Ekonomika ISSN 1392-1258 eISSN 2424-6166

2025, vol. 104(3), pp. 103–123 DOI: https://doi.org/10.15388/Ekon.2025.104.3.6

Suhel

Department of Economic Development, Faculty of Economics, Sriwijaya University, Indonesia

Email: suhel@fe.unsri.ac.id

ORCID: https://orcid.org/0009-0002-6661-3275

Ariodillah Hidayat*

Department of Economic Development, Faculty of Economics, Sriwijaya University, Indonesia

Email: ariodillahhidayat@fe.unsri.ac.id

ORCID: https://orcid.org/0000-0002-6520-5985

Anna Yulianita

Department of Economic Development, Faculty of Economics, Sriwijaya University, Indonesia

Email: annayulia@unsri.ac.id

ORCID: https://orcid.org/0000-0001-8744-3274

Muhammad Teguh

Department of Economic Development, Faculty of Economics, Sriwijaya University, Indonesia

Email: mteguh1961@gmail.com

ORCID: https://orcid.org/0000-0003-2464-0494

Abstract. This study analyzes the influence of financial development and globalization on the gender inequality index in emerging Islamic countries. The sample of this study is Islamic countries with emerging market categories, including Malaysia, Indonesia, Türkiye, Saudi Arabia, Pakistan, Qatar, Egypt, Nigeria, and Iran. These countries are sampled in this study based on the magnitude of their GDP in the Islamic emerging countries group. The analysis technique in this study uses a panel data regression. The results show that financial institution access, depth, and efficiency, as well as the KOF globalization index are proven to be able to reduce the gender inequality index. Expansion of the network of financial institutions to remote areas is deemed to improve access for women, with special attention to women in emerging Islamic countries.

Keywords: gender inequality, financial development, globalization, emerging Islamic countries.

__________

* Correspondent author.

Received: 13/01/2025. Revised: 26/05/2025. Accepted: 26/05/2025

Copyright © 2025 Suhel, Ariodillah Hidayat, Anna Yulianita, Muhammad Teguh. Published by Vilnius University Press. This is an Open Access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

Gender inequality remains one of the worst issues hindering social and economic development in various countries, especially in developing countries. Gender inequality means an unequal distribution of wealth, power, and benefits between women and men. The Gender Inequality Index (GII) reflects the level of gender inequality in three main dimensions, namely health, empowerment, and participation in the labor market. This inequality not only creates barriers for women to access equal opportunities, but also affects the productivity and economic stability of a country. In the tradition of Islamic thought, there is a general consensus that men and women were created by God with equal status (Syed & Ali, 2019).

Financial development, which includes institutional access, depth, and the efficiency index, has great potential in reducing gender inequality. In the study by Kanat et al. (2023), investigating the impact of financial development on gender inequality and poverty in the context of Pakistan, long-term estimates show that financial development reduces gender imbalances. Financial institution access allows women to access economic resources, which is essential for empowering them economically. In emerging markets, many households and small businesses have limited access to formal financial services (Tsouli, 2022). According to Le Quoc (2024), financial development directly affects the economy and empowers economic actors – especially women who may face barriers to formal financial services – by providing avenues for the provision and utilization of capital, thereby optimizing economic resources. Meanwhile, financial efficiency ensures that resource allocation is carried out optimally without gender discrimination.

In addition to financial development that is able to overcome gender inequality, external factors, such as globalization, also play an important role in influencing gender inequality. One of the most commonly used globalization indices is the KOF Globalization Index (KOFGI) which covers economic, social, and political dimensions. Globalization plays a major role in accelerating economic and social development through trade, foreign investment, and technology transfer. On the other hand, the process of globalization can magnify gender inequality, especially when women do not have adequate access to economic resources, or when cultural norms limit their participation in the public sector and the job market.

This research will focus on Islamic countries that are included in the emerging market category, namely, Malaysia, Indonesia, Türkiye, Saudi Arabia, Pakistan, Qatar, Nigeria, and Iran. Previous literature tends to highlight gender inequality in developed or developing countries, while Islamic countries with emerging market categories are still limited. The novelty of this research lies in the relationship between financial development which includes access, depth, and efficiency of financial institutions to gender inequality in Islamic countries. The hypothesis of this study is that the development of the financial sector and globalization have an influence on gender inequality in developing Islamic countries, with the financial sector having the potential to reduce the negative impact of globalization on gender inequality.

The rest of this study is explained as follows. The second part will explore theories and concepts related to this research. The third section will describe the data and methods used in the paper. The fourth part will discuss the results. The fifth section will provide the conclusions and suggestions yielded by the paper.

GII reflects gender-based disadvantages in three dimensions – reproductive health, empowerment, and the labor market – for as many countries as possible wherever good quality data allows (Human Development Report, 2024). This indicates the loss of human development potential due to the inequality between the achievements of women and men in these dimensions. It ranges from ‘0’, where women and men have the same fate, to ‘1’, where one gender has the worst possible fate in all the dimensions measured.

Gender inequality limits women’s social interaction, independence, as well as their access to new information, which adversely affects their self-esteem and ability to express themselves. This inequality has an important impact on two main aspects of parenting: the physical and mental health of mothers and their autonomy over household resources (World Health Organization, 2024).

In the economy, gender inequality can be seen through wage gaps, women’s participation in the labor force, and women’s limited access to financial resources and entrepreneurial opportunities. Women’s participation in the workforce also tends to be lower than that of men, which is influenced by factors such as cultural norms, unequal domestic responsibilities, and a limited access to skills training and higher education. These barriers not only harm women, but also limit the overall economic growth potential, as research shows that gender equality in the workplace can increase productivity and innovation (Chung & Lippe, 2020).

The financial sector promotes economic growth through capital accumulation and technological advancement by increasing savings levels, mobilizing and accumulating savings, generating information about investments, facilitating and encouraging foreign capital inflows (World Bank, 2016). In emerging market countries, the financial sector is often not fully mature, and it does not support sustainable economic growth (Hidayat et al., 2023). Emerging market countries play a strategic role in international financial dynamics (Nurhaliza et al., 2024). Countries with more advanced financial systems tend to show more rapid economic growth. Various studies state that economic growth and financial development have a causal relationship.

The development of the financial sector plays an important role in reducing poverty and social inequality (Younsi & Bechtini, 2020). By expanding access to financial services for the poor and vulnerable, the financial sector is expected to be able to help them manage risk, reduce their vulnerability to economic shocks, and increase investment and productivity, which will ultimately increase people’s incomes.

Financial development is divided into three dimensions, namely depth, access, and efficiency (Bădîrcea et al., 2023). FID is measured by macroeconomic variables such as domestic credit to the private sector as a percentage of GDP, a measure of money supply, and stock market indicators. FIA refers to the ability of individuals and businesses to access the financial services they need, such as savings, loans, and payment services. FIE is concerned with how well the financial sector can provide financial services at an efficient cost and with the optimal allocation of resources. It includes measurements of the net margin, overhead costs, financial sector profitability, the market itself, and market liquidity.

The KOFGI is a composite index which measures globalization along the economic, social, and political dimensions for almost every country in the world on a scale of 1 to 100. Currently, the index covers the period from 1970 to 2016 (Haelg, 2020). The KOFGI was first introduced in 2006. Some of the variables from the 2007 version of the KOFGI were replaced, and many new variables, particularly those that measure the de jure characteristics of globalization, were introduced. The total number of underlying variables has increased from 23 to 43 compared to the previous version of the index (Gygli et al., 2019). The selection of the KOF Globalization Index in this study is based on its superiority in measuring globalization more comprehensively than other indices. The index not only considers economic aspects such as trade and investment, but also relevant social and political dimensions in analyzing structural changes in developing Islamic countries.

The three components of globalization include economic, social, and political aspects. Economic globalization is measured through real flows of trade, foreign direct investment (FDI), and portfolio investment, as well as the restrictions that apply to these flows. Meanwhile, social globalization is reflected in the spread of ideas, information, images, and people’s movements. This is estimated through a variety of indicators, such as international telephone traffic, money transfers, tourism, foreign population, and international mail; information flows (the number of Internet users, television ownership, newspaper trade); as well as cultural proximity (the number of McDonald’s restaurants, Ikea stores, and book trade).

This study examines the influence of FIA, FID, and FIE as well as the KOFGI on GII. The population in this study is Islamic countries, while the sample is Islamic countries with emerging market categories, including Malaysia, Indonesia, Türkiye, Saudi Arabia, Pakistan, Qatar, Egypt, Nigeria, and Iran. These countries are sampled in this study based on the magnitude of their GDP in the Islamic emerging countries group. This study uses panel data, with a series from 2003 to 2022.

|

Variable |

Definition |

Source |

|

GII |

The index covers three dimensions: reproductive health, empowerment, and economic status. |

Our World in Data |

|

FID |

The depth of financial institutions can be measured through several variables, such as the private sector credit ratio, the asset ratio of financial institutions, the M2 ratio, the deposit ratio, and the contribution of the financial sector’s gross added value to GDP. |

IMF |

|

FIA |

Access to financial institutions can be measured through several variables, such as the number of accounts per 1,000 adults in commercial banks, the number of branches per 1,000 adults in commercial banks, and the percentage of the population with bank accounts based on user surveys. |

IMF |

|

FIE |

Institutional efficiency is assessed by using net interest margins, the difference between loans and deposits, non-interest income to the total revenue, operating costs as a percentage of the total assets, profitability measured by ROA and ROE, and the Boone or Herfindahl index. |

IMF |

|

KOFGI |

The KOFGI measures the economic, social, and political dimensions of globalization. |

KOF Swiss Economic Institute |

Equation (1) is an econometric model in this study. This model is linear because it uses a panel linear regression approach. This model is commonly applied in economic and financial studies in analyzing the relationship between the variables. Linearity was chosen because it allows for a simpler interpretation and an efficient estimation of parameters.

Genderit = β0 + β1 FIAit + β2 FIDit + β3FIEit + β4 GI_KOFit + eit (1)

where: β is a constant; access is the FIA; depth is the FID; efficiency is the FIE; GI_KOF is globalization index by KOF; i is the cross-section; t is the time series; and e is the error term.

This study uses a panel data regression analysis technique using three approaches, namely, common, fixed, and random effect models. In choosing the best method, this study uses the Chow, Hausman, and Lagrange multiplier (LM) testing.

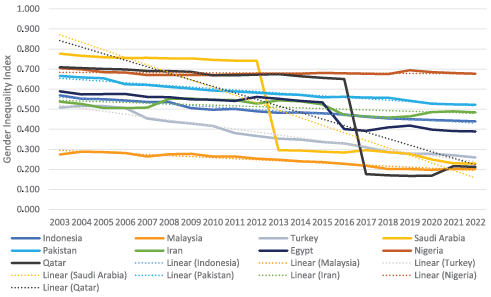

Inequality not only hinders the full realization of human potential but also hinders the overall economic growth and stability (Alawin & Sbitany, 2019). Based on Figure 2, Saudi Arabia shows fluctuating data. Saudi Arabia is one of the countries with the highest gender gap in the world, reflecting the high gender gap in economic and political empowerment (Syed et al., 2018). In 2013, GII showed a significant decline in Saudi Arabia as a result of the reforms under the leadership of Salman, which overhauled the position of women in the Saudi society. In 2017, a number of pro-women policies were introduced. This reform allows women to drive, access public facilities, as well as actively participate in the economy without male guardians (Topal, 2019).

Since 2017, Qatar has shown a significant decline in GII. According to the World Economic Forum (2017), more women occupy positions as legislators, senior officials, and managers. This shows an improvement in women’s access to high-quality jobs. In terms of education, more women completed secondary and tertiary education, which improved the scores of Qatar in the Educational Attainment sub-index.

In recent years, Nigeria is denoted by the highest score in GII, and it shows no decline. Historically, in Nigeria, certain tribes treated men favorably in terms of economic empowerment and heritage. Women are considered suitable for working in the kitchen and helping with work in the fields (Adeosun & Owolabi, 2021). This makes them dependent and submissive to men. In Nigeria, women dominate the unpaid work sector, by generating double the figure for men. Pakistan showed a fairly high GII, but it began to decline. The Pakistan society is still being affected by a strong patriarchal structure. However, there are several efforts in Pakistan, such as the Alternative Learning Program (ALP) which provides alternative education for children who are not enrolled in formal schools, including girls (Pasha, 2024).

Iran, Indonesia, and Egypt showed a slight downward trend in the GII scores. Iran’s gender inequality is greatly influenced by the Sharia Law which restricts women’s rights in social and political aspects, including the obligation to wear the hijab and restrictions on women’s participation in politics and certain sectors of activity. Meanwhile, in Indonesia, women’s rights to work still clash with the role of women in the public sector. Currently, discrimination against women is still very visible in the world of work (Larasati, 2021).

Türkiye showed a significant decrease in GII compared to the other countries studied. Türkiye is proven to have a higher ratio of women regarding participation in scientific research and teaching. Malaysia has the lowest GII and is on a downward trend. Women’s account ownership rates in Malaysia are higher compared to East Asia and Pacific and upper-middle-income groups (World Bank, 2023).

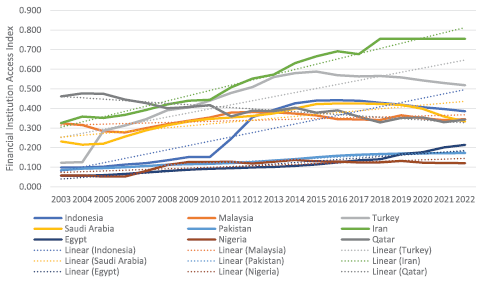

Better access to financial services can improve a company’s ability to access funds for investment (Hidayat & Shodrokova, 2024). Based on Figure 3, Iran, Türkiye, and Indonesia show the highest upward trend in the FIA index. Iran has implemented reforms in the banking and financial sectors in an effort to increase financial inclusion. Türkiye is taken forward by economic policies that support the digitalization and technological integration of the banking sector. Indonesia, through government programs such as financial inclusion and fintech development, has succeeded in increasing access to financial services in various regions (Rufaidah et al., 2023).

Saudi Arabia, Qatar, and Malaysia also show an upward trend, but not as high as the three countries discussed above. Saudi Arabia, with programs such as the Financial Sector Development Program under the 2030 vision, aims to increase financial access for the public (Noreen, 2024). Qatar has invested in modernizing the banking and financial technology sectors, as well as introducing various policies to encourage financial inclusion (Dahdal et al., 2020). Meanwhile, Malaysia has been increasing access to financial institutions through the fintech and microfinance sectors.

Egypt, Nigeria, and Pakistan showed the lowest FIA and tended to be flat. The main challenges facing Egypt are its limited infrastructure, political tensions, and economic problems (Hertog, 2017). Nigeria, as one of the most populous countries in Africa, faces a major challenge in terms of unequal access in various regions. The high dependence on the informal sector and the lack of trust in the banking system have led to individuals and small businesses not having access to banking and other financial products (Etim & Daramola, 2020).

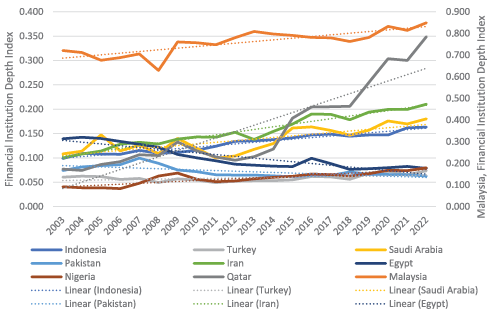

Based on Figure 4, Malaysia leads the FID score in emerging Islamic countries. As an emerging country with a Muslim majority, Malaysia is relatively more mature, with many financial products such as sukuk and sharia bonds that allow investors to engage in financial instruments that are in accordance with the sharia principles. Bank Negara Malaysia (BNM) also plays an active role in improving the stability and sustainability of the financial system.

Qatar shows a significant increase in FID. Qatar’s Third National Development Plan (2024–2030) prioritizes financial services as part of the country’s economic diversification plan. These goals include maintaining a high standard of living for all Qatari citizens, promoting and expanding domestic capacity for innovation and entrepreneurship, and aligning economic outcomes with economic and financial security (Al-Sulaiti et al., 2024).

Türkiye and Nigeria show low FIDs, experiencing a gradual upward trend. Türkiye often experiences high economic volatility, especially related to fluctuations in the Turkish Lira’s exchange rate, high inflation, and external pressures on the financial sector (Ozkaya & Altun, 2024). The financial system in Türkiye is still dominated by banks, while the capital market is less developed. However, Türkiye has introduced various policies with the objective to reduce dependence on the banking system and increase the role of the non-bank financial sector. Meanwhile, in Nigeria, despite having a sizable banking sector, public access to financial services is still limited. According to data from the Central Bank of Nigeria and the Global Findex, the percentage of the population that has a bank account is still relatively low compared to other developing countries (Demirguc-Kunt et al., 2018). In addition, MSMEs in Nigeria face major challenges in gaining access to credit. Banks prefer to provide loans to large companies or sectors that are considered to be lower risk.

Iran, Saudi Arabia, and Indonesia show a similar trend, with a slight upward motion. Iran has focused on strengthening the financial system through reforms that respond to domestic needs and external challenges. However, there are obstacles, such as international sanctions, limiting growth. Saudi Arabia, through its Vision 2030, reduces dependence on oil by developing financial markets (Nurunnabi, 2017). Indonesia, through its Vision 2045, focuses on improving the financial sector, banking assets, and other financial services. One of them is the National Strategy for Financial Inclusion (SNKI) (Soedarmono et al., 2019). Egypt and Pakistan showed a downward trend in FID. Egypt has been facing economic problems such as inflation. Whereas, Pakistan suffers from major political instability, economic volatility, and informal economy.

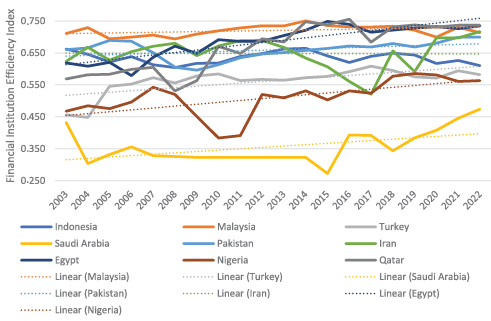

FIE measures how efficiently financial institutions in a country manage resources to provide services and generate profits. Based on Figure 5, all emerging Islamic countries studied have been showing an increasing trend. Qatar and Malaysia are the highest in the FIE scores. Qatari banks have improved the management of lower operating costs, due to an increased efficiency in operations. Qatar Central Bank (QCB) has introduced a policy to digitize payment systems and fintech, which reduces bank operating costs (Ali & Singh, 2024). Malaysia, through the Financial Sector Blueprint (FSB) initiative, has improved the efficiency of its banking system.

Pakistan, Iran, Indonesia, and Türkiye showed a flat trend, with Türkiye being more volatile. Net interest margins in Pakistan tend to be low and less stable, due to the reliance on financing from expensive external sources, as well as the relatively high rate of bad loans. Iran’s banking system is still trying to improve efficiency due to its reliance on the country’s industry and international sanctions that limit innovation. Indonesia has a stable banking system. In addition, Indonesia continues to strive to increase non-interest income through digital financial service innovation. Credit restructuring by large banks is often carried out to reduce the risk of bad loans, such as during the times of COVID-19 (Damayanthi et al., 2022).

Egypt shows a slight upward trend in the FIE, with the FIE level ranging between 0.60 and 0.75. The Central Bank of Egypt has strengthened its financial inclusion strategy, including the strengthening of digital banking services and electronic payment systems. Economic reforms that began in 2016 with the support of the IMF have helped improve the competitiveness of Egypt’s financial sector. However, Egypt still faces problems in the urban-rural gap, since financial access is still concentrated in urban areas. Furthermore, according to Hassouba, (2023), in Egypt, incentives for firms and small households to use deposits and other financial products are not strong enough. The minimum amount of mandatory savings is high enough to prevent the poor(er) population from engaging in the banking system.

Nigeria is showing a fairly high upward trend in the FIE. On the other hand, Saudi Arabia is the lowest in FIE with an upward trend. Nigeria is strengthening the banking sector with increased banking regulations and an increased supervision. This supports the increase in NIM. Innovations, such as mobile banking and digital payments, are improving the access to and efficiency of financial services. In terms of the Saudi Arabia banking sector, changes in oil prices greatly affect the income stability and slow down the improvement of the operational efficiency of its banks.

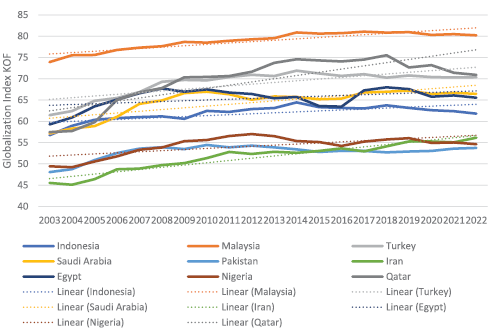

The consequences of the era of globalization will have great implications for economic development (Hidayat et al., 2021). Globalization is accompanied with changes in the role of institutions, society, businesses, countries, and international organizations (Kuz & Miskinis, 2021). Based on Figure 6, the KOFGI in emerging Islamic countries shows an increasing trend. Malaysia is the highest in the KOFGI. However, despite Malaysia being in the top position, Qatar shows a very significant upward trend in this index. This is attributed to several policies that support Qatar’s integration into the global economy and politics, as well as massive investments in the infrastructure and the energy sector that strengthen international relations. In 2010, Qatar became the world’s number one exporter of liquefied natural gas (LNG). During the same period, Qatar also established itself as a diplomatic player with proactive and multidimensional foreign policy engagements (Miller, 2020).

Türkiye shows the third highest KOFGI in emerging Islamic countries. Türkiye has adopted a policy of encouraging its openness to the global economy through trade agreements and its strategic position at the crossroads of Europe and Asia (Güneylioğlu, 2022). Türkiye also promotes cultural diplomacy by hosting various international events. The G20 organization, NATO, and the United Nations make Türkiye an important factor in the world.

Egypt, Indonesia, and Saudi Arabia showed a flat trend. Although all three have large economies, domestic policies, political issues (for example, in Saudi Arabia and Egypt) limit the progress in globalization. Saudi Arabia maintains a stable level of globalization compared to other countries in the MENA region. These three countries are the main members of the Organization of Islamic Cooperation (OIC). Indonesia strengthens its involvement in the global trade and foreign investment. The NEOM project in Saudi Arabia was designed to help the country become a global center for innovation, business, and technology (Aldusari, 2023).

Nigeria, Iran, and Pakistan are the lowest in the KOFGI. Nigeria relies heavily on oil exports, which limits economic diversification and the development of other sectors that can support global integration (Anyaehie & Areji, 2015). Iran is hampered by international sanctions that affect its trade flows. Pakistan and Iran have political systems that restrict social exchanges.

Table 2 presents the results of the unit root test using the Augmented Dickey-Fuller (ADF) method intended to examine the stationarity of the variables. The results show that all variables are statistically significant and stationary at the level, without the need for differencing. This is indicated by the significant ADF statistics at level for all variables: Gender was found to be significant at the 5% level, whereas FIA, FID, FIE, and GI_KOF were all significant at the 1% level. Therefore, all variables are categorized as I(0), or integrated at order zero. This implies that the data meet the requirements for applying a static panel regression analysis, such as the Fixed Effect Model (FEM), without the need for further transformation.

Based on Table 3, the Chow test with a value of 0.00 is more fixed effect than pooled OLS, which means that this model is better at handling differences between individuals. The Hausman test chose a fixed effect over random effect. Hence, the best model in this study is FEM.

|

Variable |

Augmented Dickey Fuller |

|

|

Level |

1st Difference |

|

|

Gender |

-2.3032** |

-4.0561*** |

|

FIA |

35.519*** |

39.991*** |

|

FID |

5.0398*** |

8.7544*** |

|

FIE |

37.488*** |

75.588*** |

|

GI_KOF |

74.700*** |

34.601** |

|

Variable |

Coefficient |

Std. Error |

t-Statistic |

Prob. |

|---|---|---|---|---|

|

C |

1.250 |

0.131 |

9.481 |

0.000*** |

|

FIA |

-0.160 |

0.044 |

-3.597 |

0.001*** |

|

FID |

-0.403 |

0.166 |

-2.419 |

0.016** |

|

FIE |

-0.287 |

0.105 |

-2.719 |

0.007*** |

|

GI_KOF |

-0.007 |

0.002 |

-3.338 |

0.001*** |

|

R-squared |

0.863 |

|||

|

Adjusted R-squared |

0.853 |

|||

|

F-statistic |

87.860 |

|||

|

Prob(F-statistic) |

0.000 |

|||

|

Cross-section Effect |

Model Selection Test |

|||

|

Indonesia_ |

-0.023 |

Chow Test |

0.000 |

Fixed Effect |

|

Malaysia_ |

0.138 |

Hausman Test |

0.000 |

Fixed Effect |

|

Turkey_ |

-0.110 |

LM Test |

0.000 |

Random Effect |

|

Saudi Arabia_ |

-0.051 |

|||

|

Pakistan_ |

-0.039 |

|||

|

Qatar_ |

0.109 |

|||

|

Egypt_ |

-0.013 |

|||

|

Nigeria_ |

0.013 |

|||

|

Iran_ |

-0.023 |

|||

|

Classical Assumption Test |

||||

|

Normality Test |

0.1878 |

|||

|

Jarque-Bera |

3.3446 |

|||

|

Heteroscedasticity Test |

||||

|

C |

0.000916 |

0.000744 |

1.232354 |

0.2195 |

|

Access |

0.000261 |

0.000279 |

0.936960 |

0.3501 |

|

Depth |

-0.000421 |

0.000918 |

-0.457966 |

0.6476 |

|

Efficiency |

0.000147 |

0.000417 |

0.351486 |

0.7257 |

|

Multicollinearity Test |

||||

|

Access |

Depth |

Efficiency |

GI_KOF |

|

|

Access |

1 |

0.1735 |

0.0159 |

0.2395 |

|

Depth |

0.1735 |

1 |

0.3759 |

0.6457 |

|

Efficiency |

0.0159 |

0.3759 |

1 |

0.2164 |

|

GI_KOF |

0.2395 |

0.6457 |

0.2164 |

1 |

|

Residual Cross-Section Dependence Test |

||||

|

Test |

Statistics |

d.f. |

Prob |

|

|

Breusch-Pagan LM |

28.02571 |

36 |

0.8263 |

|

|

Scaled LM marketing |

-0.939779 |

0.3473 |

||

|

Bias-corrected scaled LM |

-1.176621 |

0.2393 |

||

|

CD Marketing |

0.575080 |

0.5652 |

||

All of the independent variables showed probability levels below alpha 5 and 10 percent, which means that they all had a significant effect. The value of the constant is 1.251, from which, it follows that if the values of FIA, FID, FIE and KOFGI are all zero, then, the prediction value for the dependent variable is 1.251. The FIA with a value of -0.1603 indicates that if the access increases by one unit, the GII variable will decrease by 0.1603, assuming that the other variables remain constant. The FID coefficient is -0.4039, indicating that every unit of increase in depth will reduce the GII value by -0.403 assuming that the other variables are constant. The FIE variable has a coefficient of -0.2877, which means that if there is an increase in FIE by one unit, then, GII will decrease by 0.287. The KOFGI shows a coefficient of -0.007 which indicates that an increase in KOFGI by 1 unit will decrease the GII score by 0.0073. The results of this calculation are in accordance with the hypothesis and variable movement discussed in the previous section.

Based on the results of the normality test, the results showed that the probability value was 0.1878, which was higher than the significance level of 0.05 percent. This indicates that the residual in the model is normally distributed. The heteroscedasticity test showed probability values for all variables above 0.05, which means that the residual variance was constant, and that the model met the assumption of homoscedasticity. Meanwhile, the multicollinearity results showed that all correlations between the variables were below 0.08, suggesting that there were no serious multicollinearity problems in the model. The cross-section dependence test is also used to determine if there is a dependency between cross-section units in the panel data. The Breusch-Pagan LM, Pesaran, bias-corrected scaled LM, and CD Pesaran tests showed a probability of more than 0.05 each. This means that the assumption of independence between cross-sections is met.

The FIA index is able to significantly reduce gender inequality in emerging Islamic countries. The Islamic financial system often offers products that are more accessible to women, by adhering to the sharia principles that are in accordance with Islamic religious values. Financial products, such as sharia microfinance, allow women to obtain capital without having to be involved in transactions that are considered haram in Islam such as riba or interest (Rovera, 2022). Fintech has a big role to play in providing financial access without requiring women to leave the house. Islamic finance apps, like Zapp Islamic, enable transactions in accordance with the Islamic principles, fintech enables women in countries with more conservative social norms to continue to access financial services easily and without violating religious rules (Bakri et al., 2023; Pati et al., 2021). Saudi Arabia, with its strong sharia-based financial system, has implemented policies that are more open to women in the economic sector.

An increased access to better and more transparent credit information means that women can have a greater chance of getting loans and financial services compared to earlier periods. Countries that have a large educational gap between women and men tend to have greater inequality in access to financial services. Low education levels achieved by women reduce their ability to understand and access existing financial services. According to Morsy (2020), achieving gender equality in financial inclusion is a crucial step in unlocking resources for economic empowerment and growth by expanding access to economic opportunities for the broader society. It is also important at the micro level, as it improves women’s lives by giving them a voice and improving their decision-making abilities.

The FID index shows a negative and significant influence on GII in emerging Islamic countries. FID is directly related to the availability of diverse and in-depth financial services, helping in lowering gender inequality. When women have a greater access to microloans, insurance, and financial services, they are more enabled to participate in economic activities, such as building businesses and managing household finances. In many emerging countries, especially Islamic countries, women often face barriers to accessing deeper financial services. Specifically, it emphasizes the importance of increasing financial inclusion as a strategy to decrease gender inequality and boost economic growth. The principle of gender justice in Islam affirms that men and women have the same rights and responsibilities in various aspects of life. Research by Baeshen et al. (2023) shows that economic strength, social and institutional environment, as well as banking and technology market conditions are one of the determining factors for reducing gender inequality.

Pakistan has a program, called Kamyab Jawan, that provides financing for women’s small businesses (Shah & Ahmad, 2024). Sharia-based banks, such as Meezan Bank, have launched financial inclusion products designed for women. Indonesia has a thriving Islamic finance sector with a focus on financial inclusion, but the challenge is financial access for women in remote areas. Malaysia has a more mature financial system than other Islamic countries. Digital services, such as e-wallets, also expand women’s access to the financial system. Takaful and Karama represent a social program that provides women with access to financial services in Egypt. A large Muslim population has a developing Islamic financial system. Sharia-based financial developments, such as Jaiz Bank, help increase women’s access to sharia financing.

The results show that FIE is able to reduce the GII value in emerging Islamic countries. The efficiency of financial institutions in providing fast, cheap, and easily accessible services will increase financial inclusion for women. With more efficient operational activities, transaction costs will be lower, and more services will be available for women, especially in remote areas. Financial institutions are required to operate with the principles of transparency and accountability, helping to create a fair system for women in accessing financing. Disclosure of information and clear policies in profit-sharing financing can reduce uncertainty and potential exploitation (Supriatiningsih, 2018). With a clear and transparent structure, employees are able to understand the products and services offered, thereby increasing their trust and participation in the financial sector.

Many Islamic financial institutions are directly involved in social empowerment through financing that focuses on poverty reduction and improving the quality of life, especially for women. Through waqf, zakat, and sadaqah financing, financial institutions participate in skills training, education, and micro business support (Diniyya, 2019). Islamic financial institutions not only focus on financial gain, but also invest in social causes and women’s empowerment, which, in turn, is able to reduce gender inequality. Efficient financial institutions can develop microfinance programs, offering small loans to women with the objective to start their own businesses. With low operating costs and high non-interest income, financial institutions can reduce barriers for low-income women to access financing. Malaysia has policies that encourage women to start businesses, such as the Women Entrepreneur Financing Scheme which offers low-interest financing for women (Andrew et al., 2024). In Pakistan, the Poverty Alleviation Fund (PPAF) provides microloans to women (Ali et al., 2023).

The KOFGI is able to significantly reduce GII. Economic globalization is able to increase trade, investment, and capital flows between countries. This allows opening up access to women to the international job market, allowing them to have better jobs, expand career options, and get more equal salaries. Countries with higher levels of globalization also tend to have better access to technology and innovation. This technology will help women in developing their skills and participating in more modern sectors of the economy. Foreign investment can be allocated in education and health, which helps women acquire the skills and knowledge needed to work in the formal sector. Women have been shown to experience discrimination in Muslim-majority countries. For example, girls and women experience discrimination in the education system and the labor market, as well as in electoral participation.

From the social dimension, the existence of information transfer, cultural exchange, and international social networks can lead to an increased awareness of women’s rights. Countries that are more globally connected are more likely to adopt gender equality values and introduce policies that are more supportive of women. In social globalization, it also allows the spread of ideologies and movements that support gender equality. From the political side related to international cooperation, multilateral organizations and international agreements also encourage gender equality. Countries that are more open to democratic governance tend to provide more opportunities for women to participate in the policy-making process. Political globalization brings positive things, such as the efforts by the United Nations, which supports women’s empowerment.

Malaysia, as a more globally integrated country, has policies that support women in education, health, and work. Indonesia has also experienced an increase in employment opportunities for women thanks to the influence of globalization. Thus, these countries have been helping women in increasing their income. Studies show that, in Pakistan, there are differences between women and men in terms of health, education, income opportunities, employment both at home and abroad, personal security, control over assets, and participation in politics (Ashraf & Ali, 2018).

The number of women entering the workplace in Saudi Arabia and other Middle Eastern countries has been increasing. Patriarchal structural traits are changing in Middle Eastern societies and workplaces, but women’s experiences of gender segregation, underrepresentation, and exclusion still involve challenges (Aldossari & Calvard, 2023). However, Islam encourages both men and women to seek knowledge. Saudi Arabia supports globalization, and its Vision 2030 opens higher education opportunities for women with Islamic norms. In Qatar, the female labor force participation rate remains low despite an increase in higher education, where women are better educated yet less active in the job market (Zweiri & Al Qawasmi, 2021).

This study shows that financial institution access, depth, efficiency, and KOFGI all have a significant role in reducing gender inequality in developing Islamic countries. These results are in accordance with the proposed hypothesis. Access to inclusive financial institutions, sharia-based financial products, and the adoption of fintech have helped women, especially in countries with conservative social norms, to participate in the economy without violating religious rules. The depth and efficiency of financial institutions also expands women’s opportunities to access diverse and affordable financial services, such as microfinance and zakat, that support their economic empowerment. Globalization plays an important role through improving women’s access to international job markets, education, and technology, as well as strengthening gender equality policies through multilateral cooperation and cultural exchanges.

Emerging Islamic countries need to improve inclusive and sharia-based financial infrastructure, including the expansion of digital financial services in remote areas. Policies that encourage women’s financial inclusion, such as sharia-based microfinance programs, must be strengthened and integrated with financial education to increase women’s literacy. In addition, international cooperation needs to be increased to encourage the adoption of policies that support gender equality, including through global organizations such as the United Nations. The government is also advised to encourage foreign investment focusing on women’s education and health, so that they are better prepared to face the challenges of globalization and contribute to sustainable economic development.

Adeosun, O. T., & Owolabi, K. E. (2021). Gender inequality: determinants and outcomes in Nigeria. Journal of Business and Socio-Economic Development, 1(2), 165–181. https://doi.org/10.1108/jbsed-01-2021-0007

Al-Sulaiti, A., Hamouda, A. M., Al-Yafei, H., & Abdella, G. M. (2024). Innovation-Based Strategic Roadmap for Economic Sustainability and Diversity in Hydrocarbon-Driven Economies: The Qatar Perspective. Sustainability (Switzerland) , 16(9). https://doi.org/10.3390/su16093770

Alawin, M., & Sbitany, N. (2019). Gender inequality and economic development in the MENA region. Applied Econometrics and International Development, 19(1), 81–94.

Aldossari, M., & Calvard, T. (2023). The Politics and Ethics of Resistance, Feminism and Gender Equality in Saudi Arabian Organizations. Journal of Business Ethics, 181, 873–890. https://doi.org/10.1007/s10551-021-04949-3

Aldusari, A. N. (2023). Strategic Development Plan Proposed for the Future City NEOM. Cities of the Future, 57–74. 10.1007/978-3-031-15460-7_5

Ali, A. O. M. M., & Singh, A. (2024). Security And Privacy Of Mobile Banking In Qatar : A Case Highlighting Current Challenges And Future Recommendations. Library Progress International, 44(3), 11558–11566. https://bpasjournals.com/library-science/index.php/journal/article/view/2479/1618

Ali, Z., Asif, M., Nazir, N., Ur Rehman Irshad, A., Ullah, I., & Ahmad, S. (2023). Financial and social efficiency of microcredit programs of partner organizations of Pakistan Poverty Alleviation Fund. PLoS ONE, 18(3 MARCH), 1–17. https://doi.org/10.1371/journal.pone.0280731

Andrew, L., Yusuf, M. J., Bujang, A., Wan Ibrahim, W. M. F., Hassan, S. S., Ali, J. K., & Yacob, Y. (2024). The State of Women’s Co-operatives in Malaysia: Challenges and Opportunities. International Journal of Academic Research in Economics and Management Sciences, 13(1), 168–183. https://doi.org/10.6007/ijarems/v13-i1/20433

Anyaehie, M. C., & Areji, A. C. (2015). Economic Diversification for Sustainable Development in Nigeria. Open Journal of Political Science, 05(02), 87–94. https://doi.org/10.4236/ojps.2015.52010

Ashraf, I., & Ali, A. (2018). Socio-economic well-being and women status in Pakistan: an empirical analysis. Bulletin of Business and Economics (BBE), 88972, 130–174. https://bbejournal.com/index.php/BBE/article/view/174%0Ahttps://bbejournal.com/index.php/BBE/article/download/174/130

Bădîrcea, R. M., Doran, N. M., Manta, A. G., Puiu, S., Meghisan-Toma, G. M., & Doran, M. D. (2023). Linking financial development to environmental performance index—the case of Romania. Economic Research-Ekonomska Istrazivanja, 36(2). https://doi.org/10.1080/1331677X.2022.2142635

Baeshen, L., Girardone, C., & Sarkisyan, A. (2023). Financial Inclusion and the Gender Gap Across Islamic and Non-Islamic Countries. In Contemporary Issues in Sustainable Finance. Springer. https://link.springer.com/chapter/10.1007/978-3-031-22539-0_10

Bakri, M. H., Almansoori, K. K. S. M., & Azlan, N. S. M. (2023). Determinants intention usage of Islamic E-Wallet Among Millennials. Global Business and Finance Review, 28(1), 11–32. https://doi.org/10.17549/gbfr.2023.28.1.11

Chung, H., & van der Lippe, T. (2020). Flexible Working, Work–Life Balance, and Gender Equality: Introduction. Social Indicators Research, 151(2), 365–381. https://doi.org/10.1007/s11205-018-2025-x

Dahdal, A., Truby, J., & Botosh, H. (2020). Trade finance in Qatar: blockchain and economic diversification. Law and Financial Markets Review, 14(4), 223–236. https://doi.org/10.1080/17521440.2020.1833431

Damayanthi, I. G. A. E., Wiagustini, N. L. P., Suartana, I. W., & Rahyuda, H. (2022). Loan restructuring as a banking solution in the COVID-19 pandemic: Based on contingency theory. Banks and Bank Systems, 17(1), 196–206. https://doi.org/10.21511/bbs.17(1).2022.17

Demirguc-Kunt, A., Klapper, L., Singer, D., Ansar, S., & Hess, J. (2018). The Global Findex Database 2017: Measuring Financial Inclusion and the Fintech Revolution. Washington, DC: World Bank. https://doi.org/10.1596/978-1-4648-1259-0

Diniyya, A. A. (2019). Development Of Waqf Based Microfinance And Its Impact In Alleviating The Poverty. Ihtifaz: Journal of Islamic Economics, Finance, and Banking, 2(2), 107. https://doi.org/10.12928/ijiefb.v2i2.879

Etim, E., & Daramola, O. (2020). The informal sector and economic growth of South Africa and Nigeria: A comparative systematic review. Journal of Open Innovation: Technology, Market, and Complexity, 6(4), 1–26. https://doi.org/10.3390/joitmc6040134

Güneylioğlu, M. (2022). The Turkey-China rapprochement in the context of the BRI: a geoeconomic perspective. Australian Journal of International Affairs, 76(5), 546–574. https://doi.org/10.1080/10357718.2022.2076805

Gygli, S., Haelg, F., Potrafke, N., & Sturm, J. E. (2019). The KOF Globalisation Index – revisited. Review of International Organizations, 14(3), 543–574. https://doi.org/10.1007/s11558-019-09344-2

Haelg, F. (2020). The KOF globalisation index - A multidimensional approach to globalisation. Jahrbucher Fur Nationalokonomie Und Statistik, 240(5), 691–696. https://doi.org/10.1515/jbnst-2019-0045

Hassouba, T. A. (2023). Financial inclusion in Egypt: the road ahead. Review of Economics and Political Science. https://doi.org/10.1108/REPS-06-2022-0034

Hertog, S. (2017). The Political Economy of Distribution in the Middle East: Is There Scope for a New Social Contract? In International Development Policy (Vol. 7). https://doi.org/10.1163/9789004336452_006

Hidayat, A., Liliana, L., & Andaiyani, S. (2021). Factors Affecting the Composite Stock Price Index during Covid-19 Pandemic Crisis. Jejak, 14(2), 333–344. https://doi.org/10.15294/jejak.v14i2.27682

Hidayat, A., Liliana, L., Harrunurasyid, H., & Shodrokova, X. (2023). The Relationship Between Financial Development and the Composite Stock Price Index in Emerging Market Countries : A Panel Data Evidence. Organizations and Markets in Emerging Economies, 14(3), 621–643. https://doi.org/10.15388/omee.2023.14.8

Hidayat, A., & Shodrokova, X. (2024). The Impact of Banking Penetration on Foreign Direct Investment in ASEAN : Comparative Analysis. Innovation and Economics Frontiers, 27(2), 45–56. https://doi.org/10.36923/iefrontiers.v27i2.245

Human Development Report. (2024). Gender Inequality Index (GII). Human Development Report. https://hdr.undp.org/data-center/thematic-composite-indices/gender-inequality-index#/indicies/GII

Kanat, O., Yan, Z., Asghar, M. M., Zaidi, S. A. H., & Sami, A. (2023). Gender Inequality and Poverty: The Role of Financial Development in Mitigating Poverty in Pakistan. Journal of the Knowledge Economy, 15, 11848–11876. https://doi.org/10.1007/s13132-023-01527-y

Kuz, A., & Miskinis, A. (2021). The impact of globalization on European airline market. Ekonomika , 100(1), 117–138. https://doi.org/10.15388/EKON.2021.1.7

Larasati, N. P. A. (2021). Gender Inequality in Indonesia: Facts and Legal Analysis. Law Research Review Quarterly, 7(4), 445–458. https://doi.org/10.15294/lrrq.v7i4.48170

Le Quoc, D. (2024). The relationship between digital financial inclusion, gender inequality, and economic growth: dynamics from financial development. Journal of Business and Socio-Economic Development, 4(4), 370–388. https://doi.org/10.1108/jbsed-12-2023-0101

Miller, R. (2020). Qatar, Energy Security, and Strategic Vision in a Small State. Journal of Arabian Studies, 10(1), 122–138. https://doi.org/10.1080/21534764.2020.1793494

Morsy, H. (2020). Access to finance – Mind the gender gap. Quarterly Review of Economics and Finance, 78, 12–21. https://doi.org/10.1016/j.qref.2020.02.005

Noreen, U. (2024). Mapping of Fintech Ecosystem to Sustainable Development Goals ( SDGs ): Saudi Arabia’s Landscape Mapping of Fintech Ecosystem to Sustainable. Sustainability, 16(21). https://doi.org/10.3390/su16219362

Nurhaliza, S., Hidayat, A., Rohima, S., Pertiwi, R., Andaiyani, S., Shodrokova, X., & Hamidi, I. (2024). The Relationship between Financial Inclusion and Financial Stability Banking Industry in G20 Emerging Market Countries: A Panel Data Evidence. Economic Studies, 33(6), 113–132. https://www.ceeol.com/search/article-detail?id=1251404

Nurunnabi, M. (2017). Transformation from an Oil-based Economy to a Knowledge-based Economy in Saudi Arabia: the Direction of Saudi Vision 2030. Journal of the Knowledge Economy, 8(2), 536–564. https://doi.org/10.1007/s13132-017-0479-8

Ozkaya, A., & Altun, O. (2024). Domestic and Global Causes for Exchange Rate Volatility: Evidence From Turkey. SAGE Open, 14(2), 1–14. https://doi.org/10.1177/21582440241243200

Pasha, H. K. (2024). Gender Differences in Education: Are Girls Neglected in Pakistani Society? Journal of the Knowledge Economy, 15(1), 3466–3511. https://doi.org/10.1007/s13132-023-01222-y

Pati, U. K., Pujiyono, & Pranoto. (2021). Sharia Fintech as a Sharia Compliance Solution in the Optimization of Electronic-Based Mosque’s Ziswaf Management. Padjadjaran Jurnal Ilmu Hukum, 8(1), 47–70. https://doi.org/10.22304/pjih.v8n1.a3

Rovera, C. (2022). Islamic Finance and Microcredit. In Ethics in Banking (pp. 115–136). Springer, Cham.

Rufaidah, F., Karyani, T., Wulandari, E., & Setiawan, I. (2023). A Review of the Implementation of Financial Technology (Fintech) in the Indonesian Agricultural Sector: Issues, Access, and Challenges. International Journal of Financial Studies, 11(3). https://doi.org/10.3390/ijfs11030108

Shah, S., & Ahmad, P. J. (2024). Navigating Challenges: Resilience of Women Entrepreneurs in Khyber Pakhtunkhwa’s Entrepreneurial Ecosystem. CARC Research in Social Sciences, 3(3), 399–407. https://journals.carc.com.pk/index.php/CRISS/article/view/163/108

Soedarmono, W., Trinugroho, I., & Sergi, B. S. (2019). Thresholds in the nexus between financial deepening and firm performance: Evidence from Indonesia. Global Finance Journal, 40(August 2017), 1–12. https://doi.org/10.1016/j.gfj.2018.08.001

Supriatiningsih, E. (2018). The Principal of Risk and Profit Sharing in Islamic Banking. Ijtimā Iyya Journal of Muslim Society Research, 3(2), 262–280. https://doi.org/10.24090/ijtimaiyya.v3i2.1850

Syed, J., & Ali, F. (2019). Theorizing equal opportunity in Muslim majority countries. Gender, Work and Organization, 26(11), 1621–1639. https://doi.org/10.1111/gwao.12416

Syed, J., Ali, F., & Hennekam, S. (2018). Gender equality in employment in Saudi Arabia: a relational perspective. Career Development International, 23(2), 163–177. https://doi.org/10.1108/CDI-07-2017-0126

Topal, A. (2019). Economic reforms and women’s empowerment in Saudi Arabia. Women’s Studies International Forum, 76(July), 102253. https://doi.org/10.1016/j.wsif.2019.102253

Tsouli, D. (2022). Financial Inclusion, Poverty, and Income Inequality: Evidence from European Countries. Ekonomika , 101(1), 37–61. https://doi.org/10.15388/Ekon.2022.101.1.3

World Bank. (2016). Financial development. World Bank. https://www.worldbank.org/en/publication/gfdr/gfdr-2016/background/financial-development

World Bank. (2023). Gender data Malaysia. World Bank. https://genderdata.worldbank.org/en/economies/malaysia

World Economic Forum. (2017). The Global Gender Gap Report. In World Economic Forum. http://www3.weforum.org/docs/WEF_GGGR_2017.pdf%0Ahttps://www.weforum.org/reports/the-global-gender-gap-report-2017

World Health Organization. (2024). Gender Inequality Index (GII). World Health Organization (WHO). https://www.who.int/data/nutrition/nlis/info/gender-inequality-index-(gii)

Younsi, M., & Bechtini, M. (2020). Economic Growth, Financial Development, and Income Inequality in BRICS Countries: Does Kuznets’ Inverted U-Shaped Curve Exist? Journal of the Knowledge Economy, 11(2), 721–742. https://doi.org/10.1007/s13132-018-0569-2

Zweiri, M., & Al Qawasmi, F. (2021). Contemporary Qatar. In Gulf Studies (Vol. 4). https://link.springer.com/10.1007/978-981-16-1391-3