Ekonomika ISSN 1392-1258 eISSN 2424-6166

2025, vol. 104(3), pp. 124–141 DOI: https://doi.org/10.15388/Ekon.2025.104.3.7

Banking Stability under Governance Factors in SEE: Examining Capital Adequacy, Lending Rates, and Governance Quality Using Z-Score

Esat A. Durguti

Faculty of Economics – University Isa Boletini - Mitrovicë, Kosovo

E-mail: esat.durguti@umib.net

ORCID: https://orcid.org/0000-0002-5982-3664

Elvin Meka

Faculty of Business and Law – Tirana Business University College - Tirana, Albania

E-mail: elvin.meka@tbu.edu.al

ORCID: https://orcid.org/0000-0003-3404-7475

Khadijah Idrrisu

Department of Banking and Finance, Islamic University College, Ghana

E-mail: khadijah.iddris@yahoo.com

ORCID: https://orcid.org/0000-0002-1536-2341

Muhamet J. Spahiu*

UNI Universum International College, powered by Arizona State University, Prishtinë, Republic of Kosovo

E-mail: spahiu.m@gmail.com

ORCID: https://orcid.org/0000-0002-5982-3664

Abstract. This study examines banking stability in Southeast Europe by analyzing both financial and institutional factors by using the Z-score as a key metric. On the basis of covering the period of 2012–2023, the research evaluates the impact of capital adequacy, lending rates, non-performing loans, rule of law, regulatory quality, control of corruption, judicial efficiency, and government integrity. The analysis combines static Ordinary Least Squares (OLS) and dynamic Generalized Method of Moments (GMM) methods on panel data. The key findings reveal that capital adequacy, non-performing loans, and regulatory quality positively influence banking stability, thereby suggesting the benefits of strong financial regulation. Conversely, control of corruption and weak government integrity negatively affect stability, highlighting institutional weaknesses. A novel aspect of the study lies in comparing the static and dynamic models: while OLS results show the rule of law as significant and positive and judicial effectiveness as negative, the GMM model finds these institutional variables largely insignificant. This divergence emphasizes the importance of using multidimensional empirical approaches to assess the complex interplay of governance and financial performance in the banking sector. The study ultimately demands strengthened legal and regulatory institutions to enhance banking stability in the region.

Keywords: banking stability, institutional factors, bank-specific factors, panel data.

___________

* Correspondent author.

Received: 13/01/2025. Revised: 18/01/2025. Accepted: 26/05/2025

Copyright © 2025 Esat A. Durguti, Elvin Meka, Khadijah Idrrisu, Muhamet J. Spahiu. Published by Vilnius University Press. This is an Open Access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

1. Introduction

Based on the context of technological progress today, particularly in financial technology (FinTech), which has transformed the entire approach of regulatory authorities and the management of financial institutions, banking stability is highlighted as a catalyst for economic sustainability. One of the key benefits of emerging technologies for economies is FinTech, which facilitates more affordable, faster, and more accessible financial services, particularly through the expansion of digital payment solutions (Kömürcüoğlu and Akyazi, 2024). This is especially important when institutions are facing challenges such as governance issues, concerns about capital adequacy, and fluctuating lending rates (Yitayaw et al., 2022). Additionally, in developed, and especially in emerging countries, numerous studies underline the importance of the banking business not only for economic growth but also for the progress of the financial intermediary (Pham et al., 2021). Hence, this research seeks to scrutinize the level of banking stability in nominated South-East Europe (SEE) economies by employing institutional and banking industry-specific variables conceptualized and proxied by Z-score. The selection of this sample for research is based on several specific characteristics, emphasizing the geographical focus (as the countries are geographically adjacent to one another), followed by the availability of data, the shared specificities in the banking sector, and their current transitional period. Lastly, the selection addresses the research gap identified in previous studies. Grounded in academic and empirical perspectives, the present research seeks to address the existing research gap concerning the examined variables, with a particular focus on the economies under analysis. This research on banking stability distinguishes itself from prior research across multiple dimensions. First, it employs a hybrid econometric approach, integrating methodological rigor with analytical depth. Second, it leverages recent data, thus ensuring a more contemporaneous and relevant assessment of the studied phenomena. Third, it delves into governance factors variables that have been largely underexplored in the context of these economies. These distinctive attributes not only enhance the academic contribution of the present research but also inspire it with a refined dimension of originality within the academic discourse. However, a large number of researchers have noticed that the Z-score from an academic perspective is probably one of the most integrated measures that evaluate banking stability by calculating the possibility of insolvency (Jamileh, 2024; Sodokin et al., 2023; Tarkocin and Donduran, 2023; Pham et al., 2021). Historically, banking stability was evaluated exclusively by financial metrics, referred to as bank-specific indicators. Meanwhile, with the financial crisis of 2007–2008, the need to incorporate institutional and corporate governance metrics has emerged. For the selected economies, addressing these variables in a combined manner will provide additional novelty and added value, both academically and empirically. Hence, identifying the causality of the above-mentioned factors on banking stability in SEE, this research analyzes capital adequacy, lending interest rates, non-performing loans, and the main governance variables, which include the rule of law, regulatory quality, control of corruption, judicial effectiveness, and government integrity. Capital adequacy, as defined by regulatory authorities, the Basel Accord, and European Union directives, is considered one of the key indicators ensuring the stability of banks on the one hand, while, on the other hand, it reflects their ability to withstand losses without facing bankruptcy. As such, Basel III identifies that capital buffers are meant to keep banks running during periods of liquidity constraint and/or financial crises (Spahiu, 2022). Most empirical studies have offered sufficient signals of the direct connection between capital adequacy and an improved stability within the banking division (Deda et al., 2024; Jamileh, 2024; Durguti et al., 2023; Pham et al., 2021).

As highlighted by Huu Vu and Ngo (2023), those banks which meet the regulatory authorities’ criteria for capital reserves are better equipped to handle challenges and significantly reduce the likelihood of bankruptcy. However, from the opposite perspective, banks with low capital reserve levels, as well as those operating near the limits set by regulatory authorities, may face significant difficulties in carrying out daily operations, especially during times of crisis. Under these situations, governance difficulties may compound the situation by generating extra hazards (Essilfie, 2023). Interest rates influence both the profitability of banks and the capability of borrowers to repay loans. The average interest rate in Southeast Europe stands at 6.48%, highlighting variations in conditions across the countries within this region. Banking stability can be influenced by both internal and external factors. For instance, the quality of governance plays a role in affecting banking stability as it influences enforcement, institutional integrity, and risk management (Ozili, 2018). On the contrary, inadequate governance, typified by corruption coupled with weak regulatory environments, can cause low efficiency in bank supervision. According to Ullah et al. (2022), inadequate governance results in increased risk-taking activities and financial instability. Among the countries of SEE, there are several measures of governance, including the rule of law, regulatory quality, control of corruption, judicial effectiveness, and government integrity, which exhibit moderate heterogeneity across countries (World Justice Project, 2023). Therefore, by improving governance frameworks, ensuring adequate capital buffers, and managing lending rates, policymakers in these economies can strengthen banking stability and promote long-term economic growth. Overall, this research presents the key research question: “What influence do governance quality indicators have, and what pressure does their application place on banking stability?” To provide explicit econometric answers to this research question, the study aims to validate it through the proposed hypotheses, which will be tested at a significance level of α = 0.05. The specific hypotheses are:

H1: Capital adequacy has a negative and substantial effect on banking stability.

H2: Lending rates have a substantial effect on banking stability.

H3: Non-performing loans have an adverse and substantial effect on banking stability.

H4: The rule of law has constructive pressure effects on banking stability.

H5: Regulatory quality has a constructive and substantial pressure effect on banking stability.

H6: Control of corruption has an adverse and substantial effect on banking stability.

H7: Government integrity has an adverse and substantial effect on banking stability.

H8: Judicial efficiency substantially affects banking stability.

The current research aspires to contribute in several dimensions. First, it is of value due to contributing to the offering of additional empirical evidence in this field, particularly for the treated economies. Second, it addresses several issues by incorporating a combination of variables that have rarely been examined in SEE economies. Third, it applies the dynamic GMM system approach, which carefully addresses the issues of heterogeneity and endogeneity of the indicators included in the analysis. Lastly, the outcomes provide clear indications of the level and direction of the impact that these variables have on banking stability, which can be used by policymakers so that to take measures to redesign certain policies that may influence the creation of sustainable banking stability.

2. Theoretical Background

In today’s globalized and digital landscape, robust and sophisticated financial systems are crucial for economic development and stability. Transition economies, such as those in the SEE countries, provide distinct perspectives on the influence of creditor rights, government quality, and banking liberalization on bank risk. Fang et al. (2014) presented direct evidence of the causal effects produced by these factors on banking stability through an examination of transition economies. Empirical research indicates that banks with elevated capital levels typically appear more stable, thus reinforcing the moral hazard hypothesis. Additionally, the study indicates that institutional quality is extremely important for financial stability. Hoang et al. (2024) assert that capital adequacy and institutional quality can jointly improve banking stability. The interaction becomes especially evident in banking systems with minimized capital levels, wherein robust institutional frameworks may make amends for inadequate capital buffers. Considering the backdrop of capital structure for Western Balkan countries, Ahmeti et al. (2023), by employing a balanced panel dataset for forty-seven commercial banks and adopting a fixed effects regression approach, revealed a significant beneficial connection between profitability and the capital structure. Malik et al. (2022) offered concrete evidence demonstrating that components of the governance environment, namely, the rule of law, regulatory quality, and control of corruption are essential for ensuring banking stability and the whole monetary system. Deda et al. (2024) analyzed the economies of Southeastern Europe, emphasizing that the same drivers exert statistically significant adverse consequences on banking stability, while government efficiency demonstrates an insignificant statistical influence. Angelini et al. (2020) ended up arriving at identical conclusions, emphasizing the favorable implications of services provided by governments. Cieslik and Goczek (2018) discovered that an inadequate level of judicial effectiveness and government integrity encourages heightened corruption levels, adversely impacting banking stability. Ullah et al. (2022) assert that economies with a robust regulatory structure and effective enforcement can withstand financial crises and preserve banking stability.

The soundness of the banking system has become critical for economic stability and sustained growth; discovering the contributing factors of non-performing loans (NPLs) is essential for banks, banking regulators, and governments so that to implement efficient prevention strategies against banking and economic instability (Giammancoet et al., 2023). In this background, Kuzucu and Kuzucu (2019) stressed that financial institutions, mainly banks with long-term strategic goals, need to handle and preserve NPLs within the set minimal criteria. In this mindset, Abiad and Mody (2005) expressly shed light on the negative and considerable influence of government stability on NPLs when an exact threshold level has been achieved. Guidi (2021), in analyzing the SEE countries, has highlighted that these institutions serve as the primary channel through which financial resources are allocated and distributed across the region. Moreover, in recent times, they have undergone radical transformations in the context of privatization, consolidation, and cross-border acquisitions. The findings of this study underscore that banking stability is at risk in cases of increasing non-performing loans and intense market competition. Conversely, a high degree of market concentration in this sector contributes to a reduction in non-performing loans. Conversely, if the non-performing loan ratio is below the set level, the effect is considered insignificant. The inability of banking institutions to effectively obtain deposits from a broad spectrum of people hinders the possibilities for capital accumulation and restricts the capability banks to distribute loans, which is necessary for economic growth (Olawale, 2024). For instance, Martinez and Repullo (2020) in their research consider an economy where intermediaries have market power in granting loans, intermediaries monitor borrowers, which lowers their probability of default, and monitoring is costly and unobservable, which creates a moral hazard problem with uninsured depositors. Nevertheless, when it comes to interest rate policies and their effectiveness in preventing financial crises, there remains some uncertainty. Demcenko (2021), through an in-depth analysis of portfolio diversification in an international context, examined various financial instruments. The findings of this research provide evidence that optimization aimed at minimizing the level of risk results in a significant reduction in returns. The connection between credit conditions, financial crises, and interest rate policies is still debated, and these are the variables that most strongly influence results in this area (Ajello et al., 2016).

The connection they share cuts the percentage of loans compared to deposits across these two directions. The financial stability policy, which requires monitoring mechanisms, is based mainly on straightforward metrics of a narrative nature that are far from perfect, and the difficulty of evaluating financial intermediation comprehensively. As stated by Jordà et al. (2017), there are opinions that macroprudential policy should be fostered around the loan-to-deposits criterion, and there is a corresponding indication that the loan-to-deposits is an appropriate metric of financial fragility. Nonetheless, this evidence also suggests that it fails to be an early warning sign, which leaves regulators with the task of reviewing the loan-to-deposit ratio for a given moment. To enhance the credibility of this argument, Boďa and Zimková (2021) underline that loan-to-deposits is merely a descriptive measure, and that it lacks a conventional direction.

The performance of national institutions is unrelated to these economic variables, and thus the possibility of erroneous predictor variables is removed. The demonstrated association between administrative improvements and bank risk-taking does not appear to be explained by exogenous variables. The research conducted by Abbas et al. (2022) underlines that financial stability can be defined by its various qualities, such as “improving economic procedures, managing risks, and absorbing shocks”. Liashenko et al. (2023), through an advanced and challenging study, examined the application of various machine learning algorithms for the task of predicting corporate bankruptcy based on financial indicators. Specifically, they found that bagging and random forest, combined with Near-Miss and random under-sampling techniques, yielded the best results in identifying bankrupt companies in small samples, whereas artificial neural networks provided the most consistent outcomes with larger samples.

Additionally, several researchers (Gallas et al., 2024; Abbas et al., 2022) argue that financial stability and economic growth reinforce each other. Countries undergoing an economic downturn, especially suffered from an impact on banking operations and business activity. For these countries, it has become challenging to attract foreign financing, which affects GDP growth and crediting. In their analysis of the financial landscape of the eleven SEE economies, Zhuja et al. (2024), by employing a mixed econometric approach, examined the financial stability index and its interrelationship with the banking stability index, as well as several macroeconomic determinants. Their findings suggest that the strengthening of banking stability contributes to the establishment of predispositions for a stable economy, while inflation is identified as an additional risk factor for these economies. Consequently, considering this scenario, Iljaz et al. (2020) stress that it is fairly evident that economic expansion enhances financial stability. The monetary and banking industries are described as being sound when lending bodies are capable of supplying financing to families in an adequate amount, and turmoil in the economy, under both internal and external shocks, is unable to render them unstable (Idawati and Syafputri, 2022). The insufficient capacity of the banking system to withstand events, as well as external and internal shocks, can lead to an overall decrease in lending; consequently, business activity will slow down, unemployment is expected to rise, and, ultimately, economic growth will decrease.

3. Research Method

The methodology designed to empirically evaluate the influence of specific variables from the banking industry and institutional variables begins with the study data sample, the valuation and selection of variables, and, finally, the determination and justification of the applied econometric approach.

3.1. Study sample

This study constitutes a conceptual and empirical scrutiny of an interplay of bank-specific and institutional variables on banking stability, by employing a strongly balanced sample comprising six Southeast European countries from 2012 to 2023. The data were obtained from two credible organizations (the World Bank and the Heritage Foundation) and are provided annually, encompassing 72 observations. Each banking industry’s variables are expressed as a percentage, whereas institutional variables are assessed based on the World Bank’s methodology. Additionally, the variables of judicial effectiveness and government integrity are assessed following the methodological algorithm of the Heritage Foundation.

3.2. Measurements and selection of variables

The construction of this econometric paradigm is to evaluate combined determinants (both financial and institutional) in banking stability within SEE economies. The illustration of the determinants in the tabular form provides a comprehensive overview, starting from their description and role in the research, expected sign, explanation of the respective variable, method of calculation (estimation), and the source of the exploited data. Additionally, each calculation or evaluation technique that influenced the selection of various variables within the context of the performed approach will be displayed in the tabular format.

Table 1. A comprehensive summary of the variables

|

Variable and label

|

Explanation

|

Calculation

|

Source

|

Exp. sign

|

|

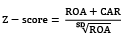

Bank stability (BS)

|

It evaluates the probability of a bank’s failure within the system by assessing returns alongside capital and dividing them by the square root of returns on assets.

|

|

World Bank:

https://databank.

worldbank.org/

|

|

|

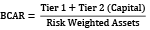

Bank Capital Adequacy Ratio (BCAR)

|

This indicator reflects the ability of the banking system to withstand potential unexpected losses to protect depositors and ensure financial stability.

|

|

WB

|

+/-

|

|

Lending Interest Rate (LIR)

|

This indicator represents the rate applied by the banking system of the countries included in the analysis to support individuals or businesses.

|

Expressed in nominal annual terms

|

WB

|

-

|

|

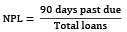

Non-Performing Loans (NPL)

|

It indicates the % of loans that are overdue by more than 90 days from borrowers, failing to adhere to the terms specified in the agreement.

|

|

WB

|

+/-

|

|

Rule of Law (RL)

|

It indicates the level of adherence to the RL, evaluated according to the World Bank’s methodology.

|

The rating is -2.5 for very poor performance, while 2.5 represents high performance.

|

WB

|

+

|

|

Regulatory Quality (RQ)

|

It indicates the quality and implementation of the legal framework, evaluated according to the WB methodology.

|

The rating is -2.5 for very poor performance, while 2.5 represents high performance.

|

WB

|

+

|

|

Control of Corruption (CC)

|

It indicates the capacity of institutional governance in CC, evaluated according to the WB methodology.

|

The rating is -2.5 for very poor performance, while 2.5 represents high performance.

|

WB

|

-

|

|

Judicial Effectiveness (JE)

|

It reflects the judicial system’s ability to enforce and implement laws efficiently and fairly.

|

The rating scale is 0 for very poor effectiveness, and 100 represents high performance.

|

The Heritage Foundation

|

+/-

|

|

Government Integrity (GI)

|

This component evaluates transparency, the fight against corruption, and the government’s ability to ensure that public resources are utilized fairly and efficiently.

|

The rating scale is 0 for very poor GI, whereas 100 represents high GI.

|

The Heritage Foundation

|

+/-

|

Source: compiled by the authors

3.3. Data analysis approach

The development of the dynamic approach is entirely interconnected with the characteristics of the data, which, in our explicit instance, involves the evaluation of banking stability through financial and institutional causes of a dynamic nature. Therefore, the utilization of the panel data contained within the study reflects dynamic features, as their current behavior undoubtedly reflects past performance. Consequently, the employment of a dynamic panel model is necessary. In the econometric context, the dynamic nature of the model limits the use of static approaches, such as Ordinary Least Squares (OLS), which, in our instance, could lead to biased conclusions due to the association between unobserved effects and the lagged dependent variable (Hasanovic and Latic, 2017). Hence, fixed-effects or random-effects for panel data cannot always resolve significant econometric issues compared to dynamic models. While addressing these shortcomings, Arellano and Bond (1991) introduced an estimator known as the Generalized Method of Moments (GMM) system to address endogeneity problems. This estimator is particularly relevant for mitigating bias and heterogeneity observed across countries, which traditional methods may fail to capture accurately. As part of their background, Arellano and Bond (1991) emphasized the necessity of incorporating additional instruments to estimate dynamic panels and proposed various transformations. Subsequently, Arellano and Bover (1995), and also Blundell and Bond (1998) further enhanced the estimator by suggesting additional constraints in the initial stages, allowing for the inclusion of more instruments to improve results. These advancements also enabled the combination of the first difference of variables. This study employs a minimal number of instrumental variables to minimize bias and address issues of endogeneity and autocorrelation. The application of this econometric approach is further inspired by the empirical analysis of Klinac (2023), and Ercegovac et al. (2024), whose econometric specification is as follows:

where: BS denotes the dependent variable, φ represents the intercept slope, β₁ – β₈ are the intercepts of the independent variables, t indicates time (2012–2023), i denotes specific effects within the analysis, πi denotes unobserved effects in the estimation, and εit signifies the latent error in the simulated method.

4. Results and Insights

4.1. Descriptive statistics

Table 2 offers a comprehensive outline of the distribution and variation of the determinants examined in this research. The research sample in our specific instance includes 72 observations for each variable, covering key valuations such as the mean, standard deviation (SD), and minimum and maximum values.

Based on the initial valuation, it is observed that banking stability has a mean value of 13.12 with an SD of 5.62 percent, reflecting moderate variation between its lowest and highest values, ranging from 4.45 to 24.29. Therefore, considering this conclusion and the assumptions based on the Z-score, it can be inferred that the economies analyzed are in the green zone (as their mean value is ≥ 3.00). The capital adequacy is observed to have a mean value of 9.32 with an SD of 1.3 percent. Additionally, the variation between its minimum value of 7.26 and the maximum value of 12.00 indicates that these economies are nearly meeting the requirements set by regulatory authorities. The lending interest rate applied by these countries has a mean value of 6.49 percent, with significant variations ranging from 3.07 to 12.67 percent.

Table 2. Descriptive statistics

|

Obs

|

Mean

|

SD

|

Min

|

Max

|

|

BS

|

72

|

13.124

|

5.623

|

4.453

|

24.290

|

|

BCAR

|

72

|

9.320

|

1.275

|

7.259

|

12.001

|

|

LIR

|

72

|

6.487

|

1.976

|

3.071

|

12.665

|

|

NPLs

|

72

|

9.138

|

5.950

|

1.932

|

22.243

|

|

RL

|

72

|

-0.227

|

0.144

|

-0.542

|

0.024

|

|

RQ

|

72

|

0.106

|

0.241

|

-0.374

|

0.524

|

|

CC

|

72

|

-0.374

|

0.203

|

-0.780

|

0.010

|

|

JE

|

72

|

42.785

|

10.156

|

20.151

|

61.400

|

|

GI

|

72

|

39.775

|

5.311

|

28.401

|

52.000

|

Source: calculations by the authors

Another critical determining factor of banking stability is the non-performing loans, which have a mean value of 9.14 percent with an SD of 5.95 percent. In the background of institutional determinants considered pressures on banking stability conception, specifically, the rule of law and regulatory quality, they exhibit mean values of -0.227 and 0.106, respectively, indicating weak performance of these indicators. Moreover, reflecting these two determinants, control of corruption has a mean value of -0.374, demonstrating limited commitment from the leadership structures of these states, and necessitating further effort and dedication to achieve satisfactory outcomes in this area. Finally, the two interrelated components, judicial effectiveness and government integrity, have mean values of 42.78 and 39.78, respectively. These outcomes, on a scale ranging from 0 to 100, provide initial indications that these states are still struggling with the inadequate functioning of judicial effectiveness, and that government integrity remains below a satisfactory level.

4.2. Correlation analysis

The research effort aimed to examine the interaction between banking stability and several independent variables through a correlation analysis. Our results confirm that banking stability has a positive correlation with non-performing loans and regulatory quality; nevertheless, it has a negative correlation with all other variables.

From the outcomes presented in Table 3, it can be observed that none of the coefficients exceed the value of 0.75. To further alleviate any uncertainties, we additionally offered a Variance Inflation Factor (VIF) breakdown. Our initial conclusion that the data employed for the examination does not display such issues is validated by the findings of this analysis, as stated in the preceding paragraph. The premise is supported by the evidence presented by Wooldridge (2012), emphasizing that none of the individual variables should exceed the threshold value of 5 (≥ 5). In our instance, the largest observed value is 2.84.

Table 3. Correlation matrix

|

BS

|

BCAR

|

LIR

|

NPLs

|

RL

|

RQ

|

CC

|

JE

|

GI

|

VIF

|

|

BS

|

1.000

|

|

|

|

|

|

|

|

|

|

|

BCAR

|

-0.236

|

1.000

|

|

|

|

|

|

|

|

1.30

|

|

LIR

|

-0.122

|

-0.112

|

1.000

|

|

|

|

|

|

|

1.66

|

|

NPLs

|

0.484

|

-0.371

|

0.290

|

1.000

|

|

|

|

|

|

2.14

|

|

RL

|

-0.113

|

-0.160

|

-0.287

|

0.050

|

1.000

|

|

|

|

|

2.84

|

|

RQ

|

0.128

|

-0.179

|

0.094

|

0.099

|

0.385

|

1.000

|

|

|

|

1.42

|

|

CC

|

-0.503

|

0.023

|

0.068

|

0.045

|

0.672

|

0.432

|

1.000

|

|

|

2.73

|

|

JE

|

-0.411

|

0.129

|

0.135

|

-0.508

|

0.063

|

0.146

|

0.160

|

1.000

|

|

2.01

|

|

GI

|

-0.589

|

0.150

|

0.103

|

-0.472

|

0.067

|

0.284

|

0.332

|

0.624

|

1.000

|

2.24

|

Source: calculations by the authors

4.3. Unit root and cointegration test

To compose a continuous chronology of justification employing the previously elaborated examinations, we additionally performed a unit root analysis, namely, the Levin-Lin-Chu test, to verify whether the data were stationary. The proposed approach relies on the null hypothesis, which presumes that the data are non-stationary. Through this research, it was determined that every single variable exhibits stationarity at the level, thereby verifying the alternative hypothesis. The rationale for performing this analysis lies in the fact that, if the data are not stationary, the model’s results may lead to generating inaccurate outcomes (Levendis, 2023). To evaluate whether the variables are cointegrated, the Pedroni test was applied. In our instance, the test yielded a coefficient of ß = 4.5313, with a probability (ρ = 0.000), providing robust evidence that the variables are well-integrated within the panel outline.

Table 4. Levin-Lin-Chu and cointegration test

|

Variables

|

At level

|

|

Statistic

|

ρ-value

|

|

BS

|

-7.7573

|

0.0000

|

|

BCAR

|

-3.5579

|

0.0002

|

|

LIR

|

-4.8819

|

0.0000

|

|

NPLs

|

-6.0167

|

0.0000

|

|

RL

|

-13.0079

|

0.0000

|

|

RQ

|

-5.7385

|

0.0000

|

|

CC

|

-3.1224

|

0.0009

|

|

JE

|

-5.0024

|

0.0000

|

|

GI

|

-6.8471

|

0.0000

|

|

Pedroni test

|

4.5313

|

0.0000

|

Source: calculations by the authors

4.4. Model fitting

The outcomes of the analysis of the applied models in the economies of Southeastern Europe (SEE) are presented in Table 5, even though the standard tests for these models, including R², F-test, Wald, Sargan, and Arellano-Bond (AR1 and AR2), were employed to validate the robustness of the results (see the second part of Table 5). In this section, a brief elaboration will be provided on some of the diagnostic tests (see the last part of Table 5) that are essential before discussing the econometric results of the models. Firstly, in terms of R2 based on the OLS approach, it is observed that the applied variables explain 63% of banking stability, as indicated by the probability value of the F-test. Meanwhile, for the dynamic GMM approach, the Wald test was performed, yielding a p-value (ρ=0.000), which demonstrates high model stability and adequacy. To further reinforce the argument, the Sargan test was conducted to assess the validity of the instruments used in the model and to eliminate potential endogeneity concerns.

Table 5. Empirical results of research

|

OLS approach

|

Arellano-Bover/Blundell-Bond approach

|

Arellano-Bover/Blundell-Bond approach robust

|

|

β

|

ρ ≥ [z]

|

β

|

ρ ≥ [z]

|

β

|

ρ ≥ [z]

|

|

BSL1.

|

“-“

|

“-“

|

0.5171

|

0.000

|

0.5172

|

0.000

|

|

BCAR

|

0.2448

|

0.052

|

-0.2506

|

0.005

|

-0.2506

|

0.012

|

|

LIR

|

-0.1254

|

0.514

|

-0.6371

|

0.000

|

-0.6371

|

0.002

|

|

NPLs

|

0.2341

|

0.002

|

0.1762

|

0.000

|

0.1762

|

0.029

|

|

RL

|

9.4913

|

0.007

|

-1.6968

|

0.414

|

-1.6968

|

0.411

|

|

RQ

|

10.4273

|

0.000

|

5.0057

|

0.003

|

5.0057

|

0.020

|

|

CC

|

-21.1299

|

0.000

|

-7.9207

|

0.000

|

-7.9207

|

0.049

|

|

JE

|

-0.1962

|

0.000

|

-0.0149

|

0.460

|

-0.0149

|

0.400

|

|

GI

|

-0.1532

|

0.068

|

-0.0821

|

0.040

|

-0.0821

|

0.015

|

|

_cons

|

17.1499

|

0.000

|

11.0704

|

0.000

|

0.5172

|

0.000

|

|

Observation

|

72

|

|

72

|

|

72

|

|

|

ꭓ2-test

|

5.541

|

0.0186

|

|

|

|

|

|

R2

|

0.6293

|

|

|

|

|

|

|

F-test

|

38.26

|

0.0000

|

|

|

|

|

|

Wald chi2

|

|

|

381.5700

|

0.000

|

64.3500

|

0.0000

|

|

Sargan test

|

|

|

64.0881

|

0.1637

|

64.0881

|

0.1637

|

|

AR1

|

|

|

|

|

-1.9452

|

0.0518

|

|

AR2

|

|

|

|

|

-0.5308

|

0.5956

|

Source: calculations by the authors

Finally, moving beyond a standard analysis, we applied a robust model within the dynamic approach to evaluate whether there are any significant changes on the one hand, and to eliminate concerns regarding autocorrelation and endogeneity on the other hand. The results presented in Table 5, in the rightmost column, indicate no significant differences. The Arellano-Bond test results indicate that the model’s outcomes do not exhibit important issues, as evidenced by AR1, which has a value of (ρ = 0.0518), suggesting a mild autocorrelation, commonly observed when dealing with panel data. Meanwhile, AR2, with a value of (ρ = 0.5956), which is insignificant in the second order, clearly indicates that there are no concerns regarding autocorrelation or issues of endogeneity.

In analyzing the results of the presented empirical approaches, it is observed within the econometric mindset that there are several distinctions between the applied approaches, such as capital adequacy and the rule of law. The findings highlight that OLS in panel data settings is assumed to be incapable of correcting issues related to endogeneity. Consequently, a more sophisticated GMM approach has been applied, addressing these concerns. Within this context, the focus of the discussion on the econometric findings will be centered around the GMM approach. The discoveries of the dynamic model indicate that the majority of the variables analyzed have a statistically significant effect. The maintenance of capital reserves, as required by international regulatory contexts and the ongoing pressures exerted by national authorities to ensure compliance, has been found to have an important harmful effect on banking stability at a confidence level of 0.01. This research outcome validates H1, aligns with the expected assumptions, and is consistent with analogous studies (Hoang et al., 2024; Pham et al., 2021), which emphasized that banks with higher capital reserves tend to be more stable, whereas the association among them demonstrates an important harmful effect. It is also noteworthy that our findings oppose the results of Yitayaw et al. (2022), who argued for a constructive association between these variables. An equivalently robust statistical effect was discovered for the lending interest rate, validating H2, which corresponds with the expected assumptions. This research offers comprehensive evidence that the financial burden imposed by high interest rates directly undermines banking stability. At first glance, from the perspective of securing income from interest, this may appear to be an interesting outcome. However, when analyzed through the lens of the inability to meet contractual obligations, the rise in non-performing loans, and the risk of losing accrued interest, the profits of financial institutions are directly diminished. Furthermore, as a result of the deterioration in economic conditions, high interest rates contribute to a slowdown in economic growth, thereby exposing institutions to the risk of capital loss. Our findings are comparable to those of Durguti et al. (2023), who additionally claim that high interest rates undermine banking stability and lead to new possibilities for money laundering. Additionally, Ajello et al. (2016) stressed that a failure to adopt an appropriate interest rate policy could lead to credit-related crises.

The mathematical model additionally implies that lending activity and asset quality management, guided by sound practices, have a beneficial interplay with banking stability, thereby underlining that the banking industry with an adequate loan portfolio translates into greater banking stability. The conclusions of this examination reject hypothesis H3 and affirm the validity of the alternative hypothesis. Our results correspond with the conclusions of Kuzucu and Kuzucu (2019), who recommend that banks following a long-term strategy to preserve non-performing loans at the required minimum level indicate a beneficial interplay with banking stability; however, the opposite effect happens as well. From the perspective of institutional determining factors, the rule of law and judicial effectiveness have demonstrated statistically insignificant effects based on the generated results, and, as such, they do not support H4 and H8. Moreover, the regulatory quality, determined by its coefficient value ß = 5.005 with ρ = 0.003, demonstrates a significantly beneficial effect on banking stability at a 0.01 statistical reliability level. The results obtained mean that a mean increase in the regulatory quality leads to a 5.005-unit enhancement of banking stability, considering the ceteris paribus assumption. The result, presented in Table 5, confirms H5 and the expected assumptions. Moreover, it corroborates assertions regarding the rule of law and judicial effectiveness, highlighting a lack of strong commitment to the rigorous implementation of the current regulatory framework. Our discoveries correspond with those of Deda et al. (2024), who studied Southeast European (SEE) countries and found that the regulatory quality significantly impacts banking stability. Additionally, Malik et al. (2022) offered scientific evidence emphasizing that institutional governance features are essential for banking stability.

Anyway, the inadequate efficiency of the rule of law presents the potential for corrupt actions among interest groups. In this context, control of corruption demonstrates a significantly harmful effect on banking stability, with a high level of statistical confidence. The discoveries indicate that each one-unit increase in control of corruption corresponds to a direct reduction of 7.920 units in banking stability, under the ceteris paribus principle, thereby confirming H6. These observations line up with those published by other researchers, for example, Deda et al. (2024), Ullah et al. (2022), Malik et al. (2022), and Angelini et al. (2020), who additionally claim that control of corruption negatively influences banking stability. Lastly, government integrity likewise demonstrates its adverse influence on banking stability, since it has a statistically significant effect at a 0.05 probability level. This result additionally confirms H7, while demonstrating that every unit getting worse in government integrity is associated with a 0.08-unit reduction in banking stability. These results provide unambiguous signs that the economies covered in this analysis have serious concerns regarding their integrity. The conclusions of this examination stand in full conjunction with the research undertaken by Sadokin et al. (2023), who predict that institutional components are adversely connected with banking stability. Similarly, Angelini et al. (2020) underline that the effective, transparent, and fair implementation of the rules and regulations enhances banking stability; on the contrary, it substantially affects banking stability.

5. Conclusion

The research has explored the determinants of banking stability in Southeastern Europe, covering the period from 2012 to 2023 through a combined approach, employing both static and dynamic methods, specifically, while using the GMM estimator. The use of the Z-score to measure banking stability provided detailed insights into how governance characteristics such as the rule of law, regulatory quality, control of corruption, judicial effectiveness, and government integrity interact with bank-specific factors like capital adequacy, non-performing loans, and lending interest rates to influence banking stability. Moreover, the dynamic approach model results showed significant evidence of a relationship between banking stability and the internal and external factors considered in this research. Based on the research findings, it is concluded and econometrically verified that the favorable impact of the regulatory quality on banking stability suggests that strong and effective regulations are essential for ensuring the stability of the financial sector. This implies that regulations must be not only well-crafted but also properly administered and adhered to. Specifically, regulatory quality acts as a robust mechanism that pressures implementing actors to adopt best practices, thereby influencing the maintenance of an adequate quality of non-performing loans. In the specific instance under analysis, the research underscores that the level of NPLs remains within satisfactory norms and has a constructive impression on the creation of banking stability in these countries during the observed period. Another noteworthy, though somewhat surprising, discovery pertains to the rule of law and judicial effectiveness, which were found to be insignificant in contributing to banking stability.

Low government integrity has a detrimental effect on banking stability, which is particularly concerning. These findings underscore the negative effect of insufficient governance on the financial sector’s health and highlight the importance of transparent and accountable governance systems. Corruption and a lack of integrity have a particularly damaging effect on banking stability. These results emphasize the undesirable effects of poor governance and corruption on the financial sector’s health, underscoring the importance of open and accountable governance methods. When institutions are transparent and accountable, banks can thrive. Conversely, control of corruption and an ineffective judicial system inflict harm not only on the banking system but also on the broader economy. Strengthening the rule of law and governance frameworks in the region will lead to a stronger, more stable banking system, which, in turn, will attract greater investments and foster a positive environment for growth.

Certainly, the research may have certain limitations: first, a relatively short time frame was considered; second, the study’s focus was on combining static and dynamic approaches in the short term. However, these aspects should not be viewed as shortcomings of the research or as deviations from its findings. For future studies, it is recommended to include a longer time frame and employ dynamic approaches capable of capturing long-term effects.

Policy Implications

The banking sector in SEE is decisive to regional economic stability and well-being, yet it is facing governance challenges and high lending standards. Governments must collaborate closely with banks to design, evaluate, and implement policies that would benefit both the banking industry and the overall economic development. The current study emphasizes that, with governmental intervention (e.g., strengthening the governance factors), banking stability can be significantly improved. Additionally, even though this research provides important policy implications by identifying variables that enhance BS and contribute to bridging the evident academic and empirical gap for these economies, it is crucial to further detail the factors influencing banking stability and to conduct specific policy interventions which would be well-structured and implemented over time and across regions.

Author Contributions

Esat A. Durguti: conceptualization, methodology, formal analysis, data curation, writing – original draft, visualization.

Elvin Meka: conceptualization, supervision, validation, writing, review and editing, resources.

Khadijah Idrrisu: investigation, data curation, writing – original draft, writing – review and editing.

Muhamet J. Spahiu: methodology, software, formal analysis, writing, review and editing, project administration.

References

Abbas, U., Ullah, H., Ali, R. I., Hussain, S.H., and Ashraf, M. W. (2022). The Impact of GDP Growth on the Financial Stability of the Banking Sector of Pakistan. Journal of Tianjin University Science and Technology, 55(2), 192-213. https://doi.org/10.17605/OSF.IO/39XAZ.

Abiad, A., and Mody, A. (2005). Financial reform: What shakes it? What shapes it? American Economic Review, 95(1), 66-88. https://doi.org/10.1257/0002828053828699.

Ahmeti, Y., Kalimashi, A., Ahmeti, A., & Ahmeti, S. (2023). The Capital Structure Determinants on Banking Sector of Western Balkan Countries. Ekonomika, 102(1), 102–121. https://doi.org/10.15388/Ekon.2023.102.1.6.

Ajello, A., Laubach, Th., Lopez-Salido, D., and Nakata, T. (2016). Financial Stability and Optimal Interest-Rate Policy. FEDS Working Paper No. 2016-67, http://dx.doi.org/10.17016/FEDS.2016.067.

Angelini, F., Candela, G. & Castellani, M. (2020). Governance efficiency with and without government. Social Choice and Welfare, 54, 183–200. https://doi.org/10.1007/s00355-019-01217-2.

Arellano, M., & Bond, S. (1991). Some Tests of Specification for Panel Data: Monte Carlo Evidence and Application to Employment Equations. The Review of Economic Studies, 58, 277–297.

Arellano, M., & Bover, O. (1995). Another Look at the Instrumental Variables Estimation of the Error Component Models. Journal of Econometrics, 68, 29–51.

Blundell, R., & Bond, S. (1998). Initial Conditions and Moment Restrictions in Dynamic Panel Data Models. Journal of Econometrics, 87, 115–143. Available at http://cemmap.ifs.org.uk/wps0209.pdf.

Boďa, M., and Zimková, E. (2021). Overcoming the loan-to-deposit ratio by a financial intermediation measure - A perspective instrument of financial stability policy. Journal of Policy Modeling, 43(5), 1051-1069. https://doi.org/10.1016/j.jpolmod.2021.03.012.

Cieślik, A., and Goczek, Ł. (2018). Control of corruption, international investment, and economic growth – Evidence from panel data. World Development. 103, 323-335. https://doi.org/10.1016/j.worlddev.2017.10.028.

Deda, G., Mehmeti, I., Tërstena, A., and Bislimi, F. (2024). Steering stability: Governance determinants and the banking business insight from Southeastern European countries. Multidisciplinary Science Journal, 7(5), 2025254. https://doi.org/10.31893/multiscience.2025254.

Demcenko, D. (2021). Word Portfolio Optimization in the Environment of Zero Interest Rate. Ekonomika, 100(1), 156-174. https://doi.org/10.15388/Ekon.2021.1.9.

Durguti, E., Arifi, E., Gashi, E., and Spahiu, M. (2023). Anti-money laundering regulations’ effectiveness in ensuring banking sector stability: Evidence from the Western Balkans. Cogent Economics & Finance, 11(1). https://doi.org/10.1080/23322039.2023.2167356.

Ercegovac, R., Klinac, I. & Pečarić, M. (2024). The Non-Sensitivity of Public Development Banks to Key Stability Performance of the Banking Sector: The Lessons for Policymakers. Croatian Economic Survey, 26 (1), 37-58. https://doi.org/10.15179/ces.26.1.2.

Essilfie, R. M. (2023). Corporate social responsibility, corporate governance, and financial performance of banks in Ghana. University of Cape Coast Institutional Respiratory. Department of Accounting and Finance. http://hdl.handle.net/123456789/11087.

Fang, Y., Hasan, I., and Marton, K. (2014). Institutional development and bank stability: Evidence from transition countries, Journal of Banking & Finance. 39, 160-176. https://doi.org/10.1016/j.jbankfin.2013.11.003.

Gallas, S., Bouzgarrou, H., and Zayati, M. (2024). Balancing financial stability and economic growth: a comprehensive analysis of macroprudential regulation. Eurasian Economic Review, 14, 1005–1033. https://doi.org/10.1007/s40822-024-00283-x.

Giammanco, M. D., Gitto, L., and Ofria, F. (2023). Government failures and non-performing loans in Asian countries. Journal of Economic Studies, 50(6), 1158-1170. https://doi.org/10.1108/JES-06-2022-0348.

Guidi, F. (2021). Concentration, competition, and financial stability in the South-East Europe banking context. International Review of Economics & Finance. 76, 639-670. https://doi.org/10.1016/j.iref.2021.07.005.

Hasanovic, E., and Latic, T. (2017). The Determinants of Excess Liquidity in the Banking Sector of Bosnia and Herzegovina. IHEID Working Papers 11-2017. Economics Section. The Graduate Institute of International Studies.

Hoang, K., Tran, S., Nguyen, D., and Nguyen, L. (2024). Bank capital, institutional quality, and bank stability: International evidence. International Journal of Revenue Management, 14(1), 33–53. https://doi.org/10.1504/IJRM.2024.135965.

Huu Vu, T., & Thanh Ngo, T. (2023). Bank capital and bank stability: The mediating role of liquidity creation and the moderating role of asset diversification. Cogent Business & Management, 10(2). https://doi.org/10.1080/23311975.2023.2208425.

Idawati, W., & Syafputri, S. A. (2022). The Effect of Digital Financial, Credit Risk, Overhead Cost, and Non-Interest Income on Bank Stability. Inquisitive: International Journal of Economics, 3(1), 23-44. https://doi.org/10.35814/inquisitive.v3i1.4227.

Ijaz, S., Hassan, A., Tarazi, A., & Fraz, A. (2020). Linking bank competition, financial stability, and economic growth. Journal of Business Economics and Management, 21(1), 200-221. https://doi.org/10.3846/jbem.2020.11761.

Jamileh Ali Mustafa (2024). From innovation to stability: Evaluating the ripple influence of digital payment systems and capital adequacy ratio on a bank’s Z-score. Banks and Bank Systems, 19(3), 67-79. https://doi.org/10.21511/bbs.19(3).2024.07.

Jordà, Ò., Richter, B., Schularick, M., and Taylor, A. M. (2017). Bank capital redux: Solvency, liquidity, and crisis. The Review of Economic Studies, 88(1), 260-286. https://doi.org/10.3386/w23287.

Klinac, I. (2023). Komparativna analiza determinanti poslovanja javnih i poslovnih banaka Europske unije nakon globalne financijske krize. ET²eR – ekonomija, turizam, telekomunikacije i računarstvo, V (1), 1-13. Retrieved from https://hrcak.srce.hr/295089.

Kömürcüoğlu, Ömer F., & Akyazi, H. (2024). Novel Analysis on the Impact of FinTech Developments for Monetary Policy: The Case of Türkiye. Ekonomika, 103(3), 70–90. https://doi.org/10.15388/Ekon.2024.103.3.5.

Kuzucu, N., and Kuzucu, S. (2019). What Drives Non-Performing Loans? Evidence from Emerging and Advanced Economies during Pre- and Post-Global Financial Crisis. Emerging Markets Finance and Trade, 55(8), 1694–1708. https://doi.org/10.1080/1540496X.2018.1547877.

Levendis, J.D. (2023). Unit Root Tests. Time Series Econometrics. Springer Texts in Business and Economics. Springer, Cham. https://doi.org/10.1007/978-3-031-37310-7_7.

Liashenko, O., Kravets, T., & Kostovetskyi, Y. (2023). Machine Learning and Data Balancing Methods for Bankruptcy Prediction. Ekonomika, 102(2), 28-46. https://doi.org/10.15388/Ekon.2023.102.2.2.

Malik, A.H., Mohamed bin Jais, A.H., and Mubashir A. K. (2022). Financial stability of Asian Nations: Governance quality and financial inclusion. Borsa Istanbul Review. 22 (2), 377-387. https://doi.org/10.1016/j.bir.2021.05.005.

Martinez Miera, D., and Repullo, R. (2020). Interest rates, market power, and financial stability. CEPR Discussion Paper No. DP15063, https://ssrn.com/abstract=3661406.

Olawale, A. (2024). Capital adequacy and financial stability: A study of Nigerian banks’ resilience in a volatile economy. GSC Advanced Research and Reviews, 21(1), 001-012. https://doi.org/10.30574/gscarr.2024.21.1.0346.

Ozili, Peterson, K. (2018). Banking stability determinants in Africa. International Journal of Managerial Finance, 14(4), 462-483. https://doi.org/10.1108/IJMF01-2018-0007.

Pham, T. T., Dao, L. K. O., and Nguyen, V. C. (2021). The determinants of banks’ stability: a system GMM panel analysis. Cogent Business & Management, 8(1). https://doi.org/10.1080/23311975.2021.1963390.

Sodokin, K., Egbeleo, E., Kuessi, R., Couchoro, M. K., and Agbodji, A. E. (2023). Regulation, institutional quality, and stability of the banking system in the West African Economic and Monetary Union. Cogent Economics & Finance, 11(2). https://doi.org/10.1080/23322039.2023.2256127.

Spahiu, M. (2022). The Current Stage of Basel III Application and Its Consequences on Financial Stability: Evidence from Kosovo. Journal of Liberty and International Affairs, 8(1), 153-169. https://doi.org/10.47305/JLIA2281153s.

Tarkocin, C., and Donduran, M. (2023). Bank Stability and Systemic Risk Measurement: Application of Z-Score Variations to the Turkish Banking Sector. International Journal of Finance & Banking Studies, 12(1), 63–73. https://doi.org/10.20525/ijfbs.v12i1.2319.

Ullah, S., Hussain, S., Nabi, A. & Mubashir, K. (2022). Role of Regulatory Governance in Financial Stability: A Comparison of High and Low Income Countries. Journal of Central Banking Theory and Practice, 11(1), 207-226. https://doi.org/10.2478/jcbtp-2022-0009.

Wooldridge, J. M. (2012). Introductory econometrics: A modern approach (6th ed.). Cengage learning.

World Justice Project. (2023). Rule of Law Index. WJP Rule of Law Index Permissions. Washington, D.C. https://worldjusticeproject.org/rule-of-lawindex/downloads/WJPIndex2023.pdf.

Yitayaw, M. K., Mogess, Y. K., Feyisa, H. L., Mamo, W. B., and Abdulahi, S. M. (2022). Determinants of bank stability in Ethiopia: A two-step system GMM estimation. Cogent Economics & Finance, 11(1). https://doi.org/10.1080/23322039.2022.2161771.

Zhuja, D., Hoti, A., Qehaja, D., & Hoti, X. (2024). Assessing financial stability in Southeast Europe (SEE): An econometric perspective. Multidisciplinary Science Journal, 6(10), 2024216. https://doi.org/10.31893/multiscience.2024216.