Ekonomika ISSN 1392-1258 eISSN 2424-6166

2025, vol. 104(3), pp. 62–83 DOI: https://doi.org/10.15388/Ekon.2025.104.3.4

Central Bank Independence and Inflation in the MENA Region: Does Institutional Quality Matter?

Abdellatif Mouatassim

Department of economics and business administration, Mohammed V University, Rabat, Morocco

ORCID: https://orcid.org/0000-0003-0847-4174

Ahmed Kchikeche*

Department of economics and business administration, Chouaib Doukkali University, El Jadida, Morocco

Route Nationale N° 1 El haouziya, BP n°356, El Jadida, Morroco

ORCID: https://orcid.org/0000-0003-1928-3381

Email: kchikeche.ahmed@ucd.ac.ma

Phone: 00212619194100

Abdellah Echaoui

Department of economics and business administration, Mohammed V University, Rabat, Morocco.

ORCID: https://orcid.org/0000-0002-4822-3372

Abderrazak El Hiri

Department of economics and business administration, Sidi Mohammed Ben Abdellah University, Fes, Morocco.

Abstract. This paper examines the impact of Central Bank independence on Inflation in 16 MENA countries from 1990 to 2017. By employing a two-stage least squares instrumental variables approach, the study assesses the influence of three legal independence measures on the inflation rate. It investigates the moderating role of institutional quality in the relationship between these two variables. The findings robustly demonstrate that an increased Central Bank independence leads to lower inflation rates across all measures, model specifications, and estimation methods. Moreover, institutional quality not only directly reduces inflation but also enhances the negative impact of the Central Bank independence on inflation. Consequently, the study suggests that policymakers in MENA countries should reinforce the independence of monetary authorities and improve the overall institutional quality to maintain price stability.

Keywords: Central Bank independence; inflation; institutional quality; MENA; two-stage-least-squares.

____________

* Correspondent author.

Received: 23/12/2024. Revised: 26/05/2025. Accepted: 26/05/2025

Copyright © 2025 Abdellatif Mouatassim, Ahmed Kchikeche, Abdellah Echaoui, Abderrazak El Hiri. Published by Vilnius University Press. This is an Open Access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

1. Introduction

The importance of the Central Bank independence (henceforth referred to as CBI) in ensuring the consistency and credibility of a monetary policy is well-documented in the literature (Aklin & Kern, 2021; Dall’Orto Mas et al., 2020). Central bank autonomy is widely regarded as a net positive for economic growth and price stability, prompting extensive reforms of central banking across the globe (Agur, 2021; Armah, 2024; Rabhi & Parsons, 2024). While some of these reforms have been aimed at mitigating inflationary pressures (Krušković, 2022), others have been driven by objectives such as regional convergence, monetary union, or meeting the International Monetary Fund requirements (Romelli, 2022).

Theoretically, CBI is considered a critical pillar for addressing the time inconsistency problem inherent in discretionary policymaking, which tends to generate inflationary biases (Kydland & Prescott, 1977). Governments often face a trade-off between inflation and unemployment, leading to policies that may favor short-term gains but result in long-term inflation (Barro & Gordon, 1983). Delegating monetary policy to an independent central bank, as proposed by Rogoff (1985), minimizes this bias by prioritizing price stability over political considerations (Binder, 2021; Wachtel & Blejer, 2020).

In the Middle East and North Africa (MENA) region, where institutional frameworks tend to be weaker, significant central bank reforms were undertaken since the 1990s (Romelli, 2024). These reforms often included revisions to the legal foundations of the monetary policy, aiming to enhance de jure independence (Cukierman et al., 1992; Romelli, 2022). While these legal changes contributed to improved monetary governance (Garriga & Rodriguez, 2023), questions remain about whether de jure independence translates into de facto autonomy, particularly in countries with fragile institutions (Filiz et al., 2022).

Control over inflation has become an increasing priority for MENA central banks. An analysis of central bank statutes, by using Romelli’s (2022) data, reveals a growing trend from the early 2000s toward adopting price stability as the primary objective of a monetary policy. In particular, the MENA region’s monetary policy landscape is marked by significant heterogeneity. It remains divided between a discretionary approach – granting substantial autonomy to monetary authorities without predefined rules, as observed in Yemen, Tunisia, Egypt, Libya, Algeria, and Iran – and an exchange rate-centered framework, which varies in rigidity across countries such as Morocco, Saudi Arabia, Qatar, Kuwait, and Jordan. Notably, a growing consensus has emerged regarding the central role of price stability in achieving broader macroeconomic objectives. Over time, most MENA countries have gradually adopted price stability as the primary objective of their monetary policy. However, the approaches to achieving this goal remain diverse across the region.

For instance, in 1990, only five countries – Bahrain, Jordan, Kuwait, Saudi Arabia, and Yemen – explicitly included price stability among their objectives, often alongside conflicting goals. By 2000, Qatar, Libya, and Oman had joined this group, while Egypt and Tunisia pursued price stability within frameworks of non-conflicting goals. Yemen stood out as the only country to adopt price stability as its sole objective. By 2017, Morocco and Yemen were the only countries where price stability had become the exclusive priority, while 12 out of the 16 countries studied continued to balance it with other, often conflicting, objectives.

Despite these reforms, inflation remains a persistent challenge in the MENA region (Gatti et al., 2023). Strengthening CBI is, therefore, critical to maintaining price stability and fostering long-term economic resilience. Yet, empirical studies on the relationship between CBI and inflation in the region remain limited, particularly those that consider the moderating role of institutional quality. This omission is significant, given the potential for institutional factors to either enhance or undermine the effectiveness of central bank autonomy.

The objective of this paper is twofold. First, it investigates the impact of the central bank independence on inflation in the MENA region. Second, it examines whether the institutional quality plays a role in the ability of monetary policy conducted by an independent central bank to reduce inflation. Based on the reviewed literature, this study seeks to test the hypothesis that the central bank independence enhances the effectiveness of the monetary policy in controlling inflation. Furthermore, it posits that higher levels of institutional quality amplify the capacity of central banks in the MENA region to maintain price stability.

To do so, this paper examines the impact of the central bank independence on inflation across the 16 MENA countries from 1990 to 2017, with a particular focus on the moderating role of institutional quality. We employ three dynamic panel estimators to ensure the robustness of our results and utilize three distinct measures of CBI to capture different dimensions of the central bank autonomy.

The remainder of this paper is structured as follows: Section 2 provides a review of the relevant literature, highlighting theoretical and empirical insights. Section 3 outlines the data and methodology used in our analysis. Section 4 presents and discusses the empirical results, while Section 5 concludes by summarizing the key findings and discussing their policy implications.

2. Literature Review

2.1. Measuring central bank independence: An overview

Measuring the central bank independence in developing countries is a challenge. Literature distinguishes between two types of measures. De jure (i.e., legal) type measures quantify independence in the analysis of legal documents and regulatory frameworks, while de facto (i.e., effective) type measures political pressures on the central bank authorities through indicators such as the turnover rate of the governor (Afrouzi et al., 2024; Binder, 2020; Strong, 2021).

De jure measures of the central bank independence go back to the pioneering work of Bade and Parkin (1982) emphasizing political pressures on the central bank independence. Later, Grilli, Masciandaro, and Tabellini (1991) constructed an alternative measure (henceforth called the GMT index) which reflects both political and economic independence. Similarly, Cukierman, Webb, and Neyapti (1992) constructed three indices (henceforth referred to as the LVAU index) based on the legal framework representing the degree of independence that the legislator would like to confer to the central bank. As for de facto measures, they are usually operationalized through either the turnover rate of the central bank governor or expert surveys measuring the extent to which the autonomy conferred by the legislation is practiced (Cukierman, 1992). More recently, Romelli (2022) constructed a new dynamic central bank independence index addressing criticisms of the LVAU and GMT measures of the central bank independence. This new index (henceforth called BCIE) incorporates the previous two measures while adding components related to financial independence, reporting, and accountability.

2.2. Central bank independence and inflation: The role of institutional quality

Since its genesis in the 1980s (Takahashi, 2021), more than 9000 studies have been devoted to the economic outcomes of the central bank independence (Vuletin & Zhu, 2011). Although much of the literature on the subject argues for the benefits of the central bank independence through arguments ranging from resolving the time inconsistency of discretionary policies to mitigating the use of the monetary policy by public authorities for electoral purposes (Kydland & Prescott, 1977), not all empirical work is aligned with these arguments. While studies on developed countries have shown that a greater central bank autonomy is associated with a lower average inflation (Visokavičienė, 2014), Hillman (1999) argues that, for transition economies, a higher degree of the central bank independence is associated with a higher inflation. In contrast, Campillo & Miron (1997), Cargill (1995), Klomp & De Haan (2010a), and Lim (2021) found no evidence of a relationship between the central bank independence and inflation. Also, while Arnone & Romelli (2013) highlight the importance of a proper measure of the central bank independence, Klomp & De Haan (2010b) argue, through a meta-regression analysis of 59 studies, that this inclusiveness is not caused by the difference in the measures of the central bank independence.

For developing countries, early studies did not show a relationship between de jure measures of CBI and inflation. However, de facto measures show that a negative relationship between inflation and independence also emerges (Cukierman, 1992; Cukierman et al., 1992; Cukierman & Webb, 1995; Hillman, 1999). More recent studies on developing countries (Anwar, 2023; Anwar & Nicholas, 2020; Garriga & Rodriguez, 2020; Gyeke-Dako et al., 2022; Jácome & Pienknagura, 2022; Mackiewicz Łyziak & Kokoszczyński, 2020) found that the central bank had a significant negative impact on inflation. An explanation of these results could be attributed to the low institutional quality of developing countries (Lim, 2021).

The ambiguous results suggest that other factors affect the effectiveness of the central bank independence in reducing inflation: the CBI is more effective in reducing inflation in the presence of high levels of financial development and institutional quality (Agoba et al., 2017, 2020; Arnone & Romelli, 2013; Katseli et al., 2020). Along these lines, Agoba et al. (2017) show that institutional quality moderates the effect of the central bank independence on inflation in African countries. Similarly, Hielscher and Markwardt (2012) report that granting autonomy to a Central Bank does not necessarily lead to a lower inflation, as the effectiveness of the central bank independence requires the union of two conditions: sufficiently high improvements in independence and a robust quality of political institutions.

We contribute to the existing literature by examining the impact of the central bank independence on inflation in a sample of countries often neglected by the literature while considering the effects of the institutional quality on this impact. Furthermore, we control the effect of the central bank independence measurements and estimation methods.

3. Data and Methodology

3.1. Data and specifications

Our specifications can be synthesized as follows:

Infi,t = f (Infi,t–1, CBIi,t, INSTQLi,t, DEMOCi,t, CBi,t × INSTQLi,t, CBIi,t × DEMOCi,t, Xi,t) (1)

where i and t represent the country and the period, respectively. The inflation rate is a function of its one-period lag Infi,t–1, the level of the central bank independence measures through one of three indicators CBIi,t = {GMT; LVAU; CBIE}, two measures of institutional quality {DEMOC; INSTQL}, their respective interaction terms with the central bank independence measures, and a set of country-specific control variables Xi,t.

We measure Infi,t as the year-to-year growth of the consumer price index. Furthermore, to smooth the inflation rate dynamics and reduce the heteroscedasticity of errors, we apply the transformation used by Cukierman et al. (1992) according to the following formula  . This measure is useful when studying developing countries that may have more volatile inflation rates (Arnone & Romelli, 2013; Cukierman et al., 1992; Jácome & Vázquez, 2008; Vuletin & Zhu, 2011). Infi,t–1 is a one-period lagged inflation rate, included to account for the persistence of this variable.

. This measure is useful when studying developing countries that may have more volatile inflation rates (Arnone & Romelli, 2013; Cukierman et al., 1992; Jácome & Vázquez, 2008; Vuletin & Zhu, 2011). Infi,t–1 is a one-period lagged inflation rate, included to account for the persistence of this variable.

We use three central bank independence measures (CBIi,t) sourced from (Romelli, 2022).

1. The GMT index, developed by Grilli et al. (1991), varies between 0 to 1 and reflects both political and economic independence. Political independence is the ability to choose the final objective of the monetary policy (e.g., inflation vs. growth and unemployment). Economic independence lies in the central bank’s ability to choose the instruments with which it can pursue these objectives.

2. The LVAU index, developed by Cukierman, Webb, and Neyapti (1992), is based on the characteristics of the legal framework that represents the degree of independence that the legislator would like to confer to the central bank. These characteristics are grouped into multiple clusters that are in turn constructed of multiple variables.

3. The CBIE index, developed by Romelli (2022), is a comprehensive and objective legal measure of the central bank independence. It addresses criticisms of previous measures like GMT by encompassing a broad range of the central bank characteristics and integrating all aspects of prior indices. Additionally, the CBIE index includes components related to financial independence, reporting, and accountability, effectively capturing all reforms to the central bank statutes.

Also, the models include measures of the rule of law and democracy that are susceptible to impact the inflation-CBI relationship (Agoba et al., 2017; Bodea et al., 2015; Fazio et al., 2018). We employ two indicators of institutional quality. First, INSTQLi,t is a country-specific score representing the rule of law, capturing the extent to which the electoral process is free and fair, the state of political pluralism and participation, and the functioning of the government (Freedom House, 2024). High levels of institutional quality are associated with a low inflation (Agoba et al., 2017). Second, we employ the Polity2 score sources from the Center for Systemic Peace (2021) to represent the authority characteristics of each country. All other things being equal, more democratic countries scored better in this regard (Garriga & Rodriguez, 2020). To measure the role of institutional quality in the impact of the central bank independence on inflation, we include the interaction terms between both variables and each of our central bank independence.

We employ multiple control variables in our study. Two dummy variables represent the key qualitative country-specific instances of our sample. First, the exchange rate regime plays a key role in the ability of central banks to conduct their monetary policy and target inflation. Thus, we include a dummy indicating whether the country has a fixed exchange rate regime based on the de facto classification by Reinhart and Rogoff (2004, 2009) and the types of the exchange rate regime by the IMF (2021). Second, we include a dummy representing whether a country is a net importer or exporter of oil. This characteristic is of high relevance in our sample which includes some of the top oil exporters in the world (Kchikeche & El Mahmah, 2022).

Finally, our study includes some key macroeconomic control variables. First, to account for the transmission of foreign inflationary pressures, we include both world inflation (WINF) measured by the median yearly percentage change in the consumer price index of all World Bank reporting countries, and the trade openness rate (TRDOPN) measured as the ratio of export and import to GDP. Furthermore, to account for the impact of domestic economic activity on inflation, we include the output gap (OTGAP), calculated by using the HP filter as the difference between the actual and potential GDP (as a % of potential GDP).

3.2. Empirical methodology

The decision to implement a Central Bank reform may be self-dependent on inflation levels, as (Anwar & Nicholas (2020) show that there is a bi-directional causality between the central bank independence and inflation in developing countries. Thus, in order to account for endogeneity and further ensure the robustness of our results, we employ two-stage least squares instrumental variables estimators, as suggested by Agoba et al. (2017). Two-stage generalized least squares (G2SLS), developed by Balestra and Varadharajan-Krishnakumar (1987), and two-stage error correction least squares (EC2SLS), described in Baltagi and Chang (2000), were used in this research.

In all cases, the lagged values of the indices of the different CBI measures were used as instruments, respectively. In all cases, the lagged CBI values were used as instruments for the central bank independence. The results of the first stage indicate that the instrument was appropriate, with the associated coefficient being significant in all cases.

4. Results and Discussions

4.1. Descriptive statistics

Table 1 presents some descriptive statistics on the variables in our models. Notably, it shows that, after adjustment, inflation averages out to zero in our sample with some significant outliers. Higher inflation rates were recorded in Libya, especially due to the post-revolution armed conflict that followed the Arab Spring. On the other hand, Iran’s economy is characterized by durable high inflation due to economic sanctions imposed by the USA and its allies. Otherwise, the average inflation in most of the countries in our sample averaged between -0.5% and 5% during the period studied.

As for the central bank measures, the level of the central bank independence in the MENA region is rather average, reaching around 0.5 for both GMT and LVAU indices, and not surpassing 0.88 for values that can go up to 1. Interestingly, the CBIE dynamic index reports a lower independence as it reflects a wider range of indicators of financial independence, reporting, and accountability. This under-reporting of independence may indicate that purely statuary characteristics of central banks in the MENA region do under-represent the effective central bank independence in the region.

Table 1. Descriptive statistics of all variables

|

Variable

|

Observations

|

Mean

|

Std. Dev.

|

Min

|

Max

|

|

Inf

|

444

|

0.003

|

0.041

|

-0.185

|

0.134

|

|

OTPAG

|

439

|

-0.005

|

1.025

|

-5.003

|

5.945

|

|

WINF

|

448

|

0.481

|

0.086

|

0.381

|

0.673

|

|

TRDOPN

|

448

|

0.332

|

0.215

|

0.018

|

1.336

|

|

DEMOC

|

440

|

-4.745

|

4.782

|

-10.00

|

7.00

|

|

INSTQL

|

448

|

5.712

|

0.905

|

2.000

|

7.000

|

|

GMT

|

448

|

0.552

|

0.122

|

0.274

|

0.867

|

|

LVAU

|

448

|

0.532

|

0.103

|

0.296

|

0.819

|

|

CBIE

|

448

|

0.373

|

0.104

|

0.250

|

0.625

|

Source: elaborated by the authors

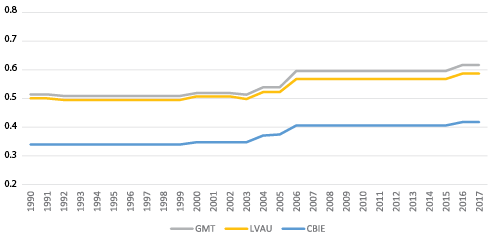

Figure 1 shows that, across all measures, the average central bank independence in the MENA region increased between 1990 and 2017 as the values of the GMT, LVAU, and CBIE indices increased by 20%, 17%, and 23%, respectively.

Figure 1. Evolution of the average level of central bank independence in the MENA region between 1990 and 2017

Source: elaborated by the authors

Figure 2 goes further into the heterogeneity in the central bank independence levels in the MENA region, thus more extensively illustrating the differences between CBIE and both GMT and LVAU indices. Figure 2 also indicates that, while, for most countries, central bank independence indices are around the sample average, Saudi Arabia, Iraq, and Tunisia are considered relatively highly independent, with values exceeding 0.6 for GMT and LVAU indices.

Figure 2. Inter-country variation in Central Bank independence measures

Source: elaborated by the authors

However, considering the CBIE, the index yields different results as the gap between these outliers and the sample average becomes narrower. This index also shows that some countries in the MENA region, such as Egypt, Iran, Kuwait, Qatar, and Yemen, reflect further the discrepancy between de jure and the actual levels of the central bank independence in these countries.

Table 2. Correlation matrix of central bank independence indicators

|

GMT

|

LVAU

|

CBIE

|

|

GMT

|

1

|

|

|

|

LVAU

|

0.7332

|

1

|

|

|

CBIE

|

0.7224

|

0.6561

|

1

|

Source: elaborated by the authors

The differences between the three central bank independence measures are further illustrated when looking at the correlation between them, as shown in Table 2. On the one hand, the correlation coefficients between the coefficients are relatively high, ranging from 0.66 to 0.73, demonstrating that they represent, overall, the same construct. On the other hand, the fact that these coefficients do not surpass 0.9 shows that there are still relevant differences between the three indicators, thereby rendering their utilization as alternative measures of the central bank independence in our estimations more useful.

Figure 3 relates, for each country, the country-average adjusted inflation rates to the average value of the three central bank independence measures. By configuring the X and Y axes to cross at the sample-average values of inflation and central bank independence, the chart yields four quadrants allowing us to divide the sample into four sub-samples. First, countries with higher-than-average levels of inflation and central bank independence are Tunisia, Iraq, Saudi Arabia, and Libya, with the latter two being clear outliers (as Libya has a comparatively high level of inflation, and Saudi Arabia has a comparatively high level of central bank independence). Second, countries with both lower-than-average levels of inflation and central bank independence are Egypt, Bahrain, Yamen, and Iran, with Iran being an outlier with a negative rate of inflation. In the third quadrant, we find countries which have lower-than-average inflation and higher-than-average central bank independence values, notably, Algeria. Finally, most of the countries in the MENA region have both higher-than-average inflation and lower-than-average central bank independence. These countries are Jordan, Lebanon, Morocco, Kuwait, Qatar, and the UAE. Overall, 11 out of the 16 countries in our sample have inflation rate levels between -1% and 1%, and the central bank independence levels between -0.4 and 0.6.

Figure 3. Inflation and central bank independence in the MENA region

Source: elaborated by the authors

Table 3 presents the results of our estimations. The table combines the results of using the three estimations methods and the central bank independence methods. Columns 1, 4, and 7 present the equations with the GMT index, columns 2, 5, and 8 present equations with the LVAU index, and columns 3, 6, and 9 present the equations with the CBIE index.

Table 3. Estimation results

|

G2SLS FE

|

G2SLS RE

|

EC2SLS

|

|

(1)

|

(2)

|

(3)

|

(4)

|

(5)

|

(6)

|

(7)

|

(8)

|

(9)

|

|

GMT

|

-0.565**

(0.274)

|

-

|

-

|

-0.436**

(0.189)

|

-

|

-

|

-0.293***

(0.094)

|

-

|

-

|

|

LVAU

|

-

|

-0.805**

(0.41)

|

-

|

-

|

-0.636**

(0.289)

|

-

|

-

|

-0.409***

(0.133)

|

-

|

|

CBIE

|

-

|

-

|

-0.580**

(0.229)

|

-

|

-

|

-0.367***

(0.131)

|

-

|

-

|

-0.242***

(0.074)

|

|

Inf(-1)

|

0.235**

(0.074)

|

0.230**

(0.075)

|

0.252***

(0.076)

|

0.27***

(0.07)

|

0.261***

(0.069)

|

0.289***

(0.07)

|

0.277***

(0.07)

|

0.271***

(0.07)

|

0.292***

(0.07)

|

|

EXCHREG

|

0.014

(0.012)

|

0.013

(0.012)

|

0.017

(0.015)

|

-0.008*

(0.004)

|

-0.007*

(0.004)

|

-0.002

(0.004)

|

-0.006

(0.004)

|

-0.005

(0.004)

|

-0.002

(0.004)

|

|

EXPORT

|

-

|

-

|

-

|

-0.009***

(0.003)

|

-0.007**

(0.003)

|

-0.01**

(0.004)

|

-0.008***

(0.003)

|

-0.006**

(0.003)

|

-0.009**

(0.004)

|

|

TRDOPN

|

0.053**

(0.022)

|

0.053**

(0.021)

|

0.057**

(0.026)

|

0.038***

(0.013)

|

0.041**

(0.014)

|

0.03**

(0.012)

|

0.034**

(0.014)

|

0.036***

(0.013)

|

0.03**

(0.012)

|

|

WINF

|

0.064**

(0.028)

|

0.064**

(0.028)

|

0.048*

(0.029)

|

0.064**

(0.028)

|

0.064**

(0.028)

|

0.047*

(0.028)

|

0.06**

(0.027)

|

0.059**

(0.027)

|

0.045*

(0.027)

|

|

OTPAG

|

-0.003

(0.002)

|

-0.003

(0.002)

|

-0.003

(0.002)

|

-0.003

(0.002)

|

-0.003

(0.002)

|

-0.002

(0.002)

|

-0.002

(0.002)

|

-0.002

(0.002)

|

-0.002

(0.002)

|

|

DEMOC

|

-0.003

(0.005)

|

-0.004

(0.006)

|

-0.002

(0.003)

|

-0.003

(0.003)

|

-0.004

(0.004)

|

-0.002)

(0.002)

|

-0.002

(0.002)

|

-0.003

(0.003)

|

-0.001

(0.001)

|

|

GMTDEMOC

|

0.005

(0.009)

|

0.006

(0.012)

|

0.006

(0.009)

|

0.006

(0.006)

|

0.008

(0.007)

|

0.004

(0.005)

|

0.004

(0.004)

|

0.005

(0.005)

|

0.003

(0.004)

|

|

INSTQL

|

-0.055*

(0.030)

|

-0.076*

(0.042)

|

-0.036**

(0.017)

|

-0.039**

(0.019)

|

-0.056**

(0.028)

|

-0.023**

(0.01)

|

-0.024***

(0.009)

|

-0.034***

(0.013)

|

-0.014**

(0.006)

|

|

INDEP*INSTQL

|

0.097*

(0.053)

|

0.138*

(0.077)

|

0.096**

(0.042)

|

0.076**

(0.037)

|

0.11**

(0.054)

|

0.065**

(0.026)

|

0.049***

(0.019)

|

0.068***

(0.026)

|

0.042***

(0.016)

|

|

C

|

0.257*

(0.152)

|

0.382*

(0.223)

|

0.166*

(0.090)

|

0.193**

(0.096)

|

0.293***

(0.147)

|

0.106**

(0.049)

|

0.114***

(0.041)

|

0.171***

(0.062)

|

0.056***

(0.025)

|

|

R2

|

0.32

|

0.33

|

0.32

|

0.55

|

0.56

|

0.58

|

0.62

|

0.66

|

0.62

|

|

Wald chi-sq

|

59.03***

|

76.02***

|

45.76***

|

199.13***

|

141.51***

|

91.38***

|

197.58***

|

144.84***

|

187.99***

|

Note: Standard errors are shown in parentheses. ***, **, and * indicate that the variable is significant at the 1%, 5%, and 10% levels, respectively.

For the estimation methods, columns 1 to 3 represent the specifications using generalized two-stage least squares with fixed effects, columns 4 to 6 represent the specification using generalized two-stage least squares with random effects, while columns 7 to 9 represent the specifications using the error-correction two-stages least squares method.

The results in Table 3 show a robust negative impact of the central bank independence on inflation across the independence measures and the estimation methods. Our results support the findings of a large set of studies, specifically, (Agoba et al., 2017; Bodea et al., 2015; Hielscher & Markwardt, 2012).

Furthermore, we provide evidence for the persistence of inflation in the MENA countries. Our results show that the lag of inflation exerts a significant positive impact on the inflation rate, thereby corroborating the findings of (Agoba et al., 2017; Arnone & Romelli, 2013; Garriga & Rodriguez, 2020; Mackiewicz Łyziak & Kokoszczyński, 2020).

Our results suggest that there is a strong negative impact of institutional quality on the level of inflation in the MENA region. These results contrast the findings presented in the works of Agoba et al. (2017); and Hielscher & Markwardt (2012) who found evidence of such a relationship. Our results also show that the institutional quality positively moderates the impact of the central bank independence on inflation. A higher institutional quality in the MENA region reinforces the role of the central bank independence in reducing inflation. However, we found no evidence of an effect of the role of democracy in reducing inflation, direct or otherwise. These results are in line with the findings of Bodea et al. (2015); and Garriga & Rodriguez (2020) and in contrast with the results of Mackiewicz Łyziak & Kokoszczyński (2020) who found that countries with democratic institutions have a lower inflation.

The analysis of the control variables’ effects on inflation yields conflicting results. First, we show that the exchange rate regime has no impact on the inflation rate. The results are in line with the findings of Agoba et al. (2022) and Hielscher & Markwardt (2012) but in contrast to the results of Agoba et al. (2017), Garriga & Rodriguez (2020), Klomp & De Haan (2010a), and Mackiewicz Łyziak & Kokoszczyński (2020) who found that the fixed exchange rate regime is associated with a lower inflation. Second, our results show that oil dependency has a determinant impact on inflation, as net oil exporters have on average lower levels of inflation (Kchikeche & El Mahmah, 2022).

Moreover, it seems that imported inflation plays a critical role in the MENA region. According to our estimates, trade openness exerts a positive impact on inflation, as does the worldwide inflation, albeit to a lesser extent. : These results are in line with the findings of Agoba et al. (2017), Bodea et al. (2015), Garriga & Rodriguez (2020), and Strong (2021) who support the positive contemporaneous spillover effect of world inflation on domestic inflation. On the other hand, our results show a robust positive effect of trade openness on inflation, iin contrast to the findings of Klomp & De Haan (2010a), Mackiewicz Łyziak & Kokoszczyński (2020) who found that trade openness reduces inflation, and the findings of Arnone & Romelli (2013), Bodea et al. (2015) Garriga & Rodriguez (2020), and Hielscher & Markwardt (2012) who found no evidence of a significant relationship between these variables. Surprisingly, our results show that the output gap has no significant impact on the level of inflation in the MENA countries, which is a result that is consistent with the findings of Arnone & Romelli (2013).

5. Conclusion

Our study examines the impact of the central bank independence on inflation dynamics for a panel of 16 developing countries in the MENA group between 1990 and 2017. We reinforce the robustness of our results by using three measures of the central bank independence and three two-stage instrumental variables least squares estimators that address endogeneity and inflation persistence problems.

Our results show that the central bank independence robustly reduced inflation in the MENA region during the study period. Central bank independence has a negative impact on inflation, as a greater independence of the central bank allows for a greater control over prices. Our results also show that this impact is reinforced through institutional quality both directly and indirectly. Institutional quality has a significant negative impact on inflation. Moreover, institutional quality ameliorates the impact of the central bank independence on inflation. Hence, the independence of the central banks in the MENA region should play a reliable role in maintaining price stability.

The rising level of trade openness in the MENA countries, as a result of being major importers of manufactured goods and exporters of fossil fuels, subjected them to the spillover of fluctuations of prices in the global markets. Accordingly, the transmission of global market prices could explain both the positive effects of trade openness and world inflation.

Based on our results, policymakers in the MENA region are encouraged to grant more independence to monetary authorities. A credible monetary policy should play a more effective role in maintaining price stability in the region. In this context, a legal and statuary reform, while, for sure still insufficient in countries with weak political and judiciary institutions, is an essential step towards alleviating governmental pressure on the monetary authorities which hinders their ability to reduce inflation. On the other hand, more research should be conducted in order to evaluate the ability of de jure independence to grant real and effective autonomy to the central banks across the region.

Author contributions

Abdellatif Mouatassim: conceptualization, methodology, software, formal analysis, investigation, data curation; writing – original draft, visualization.

Ahmed Kchikeche: methodology, software, formal analysis, investigation, data curation, writing – review and editing, visualization.

Abderrazak El Hiri: conceptualization, validation, resources.

Abdellah Echaoui: conceptualization, validation, supervision, project administration, funding acquisition.

References

Acemoglu, D., Robinson, J. A., Johnson, S., & Querubin, P. (2008). When Does Policy Reform Work? The Case of Central Bank Independence (Working Paper 14033).

Agoba, A. M., Abor, J., Osei, K. A., & Sa-Aadu, J. (2017). Central bank independence and inflation in Africa : The role of financial systems and institutional quality. Central Bank Review, 17(4), 131–146. https://doi.org/10.1016/j.cbrev.2017.11.001

Agoba, A. M., Abor, J. Y., Osei, K. A., & Sa-Aadu, J. (2020). The Independence of Central Banks, Political Institutional Quality and Financial Sector Development in Africa. Journal of Emerging Market Finance, 19(2), 154–188. https://doi.org/10.1177/0972652719877474

Agoba, A. M., Fiador, V., Sarpong-Kumankoma, E., & Sa-Aadu, J. (2022). Central Bank Independence, Exchange Rate Regime, Monetary Policy and Inflation in Africa (pp. 183–225). https://doi.org/10.1007/978-3-031-04162-4_6

Agur, I. (2021). Central bank independence and low inflation: who leads the dance? Applied Economics Letters, 28(6), 477–481. https://doi.org/10.1080/13504851.2020.1761525

Aklin, M., & Kern, A. (2021). The Side Effects of Central Bank Independence. American Journal of Political Science, 65(4), 971–987. https://doi.org/10.1111/ajps.12580

Anwar, C. J. (2023). Heterogeneity Effect of Central Bank Independence on Inflation in Developing Countries. Global Journal of Emerging Market Economies, 15(1), 38–52. https://doi.org/10.1177/09749101221082049

Anwar, C. J., & Nicholas, O. (2020). Causality Relationship between Central Bank Reforms and Inflation: Evidence from Developing Countries. Jurnal Ilmu Ekonomi, 9(1), 15–30. https://www.researchgate.net/publication/339501777_Causality_Relationship_between_Central_Bank_Reforms_and_Inflation_Evidence_from_Developing_Countries

Afrouzi, H., Halac, M., Rogoff, K., & Yared, P. (2024). Changing Central Bank Pressures and Inflation. Brookings Papers on Economic Activity, 2004(1), 205–241. https://doi.org/10.1353/eca.2024.a943916

Armah, M. K. (2024). The effect of central bank credibility on economic growth and output volatility in inflation targeting regime. Journal of Social and Economic Development, 26(2), 619–640. https://doi.org/10.1007/s40847-023-00274-9

Arnone, M., & Romelli, D. (2013). Dynamic central bank independence indices and inflation rate : A new empirical exploration. Journal of Financial Stability, 9(3), 385–398. https://doi.org/10.1016/j.jfs.2013.03.002

Balestra, P., & Varadharajan-krishnakumar, J. (1987). Full Information Estimations of a System of Simultaneous Equations with Error Component Structure. Econometric Theory, 3(2), 223–246. https://doi.org/10.1017/S0266466600010318

Baltagi, B. H., & Chang, Y. (2000). Simultaneous Equations with Incomplete Panels. Econometric Theory, 16(2), 269–279. https://doi.org/10.1017/S0266466600162073

Barro, R.-J., & Gordon, D.-B. (1983). Rules, Discretion and Reputation Monetary Policy. Journal of Monetary Economics, 12(1), 101–121. https://doi.org/10.1016/0304-3932(83)90051-X

Binder, C. (2020). De Facto and De jure Central bank Independence. In E. Gnan & D. Masciandaro (Eds.), Populism, economic policies and central banking (p. 129). https://www.econstor.eu/bitstream/10419/234533/1/suerf-cp-2020-1.pdf

Binder, C. (2021). Political Pressure on Central Banks. Journal of Money, Credit and Banking, 53(4), 715–744. https://doi.org/10.1111/jmcb.12772

Bodea, C., Hicks, R., Bodea, C., & Hicks, R. (2015). Price Stability and Central Bank Independence : Discipline , Credibility , and Democratic Institutions. International Organization, 69(1), 35–61. https://doi.org/10.1017/S0020818314000277

Campillo, M., & Miron, J. A. (1997). Why does inflation differ across countries? In: Reducing Inflation: Motivation and Strategy. NBER Chapters, National Bureau of Economic Research, 335–362. https://doi.org/10.3386/w5540

Cargill, T. F. (1995). The statistical association between central bank independence and inflation. PSL Quarterly Review, 48(193), 159–172. https://doi.org/10.13133/2037-3643/10560

Center for Systemic Peace. (2021). The policy project. Retrieved September 9, 2021, from https://www.systemicpeace.org/polityproject.html

Cobham, D. (2021). A comprehensive classification of monetary policy frameworks in advanced and emerging economies. Oxford Economic Papers, 73(1), 2–26. https://doi.org/10.1093/oep/gpz056

Cukierman, A. (1992). Central bank strategy , credibility , and independence : theory and evidence MIT press. https://mitpress.mit.edu/9780262514477/central-bank-strategy-credibility-and-independence/

Cukierman, A., & Webb, S. B. (1995). Political Influence on the Central Bank : International Evidence. The World Bank Economic Review, 9(3), 397–423. https://doi.org/10.1093/wber/9.3.397

Cukierman, A., Webb, S. B., & Neyapti, B. (1992a). Measuring the independence of central banks and its effect on policy outcomes. The World Bank Economic Review, 6(3), 353–398. https://doi.org/10.1093/wber/6.3.353

Cukierman, A., Webb, S. B., & Neyapti, B. (1992b). Measuring the Independence of Central Banks and Its Effect on Policy Outcomes. The World Bank Economic Review, 6(3), 353–398. https://doi.org/10.1093/wber/6.3.353

Dall’Orto Mas, R., Vonessen, B., Fehlker, C., & Arnold, K. (2020). The case for central bank independence : A review of key issues in the international debate (248; Occasional Paper Series). https://doi.org/10.2866/908675

Fazio, M. D., Silva, C. T., Tabak, M. B., & Cajueiro, O. D. (2018). Inflation targeting and financial stability: Does the quality of institutions matter? Economic Modelling, 71(March 2017), 1–15. https://doi.org/10.1016/j.econmod.2017.09.011

Filiz, D., Papageorgiou, C., & Garbers, H. (2022). Monetary Policy Frameworks: An Index and New Evidence (WP/22/22; IMF Working Papers). https://www.imf.org/en/Publications/WP/Issues/2022/01/28/Monetary-Policy-Frameworks-An-Index-and-New-Evidence-512228

Freedom House. (2021). Institutional quality. Retrieved June 2, 2021, from https://freedomhouse.org/report/freedom-world.

Garriga, A. C., & Rodriguez, C. M. (2020). More effective than we thought: Central bank independence and inflation in developing countries. Economic Modelling, 85, 87–105. https://doi.org/10.1016/j.econmod.2019.05.009

Garriga, A. C., & Rodriguez, C. M. (2023). Central bank independence and inflation volatility in developing countries. Economic Analysis and Policy, 78, 1320–1341. https://doi.org/10.1016/j.eap.2023.05.008

Grilli, V., Masciandaro, D., & Tabellini, G. (1991). Political and monetary institutions and public financial policies in the industrial countries. Economic Policy, 6(13), 341–392. https://doi.org/https://doi.org/10.2307/1344630

Gyeke-Dako, A., Agbloyor, E. K., Agoba, A. M., Turkson, F., & Abbey, E. (2022). Central Bank Independence, Inflation, and Poverty in Africa. Journal of Emerging Market Finance, 21(2), 211–236. https://doi.org/10.1177/09726527221078434

Hielscher, K., & Markwardt, G. (2012). The role of political institutions for the effectiveness of central bank independence. European Journal of Political Economy, 28(3), 286–301. https://doi.org/10.1016/j.ejpoleco.2011.08.004

Hillman, A. L. (1999). Political Culture and the Political Economy of Central-Bank Independence. In Central Banking, Monetary Policies, and the Implications for Transition Economies (pp. 73–86). Springer, Boston, MA. https://doi.org/10.1007/978-1-4615-5193-5_5

IMF. (2021). Classification of Exchange Rate Arrangements and Monetary Policy Frameworks IMF staff reports. Recent Economic Developments; and International Financial Statistics. Retrieved April 26, 2021, from https://www.imf.org/external/np/mfd/er/2004/eng/0604.htm

Jácome, L. I., & Vázquez, F. (2008). Is there any link between legal central bank independence and inflation ? Evidence from Latin America and the Caribbean. European Journal of Political Economy, 24(4), 788–801. https://doi.org/10.1016/j.ejpoleco.2008.07.003

Jácome, L. I., & Pienknagura, S. (2022). Central Bank Independence and Inflation in Latin America—Through the Lens of History (WP/22/186). https://www.imf.org/en/Publications/WP/Issues/2022/09/16/Central-Bank-Independence-and-Inflation-in-Latin-America-Through-the-Lens-of-History-523542

Katseli, L. T., Theofilakou, A., & Zekente, K.-M. (2020). Central bank independence and inflation preferences: New empirical evidence on the effects on inflation. Economic Issues, 25(1), 2020. https://www.economicissues.org.uk/Files/2020/EI_March2020_katseli.pdf

Kchikeche, A., & El Mahmah, A. (2022). Is There Any Impact of Public Spending on Bank Performance? Empirical Evidence from the MENA Region (ERF Working Papers Series, 1555). https://erf.org.eg/publications/is-there-any-impact-of-public-spending-on-bank-performance-empirical-evidence-from-the-mena-region-2/

Klomp, J., & De Haan, J. (2010a). Central bank independence and inflation revisited. Public Choice, 144(3–4), 445–457. https://doi.org/10.1007/s11127-010-9672-z

Klomp, J., & De Haan, J. (2010b). Inflation And Central Bank Independence : A Meta-Regression. Journal of Economic Surveys, 24(4), 593–621. https://doi.org/10.1111/j.1467-6419.2009.00597.x

Krušković, B. D. (2022). Central Bank Intervention in Inflation Targeting. Journal of Central Banking Theory and Practice, 11(1), 67–85. https://doi.org/10.2478/jcbtp-2022-0003

Kydland, F. E., & Prescott, E. C. (1977). Rules Rather than Discretion : The Inconsistency of Optimal Plans. The Journal of Political Economy, 85(3), 473–492. https://doi.org/10.1086/260580

Lim, J. J. (2021). The limits of central bank independence for inflation performance. Public Choice, 186(3–4), 309–335. https://doi.org/10.1007/s11127-019-00771-8

Mackiewicz Łyziak, J., & Kokoszczyński, R. (2020). Central bank independence and inflation — Old story told anew. International Journal of Finance & Economics, 25(1), 72–89. https://doi.org/10.1002/ijfe.1730

Mourougane, A. (1997). Crédibilité, Indépendance et Politique Monétaire: Une revue de la littérature (G 9721; Série des documents de travail de la Direction des Etudes et Synthèses Économiques). https://www.bnsp.insee.fr/ark:/12148/bc6p06zqsg7

Rabhi, A., & Parsons, B. (2024). How is Central Bank Independence Shaping Income Inequality in Developing Countries? International Advances in Economic Research, 30(2), 159–176. https://doi.org/10.1007/s11294-024-09899-w

Reinhart, C. M., & Rogoff, K. S. (2004). The Modern History of Exchange Rate Arrangements: A Reinterpretation. The Quarterly Journal of Economics, 119(1), 1–48. https://doi.org/10.1162/003355304772839515

Reinhart, C. M., & Rogoff, K. S. (2009). The Aftermath of Financial Crises. American Economic Review, 99(2), 466–472. https://doi.org/10.1257/aer.99.2.466

Rogoff, K. (1985). The Optimal Degree of Commitment to an Intermediate Monetary Target. The Quarterly Journal of Economics, 100(4), 1169–1189. https://doi.org/10.2307/1885679

Romelli, D. (2022). The political economy of reforms in Central Bank design: evidence from a new dataset. Economic Policy, 37(112), 641–688. https://doi.org/10.1093/epolic/eiac011

Romelli, D. (2024). Trends in central bank independence: a de-jure perspective Trends in central bank independence: a de-jure perspective (BAFFI CAREFIN Working Papers No 217). https://repec.unibocconi.it/baffic/baf/papers/cbafwp24217.pdf

Strong, C. O. (2021). Political influence, central bank independence and inflation in Africa: A comparative analysis. European Journal of Political Economy, 69, 102004. https://doi.org/10.1016/j.ejpoleco.2021.102004

Takahashi, W. (2021). Central Bank Independence in a Changing Environment (pp. 13–42). https://doi.org/10.1007/978-981-16-4146-6_2

Visokavičienė, B. (2014). Monetary policy in advanced economies during the global financial crisis: lessons for lithuania. Ekonomika, 93(1), 40–56. https://doi.org/10.15388/Ekon.2014.0.3023

Vuletin, G., & Zhu, L. (2011). Replacing a “Disobedient” Central Bank Governor with a “Docile” One: A Novel Measure of Central Bank Independence and Its Effect on Inflation. Journal Of Money, Credit and Banking, 43(6), 1185–1215. https://doi.org/10.1111/j.1538-4616.2011.00422.x

Wachtel, P., & Blejer, M. I. (2020). A Fresh Look at Central Bank Independence. Cato Journal, 40(1), 105–132. https://doi.org/10.36009/CJ.40.1.7

Appendix 1.

Central Bank Independence Reforms in the MENA Region

Between 1990 and 2017

Employing a methodology based on analyzing changes in the components of the Central Bank Independence Index (CBIE), we track central bank reforms in the MENA region between 1990 and 2017. The approach relies on data from Romelli (2024), which includes the composite CBIE, its sub-components, and the specific items used to construct the sub-indices. Reforms are identified by examining modifications in each individual item, allowing for a detailed assessment of shifts in central bank independence. By focusing on these granular changes, the analysis ensures a precise classification of reforms by specific areas. This systematic approach provides a comprehensive understanding of the evolution of central bank independence in the region over the studied period and shows significant strides in improving Central bank independence in the MENA region. The complete list of central bank independence reforms is presented in Appendix 1.

|

Area of Reform

|

Country

|

Year

|

The specific reform

|

|

Governor and Central Bank Board

|

Bahrain

|

2006

|

- The governor’s term is set at five years, while other board members serve for four years.

- There are no provisions for the governor’s dismissal, which was previously linked to non-political reasons

|

|

Iraq

|

2004

|

- Dismissal of the governor is limited to non-political reasons. The governor and board members are prohibited from holding other government positions.

- The appointment process for board members has shifted from a collective executive decision to one made by one or more members.

- The board members’ term has been extended from four to five years.

- The staggering terms and the participation of government representatives have been modified.

|

|

Morocco

|

2006

|

- The governor is appointed by one or more members of the executive authority.

- The term of the other board members has changed from discretionary to a fixed duration of 6 to 8 years. Holding government positions is prohibited.

- The staggering of board members’ terms is now mandatory

|

|

Qatar

|

2012

|

- Qualification criteria are required for the governor and other board members.

|

|

Iran

|

2014

|

- No provisions exist for the governor’s dismissal.

- Qualification criteria are now required for the governor

|

|

Tunisia

|

2016

|

- The governor may serve a maximum of two terms.

- The appointment of board members is now collectively decided by the executive authority.

- Board members may serve only two consecutive terms.

|

|

Monetary Policy and Conflicts Resolution

|

Egypt

|

2003

|

- The central bank participates in monetary policy formulation with limited influence, whereas previously, its role was restricted to advising the government.

|

|

Yemen

|

2000

|

- The central bank’s role in monetary policy formulation has become exclusive. It has the final say in disputes.

|

|

Iraq

|

2004

|

|

Morocco

|

2006

|

|

Tunisia

|

2016

|

|

Objectives of Monetary policy

|

Yemen

|

2000

|

- Price stability has become the central objective of the bank, whereas it was previously associated with non-conflicting goals.

|

|

Algeria

|

2003

|

- Price stability is now linked to financial objectives that may conflict. Previously, price stability was associated with other competing goals, such as economic growth.

|

|

Iraq

|

2004

|

- Price stability is now associated with non-conflicting objectives, whereas it was previously linked to conflicting ones.

|

|

Morocco

|

2006

|

- Price stability becomes the bank’s primary objective, after being linked to economic growth

|

|

Limitations on Lending to the Government

|

Yemen

|

2000

|

- The maturity of advances to the government is within the next six months.

- The applicable interest rate is not specified.

|

|

Iraq

|

2004

|

- Advances and loans to the government are prohibited.

- Loan limits are defined in cash.

- The bank determines the financing conditions.

- The interest rate on advances is the market rate, with a maturity of six months.

- The central bank is prohibited from buying or selling government securities on the primary market.

|

|

Morocco

|

2006

|

- Loans to the government are subject to limits, with conditions set by the bank’s charter.

- The interest rate on advances is the market rate, with a maturity of six months.

- The central bank is prohibited from buying or selling government securities on the primary market.

|

|

Qatar

|

- Advances and loans to the government are subject to limits.

- Financing conditions are specified by the bank’s charter.

- The central bank’s loan limits are now proportional to public revenue.

- The maturity of advances is within six months.

|

|

Tunisia

|

- Advances and loans to the government are prohibited.

- Loan limits are defined in cash amounts. The bank alone determines the loan conditions.

- The interest rate on advances is the market rate, with a maturity of six months.

- The central bank is prohibited from buying or selling government securities on the primary market.

|

|

Jordan

|

2016

|

- Advances and loans to the government are prohibited, whereas they were previously allowed.

- The bank alone determines the government’s financing conditions.

- The central bank’s loan limits are defined in cash amounts.

- The maturity of advances is within the next six months. The interest rate on advances is the market rate.

|

|

Financial independence

|

Egypt

|

1993

|

- The bank’s status is now clearly defined, with exclusive rights over its annual budget.

- The status precisely quantifies the bank’s capital.

|

|

Morocco

|

2006

|

- The central bank now has the exclusive right to determine and approve its annual budget.

- The adoption of the central bank’s annual balance sheet is exclusively within the authority of its decision-making bodies

|

|

Bahrain

|

- The bank’s accounts are no longer audited by a government auditing agency.

|

|

Iraq

|

2004

|

- The government can now capitalize the central bank, which was not possible previously.

|

|

2017

|

- The central bank’s accounts are audited by an external auditing agency appointed by the government, whereas they have not been audited before 2017

|

|

Algeria

|

2016

|

- Automatic capital injection for the central bank.

- The decision to transfer funds from the Treasury to the central bank is based on technical criteria

|

|

Tunisia

|

- The central bank’s accounts are not audited by a national auditing agency.

|

|

Reporting and disclosure

|

Iraq

|

2004

|

- The central bank publishes financial statements at least once a year, accompanied by a certification from an independent auditor, whereas previously, they were under the seal of the banking superintendent or a public authority.

|

|

Tunisia

|

2006

|

Appendix 2.

Monetary Policy Framework and Objectives in the MENA Region

between 1990 and 2017

Building on the classification of monetary policy frameworks proposed by Cobham (2021) and utilizing the CBIE database compiled by Romelli (2024), we examine the successive changes in the monetary policy frameworks and objectives of MENA countries.

A detailed overview of these developments, covering the period from 1990 to 2017, is provided in the accompanying table.

|

Country

|

Monetary policy framework

|

Monetary policy objective

|

|

Algeria

|

[1990 -2017]: Loosely structured discretion (LSD)

|

[1990 -2002]: Price stability together with economic growth/development with no priority.

[2003 -2017]: Price stability plus other goals including financial stability of the financial system that may conflict with the former, without priority.

|

|

Bahrain

|

[1990 -1994]: Augmented exchange rate fix (AERF).

[1995 -2017]: Full exchange rate targeting (FERT)

|

[1990 -2005]: Price stability plus other goals including financial stability of the financial system that may conflict with the former, without priority.

[2006 -2017]: Objectives do not include price stability.

|

|

Egypt

|

[1990 -1991]: Unstructured discretion (UD).

[1992 -2002]: Loose exchange rate targeting (LERT).

[2003 -2017]: Loosely structured discretion (LSD).

|

[1990 -2017]: Price stability together with non-conflicting objectives but without priority.

|

|

Iran

|

[1990 -1998]: Unstructured discretion (UD).

[1999 -2017]: loosely structured discretion (LSD).

|

[1990 -2017]: Price stability together with economic growth/development with no priority.

|

|

Iraq

|

[1990 -2002]: Multiple direct controls (MDC).

[2003 -2006]: Unstructured discretion (UD).

[2007 -2017]: Augmented exchange rate fix (AERF).

|

[1990 -2003]: Price stability together with economic growth/development with no priority.

[2004 -2017]: Price stability plus other goals including financial stability of the financial system that may conflict with the former, without priority.

|

|

Jordan

|

[1990 -2000]: Loose exchange rate targeting (LERT).

[2001 -2017]: Full exchange rate targeting (FERT).

|

[1990 -2017]: Price stability plus other goals including financial stability of financial system that may conflict with the former, without priority.

|

|

Kuwait

|

[1990 -2002]: Loose exchange rate targeting (LERT).

[2003 -2006]: Full exchange rate targeting (FERT).

[2007 -2017]: Loose exchange rate targeting (LERT).

|

[1990 -2017]: Price stability plus other goals including financial stability of the financial system that may conflict with the former, without priority.

|

|

Lebanon

|

[1990 -1992]: Loosely structured discretion (LSD).

[1993 -1998]: Loose converging exchange rate targeting (LCERT).

[1999 -2017]: Full exchange rate targeting (FERT).

|

[1990 -2017]: Objectives do not include price stability.

|

|

Libya

|

[1990 -1991]: Augmented exchange rate fix (AERF).

[1992 -2001]: Unstructured discretion (UD).

[2002 -2013]: Augmented exchange rate fix (AERF).

[2014 -2017]: Unstructured discretion (USD).

|

[1990 -1995]: No data available.

[1996 -2017]: Price stability plus other goals including financial stability of the financial system that may conflict with the former, without priority.

|

|

Morocco

|

[1990 -1990]: Loosely structured discretion (LSD).

[1991 -2006]: Loose exchange rate targeting (LERT).

[2007 -2017]: Full exchange rate targeting (FERT).

|

[1990 -2005]: Price stability together with economic growth/development with no priority.

[2006 -2017]: Price stability is the single or primary objective.

|

|

Oman

|

[1990 -2017]: Augmented exchange rate fix (AERF).

|

[1990 -1999]: No data available.

[2000 -2017]: Price stability plus other goals including financial stability of the financial system that may conflict with the former, without priority.

|

|

Qatar

|

[1990 -1992]: Augmented currency board (ACB).

[1993 -2000]: Loose exchange rate targeting (LERT).

[2001 -2017]: full exchange rate targeting (FERT).

|

[1990 -1991]: No data available.

[1992 -2017]: Price stability plus other goals including financial stability of the financial system that may conflict with the former, without priority.

|

|

Saudi Arabia

|

[1990 -1999]: Loose exchange rate targeting (LERT).

[2000 -2017]: Full exchange rate targeting (FERT).

|

[1990 -2017]: Price stability plus other goals including financial stability of the financial system that may conflict with the former, without priority

|

|

Tunisia

|

[1990 -2017]: Loosely structured discretion (LSD).

|

[1990 -2015]: Price stability together with non-conflicting objectives but without priority.

[2016 -2017]: Price stability plus other goals including financial stability of the financial system that may conflict with the former, without priority.

|

|

United Arab Emirates

|

[1990 -1991]: Loose exchange rate targeting (LERT).

[1992 -2017]: Full exchange rate targeting (FERT).

|

[1990 -2017]: Price stability together with economic growth/development with no priority.

|

|

Yemen

|

[1990 -1994]: Unstructured discretion (UD).

[1995 -2014]: Loosely structured discretion (LSD).

[2015 -2017]: Unstructured discretion (UD).

|

[1990 -1999]: Price stability plus other goals including financial stability of the financial system that may conflict with the former, without priority.

[2000 -2017]: Price stability is the single or primary objective.

|

|

UD: Ineffective set of instruments and incoherent mix of objectives.

LSD: Instruments not effective or objectives not coherent or both only partly so.

FERT: Narrow announced stationary targets typically attained.

LERT: Narrow stationary targets not well hit or wider targets attained.

ACB: Domestic currency 100% backed by foreign currency, basic monetary instruments in use.

AERF: Exchange rate fixed by intervention, some basic monetary instruments in use.

MDC: Multiple exchange rates and/or controls on direct lending, interest rates, etc.

|

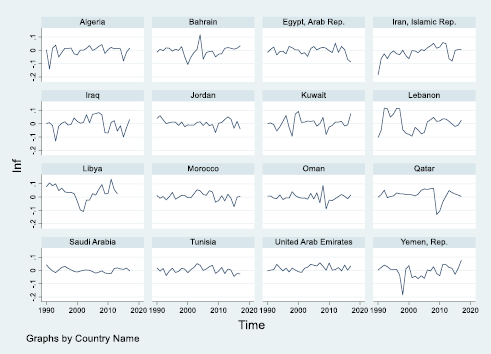

Appendix 3.

The evolution of the adjusted inflation rate in our sample

during the study period.