scope, and therefore any generalizations should be made with caution. Despite these limitations, the study provides valuable insights and offers a significant contribution to understanding the financial behaviors of Turkish companies.

Future research could explore larger sample sizes, cross-country comparisons, and other financial constraints affecting post-reporting disclosures. Alternatively, it could examine the topic from perspectives such as auditing, audit quality, or the audit process.

Ahmadi, S., Soroushyar, A., & Naseri, H. (2013). A study on the effect of earnings management on restatement and the changes on information content of earnings following restatements: Evidence from Tehran Stock Exchange. Management Science Letters, 3(12), 2867–2876. https://doi.org/10.5267/j.msl.2013.11.011

Alyousef, H. Y., & Almutairi, A. R. (2010). An Empirical Investigation of Accounting Restatements by Public Companies: Evidence from Kuwait. International Review of Business Research Papers, 6(1), 513–535.

Atasel, O.Y., Güneysu, Y. & Ünal, H. (2020) Impact of Environmental Information Disclosure on Cost of Equity and Financial Performance in an Emerging Market: Evidence from Turkey, Ekonomika, 99(2), 76–91. 10.15388/Ekon.2020.2.5

Badertscher, B. A., & Burks, J. J. (2011). Accounting Restatements and the Timeliness of Disclosures. Accounting Horizons, 25(4), 609–629. https://doi.org/10.2308/acch-50026

Bardos, K. S., & Mishra, D. (2014). Financial restatements, litigation and implied cost of equity. Applied Financial Economics, 24(1), 51–71. https://doi.org/10.1080/09603107.2013.864033

Bellikli, U. (2024). The Effect of Accounting Conservatism On Corporate Social Responsibility: Evidence from the Corporate Governance Index in Türkiye. Ege Academic Review, 24(1), 85-100. https://doi.org/10.21121/eab.1328302

Bellikli, U., & Daştan, A. (2021). Accounting Conservatism and Intellectual Capital: Evidence from Turkey with Comparison Models and Sectors. Ege Academic Review, 21(4), 333-355. https://doi.org/10.21121/eab.1017873

Beneish, M. D., Press, E., & Vargus, M. E. (2012). Insider trading and earnings management in distressed firms. Contemporary Accounting Research, 29(1), 191–220. https://doi.org/10.1111/j.1911-3846.2011.01084.x

Bermpei, T., Kalyvas, A. N., Neri, L., & Russo, A. (2022). Does economic policy uncertainty matter for financial reporting quality. Review of Quantitative Finance and Accounting, 58(4), 795–845. https://doi.org/10.1007/s11156-021-01010-2

Bloom, N. (2014). Fluctuations in Uncertainty, Journal of Economic Perspectives, 28(2), 153–176. https://doi.org/10.1257/jep.28.2.153

Bowen, R., Dutta, S., & Zhum, P. (2018). Are financially constrained firms more prone to f inancial restatements? Working paper. https://doi.org/10.21608/sjar.2023.297436. Available at SSRN 3211497.

Burks, J. (2010). Disciplinary measures in response to restatements after Sarbanes-Oxley. Journal of Accounting and Public Policy, 29(3), 195–225. https://doi.org/10.1016/j.jaccpubpol.2010.03.002

Burns, N., & Kedia, S. (2006). The impact of performance-based compensation on misreporting. Journal of Financial Economics, 79(1), 35–67. https://doi.org/10.1016/j.jfineco.2004.12.003

Butkevičius, R. (2020). Universal Model of Lost Profits Calculation, Ekonomika, 98(2), 97–111. https://doi.org/10.15388/Ekon.2019.2.7

Campa, D., & Camacho-Mi˜nano, M. M. (2014). Earnings management among bankrupt non-listed companies: evidence from Spain. Spanish Journal of Finance and Accounting, 43(1), 3–20. https://doi.org/10.1080/02102412.2014.890820

Campa, D., & Camacho-Mi˜nano, M. M. (2015). The impact of SME’s pre-bankruptcy financial distress on earnings management tools. International Review of Financial Analysis, 42, 222–234. https://doi.org/10.1016/j.irfa.2015.07.004

Çekin, S. E. (2019). Türkiye’de Finans Sisteminin Yapısı ve Dönüşüm Gerekleri. Ankara Seta Publishing.

Chen, X., Cheng, Q., & Lo, A. K. (2014). Is the Decline in the Information Content of Earnings Following Restatements Short-Lived? The Accounting Review, 89(1), 177–207. https://doi.org/10.2308/accr-50594

Conceptual Framework for Financial Reporting-CFFR (2018). TFRS, Conceptual Framework.

Cui, X., Ma, T., Xie, X. & Goodell, J.W. (2023). Uncertainty of uncertainty and accounting conservatism, 52, 103525. https://doi.org/10.1016/j.frl.2022.103525

Cui, X., Wang, C., Liao, J., Fang, Z. & Cheng, F. (2021). Economic policy uncertainty exposure and corporate innovation investment: evidence from China, Pacific-Basin Finance Journal, 67, 101533. https://doi.org/10.1016/j.pacfin.2021.101533

Drechsler, I. (2013). Uncertainty, time-varying fear, and asset prices, The Journal of Finance, 68(5), 1843–1889. http://www.jstor.org/stable/42002598

Efendi, J., Srivastava, A., & Swanson, E. (2007). Why Do Corporate Managers Misstate Financial Statements? The Role of Option Compensation and Other Factors. Journal of Financial Economics, 85(3), 667–708. https://doi.org/10.1016/j. jfineco.2006.05.009

Farrell, K., Unlu, E., & Yu, J. (2014). Stock repurchases as an earnings management mechanism: the impact of financing constraints. Journal of Corporate Finance, 25(2), 1–15. https://doi.org/10.1016/j.jcorpfin.2013.10.004

García Lara, J. M., García Osma, B., & Neophytou, E (2009). Earnings quality in ex-post failed firms. Accounting and Business Research, 39(2), 119–138. https://doi.org/10.1080/00014788.2009.9663353

Goodell, J.W., Goyal, A. & Urquhart, A., (2021). Uncertainty of uncertainty and firm cash holdings, Journal of Financial Stability, 56, 100922. https://doi.org/10.1016/j.jfs.2021.100922

Graham, J. R., Li, S., & Qiu, J. (2008). Corporate Misreporting and Bank Loan Contracting. Journal of Financial Economics, 89(1), 44–61. https://doi.org/10.1016/j.jfineco.2007.08.005

He, G., & Ren, H. M. (2023). Are financially constrained firms susceptible to a stock price crash? The European Journal of Finance, 29(6), 612–637. https://doi.org/10.1080/1351847X.2022.2075280

Hennes, K., Leone, A., & Miller, B. (2008). The importance of distinguishing errors from irregularities in restatement research: The case of restatements and CEO/CFO turnover. The Accounting Review, 83(6), 1487–1519. https://doi.org/10.2308/accr.2008.83.6.1487

Hribar, P., & Jenkins, N. (2004). The effect of accounting restatements on earnings revisions and the estimated cost of capital. Review of Accounting Studies, 9(2-3), 337–356. https://doi.org/10.2139/ssrn.488003

Hu, S., Qian, Y. & Hu, S. (2024). Do customers’ financial restatements affect how auditors respond to their suppliers? Evidence from China, Managerial Auditing Journal, 39(3), 294-319. https://doi.org/10.1108/MAJ-04-2023-3906

Im, H.Y., Park, H., Pathan, S., & Faff, R. (2024). Transient institutional ownership, costly external finance and corporate cash holdings. Journal of Business Finance and Accounting, 10(24), 1–38. https://doi.org/ 10.1111/jbfa.12840

International Accounting Standards (2007). IAS-10 Events After the Reporting Period.

Jin, J.Y., Kanagaretnam, K., & Li, N. (2023). The Impact of FASB Staff Position APB 14-1 on Corporate Financing: A Debt Contracting Perspective. Journal of Risk and Financial Management,16(213), 1-23. https://doi.org/10.3390/jrfm16040213

Jones, S. (2011). Does the capitalization of intangible assets increase the predictability of corporate failure? Accounting Horizons, 25(1), 41–70. https://doi.org/10.2308/acch.2011.25.1.41

Kurt, A. C. (2018). How do financial constraints relate to financial reporting quality? Evidence from seasoned equity offerings. European Accounting Review, 27(3), 527–557. https://doi.org/10.1080/09638180.2017.1279556

Li, Z., Liu, X. & Wang, B. (2024). Military-experienced senior executives, corporate earnings quality and firm value, Journal of Accounting Literature, 46(3), 401-445. https://doi.org/10.1108/JAL-08-2022-0089

Martínez-Sola, C., Sanabria-García, S., & Garrido-Miralles, P. (2024). The effect of financial constraints on accounting restatements: Spanish evidence. European Research on Management and Business Economics, 30(2), 100244, https://doi.org/10.1016/j.iedeen.2024.100244

Mehanna, S.F., & Soliman, M.M. (2023). Are Financially Constrained Firms More Susceptible to Restatements’ Incidence. Egypts Presidential Specialized Council for Education and Scientific Research, 1(23), 23–32. https://doi.org/ 10.21608/sjar.2023.297436

Neamtiu, M., Shroff, N., White, H.D. & Williams, C.D. (2014). The impact of ambiguity on managerial investment and cash holdings, Journal of Business Finance & Accounting, 41(7–8), 1071–1099. http://hdl.handle.net/1721.1/111108

Olusola, L., & Abdulasisi, M. (2020). Firm characteristics and restatement of financial statements in Nigeria. International Journal of Research and Innovation in Social Science, 4(8), 623–628.

Park, J. C., & Wu, Q. (2009). Financial Restatements, Cost of Debt and Information Spillover: Evidence from the Secondary Loan Market. Journal of Business Finance & Accounting, 36(9-10), 1117–1147. https://doi.org/10.1111/j.1468- 5957.2009.02162.x

Reinhart, C.M. (2022). From Health Crisis to Financial Distress. IMF Econ Rev 70, 4–31 https://doi.org/10.1057/s41308-021-00152-6

Rezaee, Z., Asiaei, K., & Safdel Delooied, T. (2021). Are CEO experience and financial expertise associated with financial restatements? Spanish Accounting Review, 24(2), 270–281. https://doi.org/10.6018/rcsar.379991

Richardson, S., Tuna, I., & We, M. (2002). Predicting earnings management: The case of earnings restatements. Social Science Research Network Working Paper Series.

Scholz, S. (2014). Financial restatement trends in the United States: 2003–2012. Center for audit quality, 23, 1–42.

Wu, P., Gao, L., Chen, Z., & Li, X. (2016). Managing reputation loss in China: in-depth analyses of financial restatements. Chinese Management Studies, 10(2), 312–345. https://doi.org/10.1108/CMS-12-2015-0275

Zhang, H., Huang, H. G., & Habib, A. (2018). The effect of tournament incentives on financial restatements: Evidence from China. The International Journal of Accounting, 53(2), 118–135. https://doi.org/10.1016/j.intacc.2018.05.002