Ekonomika ISSN 1392-1258 eISSN 2424-6166

2025, vol. 104(3), pp. 6–22 DOI: https://doi.org/10.15388/Ekon.2025.104.3.1

Cordelia Onyinyechi Omodero

Department of Accounting, College of Management and Social Sciences

Covenant University Ota, Ogun State, Nigeria

Email: onyinyechi.omodero@covenantuniversity.edu.ng

ORCID: https://orcid.org/0000-0002-8758-9756

Abstract. The challenge of tax collection in rising economies cannot be overstated. These economies have had certain economic setbacks as a result of a lack of a domestic revenue base, tax evasion, and macroeconomic and monetary issues hindering tax revenue growth. This study critically examines the key aspects influencing the tax revenue increase and collection in Sub-Saharan Africa. The dependent variable is the tax revenue, and the monetary and macroeconomic factors that influence it are inflation, income per person, foreign direct investment inflows, broad money supply, and trade openness. These characteristics are shared by several countries in Sub-Saharan Africa. The study uses the Vector Error Correction Model to analyze secondary data from the World Bank Development Indicators for the period of 1990–2023. The findings of this research show that inflation and foreign direct investment inflows have a negative association with tax revenue in the long run, but both have a significant positive impact on the tax revenue in the short term. Other factors, including the broad money supply, GDP per capita, and trade openness, have a negative but insignificant association with tax revenue. The study advises a shift in financial policy to lower inflation and increase the overall money supply. Again, a friendly business climate is required to encourage the free movement of business investment and international commerce in sub-Saharan African regions.

Keywords: Income policy, money supply, inflation, macroeconomic policy, FDI, trade, Taxation.

________

Received: 25/01/2025. Revised: 05/02/2025. Accepted: 26/05/2025

Copyright © 2025 Cordelia Onyinyechi Omodero. Published by Vilnius University Press

This is an Open Access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

Despite the growing demand for the tax income in most emerging countries in Sub-Saharan Africa, monetary and macroeconomic issues impede tax collection in these challenged locations. Numerous countries globally implemented extraordinary fiscal policies to recover from the economic crisis (Okine et al., 2023). However, Sub-Saharan African countries had a much lower average tax rate of 13% of GDP in 2022, compared to 18% in emerging and developing countries and 27% in the most prosperous countries (IMF, 2023). There is no controversy that governments need tax revenues to support the fulfilment of social commitments, but the financial policies and economic factors that determine revenue collections must be weighed and controlled. Gökpınar (2023) opines that tax proceed is unswervingly influenced by – in their entirety – all the factors distressing the revenue, prosperity and disbursements that attract tax liability because these essentials intermingle, predominantly with financial and macroeconomic pointers.

Furthermore, inability to garner adequate income and insufficient fiscal management capability have subjected African countries to a small fraction of the revenue generated by taxes, weakening their economic viability and making them vulnerable to unexpected financial perils.

Several studies on the drivers of tax income in both established and emerging countries have been conducted in the past and recently, with diverse results. Anastasiou et al. (2022) found that corruption control and strong governance improved the tax revenue collection in 26 European nations, while Nikiema and Zore (2024) corroborated this finding in Sub-Saharan Africa. Neog and Gaur’s (2020) study in India showed how economic growth, trade, government spending and inflation depleted income tax collection. Saptono and Mahmud (2021) agreed that inflation was harmful to the tax revenue, however, a price hike became a catalyst for tax revenue growth in the study of Ihuarulam et al. (2021). As for Danchev et al. (2020), the use of digital payment methods boosted tax revenue globally. Other studies (Saptono & Mahmud, 2021; Tarawalie & Hemore, 2021; He et al., 2022) proved that GDP and trade freedom helped to increase the tax revenue. These divergent outcomes from past studies have made this study crucial, especially in emerging economies such as sub-Saharan Africa. The current research is focusing on major financial and macroeconomic indicators as drivers of tax revenue collection in Sub-Saharan Africa. The main determinants identified in this present study include: GDP per capita, foreign direct investment inflows (FDII), inflation, trade openness, and broad money supply. These combined characteristics reflect financial and macroeconomic forces that determine the amount of the tax revenue which governments in Sub-Saharan African regions may collect from the taxpayer.

Thus, the study’s specific objectives include the following items:

i. To consider the implication of gross domestic product per capita on the tax revenue in Sub-Saharan Africa;

ii. To evaluate the weight of FDII on the tax revenue in Sub-Saharan Africa;

iii. To ascertain the effectiveness of broad money supply in improving the tax revenue in Sub-Saharan Africa;

iv. To examine the effect of inflation on the tax revenue in Sub-Saharan Africa;

v. To corroborate the influence of trade openness on the tax revenue in Sub-Saharan Africa.

In order to achieve the objectives outlined above, the following null hypotheses have been formulated:

H01: Gross domestic product per capita does not have any implication on the tax revenue in Sub-Saharan Africa;

H02: FDII does not actually have any weighty impression on the tax revenue in Sub-Saharan Africa;

H03: Broad money supply is not effective in improving the tax revenue in Sub-Saharan Africa;

H04: Inflation does not affect the tax revenue collection in Sub-Saharan Africa;

H05: Trade openness does not have any influence on the tax revenue in Sub-Saharan Africa.

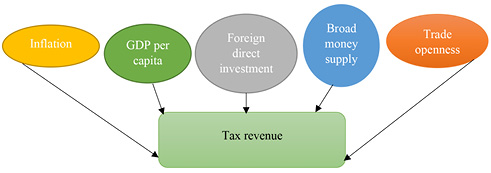

Figure 1 gives a breakdown of the study variables and the underlying conceptual assumptions. The arrow indicates the assumption that the monetary and macroeconomic factors indicated in the circles are obviously meant to affect the tax revenue collection in Sub-Saharan Africa negatively or positively.

Tax revenue (TXRV). The tax revenue is an obligatory charge on individual and corporate income in a country that is legally paid to the government to support the country’s economic and social growth. The expansion of the economy is commonly described as an increase in a country’s output that is evaluated yearly, whereas taxation represents the fraction of a country’s population’s earnings gathered by the state for which no clear equivalent return is supplied to the taxpayers (Maganya, 2020). According to Gökpınar (2023), tax revenues are impacted by a variety of factors including revenue, prosperity, and disbursements, which are associated with financial and macroeconomic trends. Taxation is the main driver of funding for the federal government, and it ensures an ongoing revenue stream for its coffers. The revenues from taxes are significant for countries that are developed as well as developing because of the tax revenue purpose, position within the fiscal framework, and status as a mandatory and periodic means of earning money (Gökpınar, 2023). Taxation is essential for encouraging long-term prosperity and decreasing poverty in emerging economies. Taxes frequently influence family choices regarding whether to use less and conserve more, to offer fewer employment opportunities, and to make investments in human resources due to their impact on financial freedom (Maganya, 2020).

Inflation (INFL). Inflation refers to the pace at which costs of commodities rise over the course of time. Inflation is often defined as a comprehensive metric that includes a spike in total costs or the general cost of everyday life in a country (Oner, 2024). In most cases, inflation is closely related to the tax income. It symbolizes emerging economies like Africa as a whole where taxes on consumption produce large income. The tax on consumption is calculated based on the worth of the transaction; hence, a hike across all prices of goods and services might result in an increased tax income (Queku et al., 2024). Inflation pushes persons into more expensive tax categories, which normally involve greater tax burdens, and reduces the monetary value of the income-free individual exemption (together with any other concessions or benefits). As a result, both the actual and marginal rates of taxation rise. This phenomenon is known as bracket creep (Beer et al., 2023). Inflation can also lead to tax evasion since the amount of tax to be paid may be too high for the taxpayer to fully comply, resulting in the government losing money.

GDP per capita (GDPC). A steady growth in GDP will ultimately result in a boost in GDP per capita, which is used to compare one country’s financial wellness to others. It serves as an instrument for comparing living conditions in different nations and throughout periods. Consequently, rising earnings raise GDP per capita, which raises the tax-to-GDP ratio.

Broad money supply (BSM2). Individuals and businesses that will comply with fiscal obligations require a broad money supply in order to access funds without being restricted by monetary authorities. In order for central banks to effectively execute their critical roles in the monetary policy, it is imperative that they possess the capability to influence the supply of money and credit, thereby maintaining market liquidity at an optimal level (Komurcuoglu & Akyazi, 2024). This is more critical when it comes to monitoring and controlling a broad money supply which falls under their purview. According to Komurcuoglu and Akyazi (2024), controllability in this context refers to the ability of the central bank to manipulate these quantities – either by increasing or decreasing them – through its monetary policy measures. Thus, if the government is to earn adequate tax revenue, the money supply must be well-regulated to benefit enterprises and the overall economic viability.

Foreign direct investment inflow. Foreign direct investment (FDI) is a type of investment made across borders whereby an investor from one country creates a long-term stake in and considerable influence over a company from another country. The flow of funds includes equity trades, profits reinvesting, and interdependent financing transactions (OECD, 2020). Through the mechanism of FDI, international enterprises bring forth new technologies, superior management practices, and advanced manufacturing techniques that can significantly elevate productivity in the host economy (Yeboah, 2025). Foreign direct investment inflows can also boost the total tax income since multinational corporations operate on a greater scale and can afford to pay their taxes on time. Furthermore, FDI functions as a means of knowledge dissemination, fostering positive spillover effects that include skill enhancement, innovation, and greater competitiveness for local industries (Yeboah, 2025). The same is expected when the government allows free trade without obstacles. It is considered that trade openness enables for the adequate collection of both direct and indirect taxes resulting from commodity purchases and sales in both international and domestic markets.

Trade openness. Commerce openness is defined as the proportion of exports and imports of goods and services over the GDP, which indicates a country’s degree of exposure to worldwide commerce. Increased trade openness may benefit exporters in two ways: costs related to exports fall while imported products and services rise. Hence, accessibility to trade and tax income are likely to have a favorable association. On the contrary, Dung (2024) opines that trade also influences economic growth by modifying the competitive landscape, permitting foreign producers to enter the market and compete with local businesses.

Kalivoshko et al. (2020) investigated the influence of macroeconomic factors on the taxation of individual earnings. The correlation examination revealed that personal income tax collections were unaffected by joblessness, the buyer pricing measure, or the proportion of unofficially engaged persons. According to the report, the overall proportion of unofficially hired people in the Ukrainian regions was 22.4%. Companies failed to tax these residents, and their governments lost money, resulting in the existence of no relationship. Neog and Gaur (2020) used flexible simultaneous mathematical models to identify the primary economic drivers of the tax revenue growth in India from 1981 to 2016. Research findings revealed that economic expansion, assistance, and commerce raised more money from taxes; however, price hikes, developmental spending, and agricultural output decreased the income tax effectiveness. Danchev et al. (2020) discovered that the widespread use of digital payment methods has a considerable helpful influence on paying taxes on time.

Ihuarulam et al. (2021) looked at the way tax income was connected to specific macroeconomic factors. The findings indicated that inflation had a favorable relationship with the tax income at a statistical importance of 5%. A one-unit rise in price increases contributed with a 0.007 boost in tax income; economic expansion was both encouraging and statistically substantial at 5%; each unit boost in GDP translated in a 0.78 improvement in governmental earnings from taxes. Ultimately, for each unit rise in joblessness, the tax output parameter fell by 0.10. Saptono and Mahmud (2021) assessed macroeconomic parameters that affected tax collections in six Southeast Asian nations between 2008 and 2019. The study indicated that per capita income, production, and trade liberalization all had a favorable and substantial impact on the real tax-to-GDP ratio and tax effort. In the contrary, inflation was deemed an unnecessary variable due to its minimal impact on the two metrics of tax effectiveness. Tarawalie and Hemore’s (2021) long-term research revealed that real GDP, open trading, and government support for development were the primary predictors of tax income in Sierra Leone, with correlations that were positive. The results were consistent with the short-term outcomes, which revealed an advantageous connection between earnings from taxes and its regression factors, real GDP and trade liberalization. However, the short-term results indicated that price increases had an adverse effect on the tax income.

Anastasiou et al. (2022) discovered that, in 26 European countries between 2015 and 2018, GDP per capita and aggregate debt, the intensity of graft management, the government’s performance measure, the quality of tax administration productivity, and the degree of rates of taxation (persons and companies) all had a major effect on the revenue from taxes. Raouf (2022) tackled the central question concerning the point whether modifications to tax income are related to improvements in financial participation. The primary results revealed a negative connection between monetary inclusion and revenues from taxes, indicating that, at low points, monetary inclusion had an adverse effect on revenues from taxes, while, at substantial levels, it had an optimistic and considerable effect on earnings from taxes. Ha et al. (2022) demonstrated that openness to economic activity, foreign direct investment, the ratio of foreign debt to GDP, and the proportion of value added in manufacturing to GDP all had a favorable influence on the collection of taxes, but government support for development had an adverse effect on revenue. According to Maryantika and Wijaya (2022), government expenditure, advancement of humanity, and economic progress all have a beneficial impact on tax collection in Indonesia, however, corruption did not impact tax receipts. In addition, expansion of the economy mitigated the effects of government expenditure and social progress on tax collections, but not the influence of malfeasance.

Omotosho (2022) studied monetary-fiscal relations in developing countries that are wealthy in resources. The research discovered proof of active financial and inactive fiscal policy, but also confirmed the existence of income replacement as a phenomenon that affects the inherent stabilizer’s function in fiscal planning. When the tax system responds to crude-related transfers in a muted manner, the revenue replacement effect is negated, taxes adjust favorably to financial obligations, and the acute inflationary effects of oil price swings are reduced. The outcomes emphasized the crucial importance of innovative fiscal strategies that are not as susceptible to natural resources rent inflows as an approach for maintaining debt levels and general economic wellness in countries with plentiful resources. According to Nyiko et al. (2022), government expenditure had a beneficial statistical impact on taxes, but price increases and trade had adverse consequences in the short term as well as in the long term. GDP growth produced a good short-term impact on taxes, but had an undesirable long-term minor effect.

Gökpınar (2023) evaluated how specific financial and macroeconomic indicators influence tax receipts in Turkey. The statistical findings demonstrated a co-integration link between revenue from taxation and all of the uncorrelated variables employed in the investigation. Based on the long-run coefficient projections, the overall funds, the manufacturing activity measure, the deposit rate of return, and export all had a positive effect on the tax level, but the rate of jobless and the currency exchange rate had an adverse consequence. In addition, the findings indicated that wide availability of money had the largest impact on tax collections. Mebratu (2023) found an upward association between revenue from taxation inefficiencies and nepotism, parliamentary oversight, rule of law, and faith-based conflicts, while a contrary relationship exists with administrative performance, internal disputes, stable governance, and armed forces involvement in the electoral process.

According to Queku et al. (2024), weakening of indigenous currencies negatively impacts the tax income. High borrowing costs, supported by expensive capital investment, might increase the tax income. The rise in inflation and FDI has a favorable impact on the tax income. The responses to impulses and variation breakdown demonstrated that fluctuations in the tax income were mostly caused by their own shifts during the periods being examined, despite the fact that foreign direct investment, exchange and inflation rates remained important. The finding was that, while the overall economic climate influences tax revenue, personal disturbances or improvements are poorly related to African tax collections. Bah (2024) examined the overall consequences of the state of institutions on revenue collection from taxes in Sub-Saharan African countries. The six quality assurance measures were: participation and credibility, stabilization of politics, excellence in regulation, rules of law, graft management, and efficiency in government. The researchers discovered that strong institutions had a favorable and considerable impact on income tax gathering in Sub-Saharan Africa. The six institutional quality measures had a beneficial effect on the overall tax receipts.

Nikiema and Zore (2024) revealed that institutional quality in Sub-Saharan Africa decreased tax revenue unsteadiness, with indirect tax collections having a greater impact than directly assessed taxes. According to Chamisa and Sunde (2024), household spending and the percentage of agricultural output in GDP had a damaging and considerable long-term influence on the tax income. The rise in GDP, price hikes, foreign direct investment, and the real rate of interest all had an upward trend – yet little influence on the amount of taxes collected was observed. Trade accessibility, the underground economy, and growing populations all demonstrated an antagonistic and non-significant relationship with tax revenues. The short-term study revealed that a lag of income taxes, GDP growth, private consumer spending, price increases, and trade permeability all had a substantial influence on tax earnings, although the percentage of agricultural products in GDP and the informal economy did not. The real rate of interest and rising populations had a beneficial though little effect on tax collection.

Zahid et al. (2024) looked at the ways that macroeconomic drivers in the South Asian area influenced budgetary long-term feasibility. The findings proved the presence of financial viability in a few Asian nations. In addition, the findings revealed that utilizing macroeconomic factors considerably increased the budgetary efficiency. Also, the outcomes demonstrated that macroeconomic issues influenced fiscal viability.

The present investigation makes use of secondary information from the World Development Indicators (WDI), a World Bank-powered initiative. The period covered by this study is from 1990 to 2023. The entire list of Sub-Saharan African countries was included in this study. The total tax income as a proportion of GDP is the dependent factor considered in this research. At the same time, macroeconomic metrics that serve as predictors include the yearly inflation rate, GDP per capita, foreign direct investment inflows, the broad money supply, and the trade-to-GDP ratio. Table 1 presents the technical descriptions of each parameter employed in this investigation.

|

Variable codes |

Description |

Source |

Expected outcome |

|

TXRV |

Tax revenue (% of GDP) |

World Bank Development Indicator (WBDI) |

Dependent variable |

|

INFL |

Inflation rate (inflation, GDP deflator – annual %) |

WBDI |

- |

|

GDPC |

Gross domestic product divided by midyear population (expressed in current US $) |

WBDI |

+ |

|

FDII |

Foreign direct investment inflow |

WBDI |

+ |

|

BSM2 |

Broad money supply |

WBDI |

+ |

|

TOPN |

Trade openness measured as the sum of exports and imports of goods and services as a ratio of GDP (% of GDP) |

WBDI |

+ |

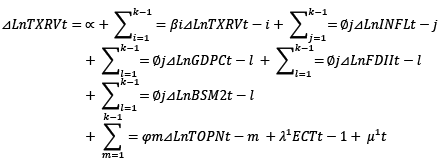

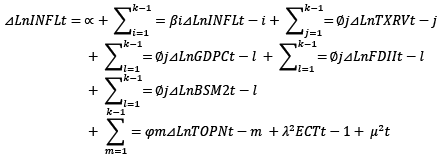

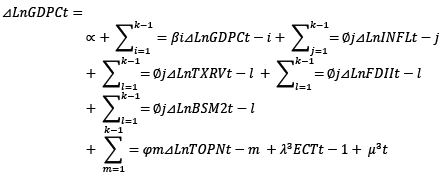

Based on the results of the unit root test in Table 3, which indicate that all series are stationary at order one, and the Johansen co-integration test in Table 5, which reveals the existence of long run co-integration among the variables used in this study, the study employs the Vector Error Correction Model (VECM), as specified in Equations 1–6.

(1)

(1)

(2)

(2)

(3)

(3)

(4)

(4)

(5)

(5)

(6)

(6)

Where:

Ln = Natural log; t = Time; k = maximum lag; β = coefficients;

Ø = difference in parameters;

K – 1 = the lag length is reduced by 1;

λ = speed of adjustment parameter with a negative sign;

βi,Øj,φm = Short-run kinetic coefficients of model modification Long-term stabilization;

ECTt–1 = the error correction term represents the lagged value of the residuals produced from the reliant variable’s co-integrating regression with the regression factors. Long run details are acquired from the long run co-integrating interaction.

μ1t = residuals (stochastic error terms frequently termed as impulses, or innovations or shocks).

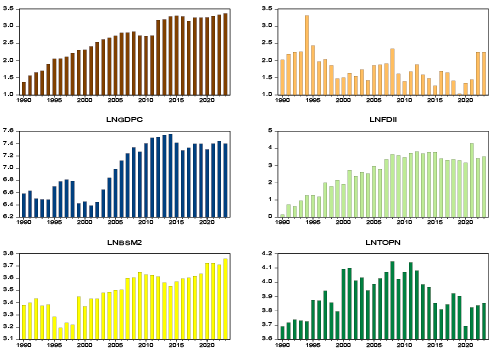

Section 4 presents a breakdown of the results gained from data analysis. This section displays all outcomes and interpretations. The findings include trend analysis (Figure 2), whereas Tables 1–7 provide descriptive statistics, the unit root test, VAR lag order selection criteria, the Johansen Co-integration Rank Test, Vector Error Correction Estimates, and diagnostic tests, respectively.

According to Figure 2, the tax income decreased significantly between 2008 and 2010, but it appears to be increasing steadily between 2021 and 2023. Inflation in the Sub-Saharan area, which was excessively high in 1994, fell to its lowest point in 2019 before rising again in 2022–2023. FDII peaked in 2020 and fell to its lowest point in 1990. GDPC was the lowest in 2001 and greatest in 2014. The broad money supply reached its peak in 2023, whereas trade-to-GDP had the worst fall in 2020.

The descriptive statistics in Table 2 demonstrate the nature of the data acquired for this investigation; essentially, they confirm whether or not the datasets are regularly distributed.

To appropriately locate the normality of the datasets, Kurtosis and Jarque-Bera are the primary statistical instruments to examine the datasets closely. The Kurtosis results are consistent with the normal distribution of datasets, whereas the Jarque-Bera probability value is greater than the 0.05 level of significance. The relevance of this finding is that all datasets used in this investigation are typically allotted.

|

TXRV |

INFL |

GDPC |

FDII |

BSM2 |

TOPN |

|

|

Mean |

2.648 |

1.812 |

7.024 |

2.676 |

3.509 |

3.917 |

|

Median |

2.723 |

1.714 |

7.182 |

3.073 |

3.520 |

3.912 |

|

Maximum |

3.378 |

3.312 |

7.555 |

4.303 |

3.758 |

4.146 |

|

Minimum |

1.374 |

1.029 |

6.388 |

0.148 |

3.194 |

3.692 |

|

Std. Dev. |

0.589 |

0.437 |

0.409 |

1.111 |

0.149 |

0.135 |

|

Skewness |

-0.509 |

1.119 |

-0.243 |

-0.707 |

-0.401 |

-0.032 |

|

Kurtosis |

2.161 |

3.249 |

1.427 |

2.327 |

2.387 |

1.899 |

|

Jarque-Bera |

2.465 |

14.26 |

3.840 |

3.476 |

1.443 |

1.720 |

|

Probability |

0.291 |

0.798 |

0.146 |

0.176 |

0.486 |

0.423 |

|

Sum |

90.05 |

61.62 |

238.8 |

90.97 |

119.3 |

133.2 |

|

Sum Sq. Dev. |

11.46 |

6.294 |

5.537 |

40.73 |

0.735 |

0.604 |

|

Observations |

34 |

34 |

34 |

34 |

34 |

34 |

|

Variable |

ADF-Statistics |

Critical value @ 5% |

p-value |

Order of Integration |

|

LNTXRV |

-5.461 |

-2.957 |

0.000 |

I(1) |

|

LNINFL |

-6.581 |

-2.957 |

0.000 |

I(1) |

|

LNGDPC |

-4.134 |

-2.957 |

0.003 |

I(1) |

|

LNFDII |

-10.08 |

-2.957 |

0.000 |

I(1) |

|

LNBMS2 |

-6.804 |

-2.957 |

0.000 |

I(1) |

|

LNTOPN |

-5.434 |

-2.960 |

0.000 |

I(1) |

The unit root test in Table 3 provides a signal that the series are stable at order one, which means that no series is stationary at level. As a result, if there is no evidence of long-term co-integration, we should employ the Vector Autoregressive (VAR) Model, or VECM if long-term co-integration is confirmed. However, before determining whether or not there is a long-run relationship between the series, a lag selection test is required to lead the testing of a long-run relationship. The lag order selection test is shown in Table 4. The results demonstrate that all of the criteria utilized picked lag 2 as the suitable lag for the long-term computation, as shown in Table 5.

|

Lag |

LogL |

LR |

FPE |

AIC |

SC |

HQ |

|

0 |

22.99 |

NA |

1.398 |

-1.062 |

-0.787 |

-0.971 |

|

1 |

157.6 |

210.4 |

3.051 |

-7.228 |

-5.305* |

-6.591 |

|

2 |

203.2 |

54.03* |

2.181* |

-7.822* |

-4.249 |

-6.638* |

|

Hypothesized No. of CE(s) |

Eigenvalue |

Trace Statistic |

0.05 Critical Value |

Prob.** |

|

None * |

0.795161 |

172.2486 |

95.75366 |

0.0000*** |

|

At most 1 * |

0.732505 |

123.0972 |

69.81889 |

0.0000*** |

|

At most 2 * |

0.705074 |

82.21889 |

47.85613 |

0.0000*** |

|

At most 3 * |

0.505388 |

44.36692 |

29.79707 |

0.0006*** |

|

At most 4 * |

0.375564 |

22.54350 |

15.49471 |

0.0037*** |

|

At most 5 * |

0.226093 |

7.945391 |

3.841466 |

0.0048*** |

|

Max-Eigen Co-integration Rank Test |

||||

|

Hypothesized No. of CE(s) |

Eigenvalue |

Max-Eigen Statistic |

0.05 Critical Value |

Prob.** |

|

None * |

0.795161 |

49.15145 |

40.07757 |

0.0037*** |

|

At most 1 * |

0.732505 |

40.87830 |

33.87687 |

0.0062*** |

|

At most 2 * |

0.705074 |

37.85197 |

27.58434 |

0.0017*** |

|

At most 3 * |

0.505388 |

21.82342 |

21.13162 |

0.0399** |

|

At most 4 * |

0.375564 |

14.59811 |

14.26460 |

0.0443** |

|

At most 5 * |

0.226093 |

7.945391 |

3.841466 |

0.0048*** |

Table 5 shows that the Johansen and Max-Eigen Co-integration Rank Tests indicate the presence of a long-run association that is significant at the 0.01 (***) and 0.05 (**) levels of significance. As a result, we conclude that the series have a long-run connection and that the use of VECM for an estimate is suitable. This means that the null hypothesis that there is no long-run link between series has been rendered incorrect.

Long run estimation result

|

Co-integrating Equation (Eq): |

CointEq1 |

|

LNTXRV(-1) |

1.000 |

|

LNINFL(-1) |

-0.243(0.09)* |

|

LNGDPC(-1) |

0.218(0.15) |

|

LNFDII(-1) |

-1.002(0.08)* |

|

LNBSM2(-1) |

1.277(0.38) |

|

LNTOPN(-1) |

3.183(0.32) |

|

C |

-25.18 |

Short run VECM estimation result

|

Error Correction: |

D(LNTXRV) |

D(LNINFL) |

D(LNGDPC) |

D(LNFDII) |

D(LNBSM2) |

D(LNTOPN) |

|

CointEq1 |

0.08(0.08)* |

0.22(0.35) |

0.01(0.09)* |

0.82(0.27) |

0.06(0.05)** |

-0.14(0.07)* |

|

D(LNTXRV(-1)) |

-0.13(0.19) |

-1.29(0.81) |

-0.04(0.23) |

-0.88(0.62) |

-0.15(0.12) |

0.02(0.17) |

|

D(LNINFL(-1)) |

0.07(0.05)** |

-0.05(0.22) |

0.02(0.06)* |

0.25(0.16) |

0.02(0.03)** |

-0.03(0.04)** |

|

D(LNGDPC(-1)) |

-0.12(0.22) |

-0.49(0.91) |

0.59(0.25) |

-0.48(0.69) |

-0.01(0.14) |

0.07(0.19) |

|

D(LNFDII(-1)) |

0.12(0.06)* |

0.37(0.28) |

-0.01(0.08)* |

-0.08(0.21) |

-0.00(0.04)** |

-0.11(0.06)* |

|

D(LNBSM2(-1)) |

-0.67(0.46) |

-1.45(1.85) |

0.90(0.52) |

-1.67(1.42) |

-0.24(0.28) |

0.89(0.39) |

|

D(LNTOPN(-1)) |

-0.17(0.27) |

-0.82(1.08) |

-0.16(0.31) |

-1.41(0.83) |

-0.15(0.16) |

0.28(0.23) |

|

C |

0.06(0.02) |

0.07(0.09) |

0.00(0.02) |

0.18(0.07) |

0.02(0.01) |

0.00(0.02) |

|

R-squared |

0.177 |

0.155 |

0.248 |

0.496 |

0.196 |

0.309 |

|

Adj. R-squared |

-0.061 |

-0.091 |

0.028 |

0.349 |

-0.037 |

0.107 |

|

S.E. equation |

0.102 |

0.411 |

0.116 |

0.314 |

0.062 |

0.088 |

|

F-statistic |

0.742 |

0.631 |

1.129 |

3.376 |

0.839 |

1.532 |

Table 6 presents the results of the Vector Error Correction Estimates, which illustrate the long-run link between the variables as well as the short-term connectivity and the point at which the long-run disequilibrium may be rectified. The long-run outcome shows that inflation is harmful to tax revenue collection, with a t-statistic of -0.243 and a p-value of 0.09. This conclusion supports the work of Neog and Gaur (2020), but contradicts the findings of Ihuarulam et al. (2021). Furthermore, the foreign direct investment inflow has a t-statistic of -1.002 and a p-value of 0.08 indicating that, at the 10% level of significance, the foreign direct investment inflow has no long-term beneficial effect on tax earnings in Sub-Saharan Africa. This result is in slight contradiction if compared with theoretical literature which tends to believe that FDI is meant to boost the tax revenue. The phenomenon of domestic tax base erosion and the strategic shifting of profits, commonly known as Base Erosion and Profit Shifting (BEPS), illustrates the tactics employed by multinational corporations to exploit transfer pricing and thin capitalization techniques for the purpose of profit relocation from African countries. BEPS refers to the tax planning strategies that multinational enterprises utilize to exploit loopholes in tax laws, thereby facilitating the artificial transfer of profits to jurisdictions characterized by low or nonexistent tax rates, thus circumventing tax responsibilities (OECD, 2024). Therefore, while the taxation of profits yields short-term benefits for the African region, a detailed analysis of tax legislation over time uncovers methods of tax avoidance that ultimately create an adverse relationship between Foreign Direct Investment (FDI) and tax revenue in the long run. Although, the OECD/G20 BEPS Project now equips governments with essential regulations and instruments to address tax avoidance, thereby ensuring that profits are taxed in the jurisdictions where the economic activities that generate them take place, and where value is created (OECD, 2024). The Error Correction Term (ECT) is useful in analyzing short-term connections. It also looks at whether the framework has the capacity to recover to equilibrium over time after an abrupt shift. Table 6 shows the observed results for the ECT technique. CointEq1 is a measure of the regression equation’s correcting error coefficient. The ECT coefficient is found to be positive and statistically significant at the 10% level. It displays an upward convergence rate, with the model becoming 8% closer to equilibrium each year.

Short-run estimations show that inflation is favorably linked with the broad money supply and tax income at the 5% level of relevance and GDPC at the 10% level, but there is a significant negative correlation with trade openness at the 5% level of materiality. FDII has a substantial negative relationship with the broad money supply at the 5% level of significance, as well as a negative relationship with trade openness and GDPC at the 10% level, but a positive relationship with the tax income. The results are congruent with the findings of Queku et al., 2024.

The model is stable and devoid of serial correlation and heteroskedasticity, as shown in Table 7. The p-values are above the 0.05 threshold, implying that the model is suitable for this study. As a result, the findings of this study are credible and relevant to policymaking.

|

Chi-sq |

Prob. |

|

294.47 |

0.481 |

VECM Residual Serial Correlation LM Tests

|

LM-Stat |

Prob |

|

17.66 |

0.99 |

The study investigates how monetary instruments and macroeconomic conditions influence tax revenue collection in Sub-Saharan Africa. The low tax income in Sub-Saharan Africa is due to a number of issues, some of which are considered in this paper. The findings demonstrate that inflation and foreign direct inflows are the most important factors influencing the amount of tax income collected in Sub-Saharan Africa. In the long run, both inflation and FDII had a negative and substantial impact on the tax income, although, in the near term, there is a positive link between them, resulting in a faster correction of errors that arise over time to the tone of 8% ECT coefficient.

Other parameters, such as the broad money supply, trade openness, and GDP per capita, have a negative but intangible relationship with tax revenue. On this point, the study recommends more practical steps to manage inflation rates in all Sub-Saharan African nations. The study suggests that regional monetary authorities and governments should work together to put all measures in place to prevent commodity and service price increases in Sub-Saharan Africa. It is also critical to consider developing a favorable business environment that would allow international investors to operate smoothly. If the business environment is favorable, international enterprises will be attracted to the region. Thus, the political structure in Sub-Saharan Africa should be harmonized to create a suitable environment for foreign corporations to continue operations and contribute to the well-being of African regions.

It is essential for policymakers to establish robust strategies aimed at managing long- and short-term economic fluctuations affecting tax revenue growth. This can be achieved through the implementation of stringent macroeconomic and monetary policies, the enhancement of financial market stability, and the promotion of domestic market broadening to alleviate the negative impacts on revenue growth. The fiscal measures should include more government expenditure in infrastructural development and control of the prices of goods and services in order to reduce inflation. Sub-Saharan African governments should endeavor to design and implement macroeconomic policies that are both effective and fair. This dual focus is essential not only for stimulating economic activity but also for fulfilling the important obligation of advancing the well-being of their citizens. This study’s practical application is expected to mitigate inflation by establishing monetary policies that will lower the prices of goods and services within local markets. Consequently, this will result in a reduction of imports of similar products and an increase in the export of domestic goods, ultimately enhancing foreign earnings. However, the analysis is constrained by data (notably, the limitations include information on the exchange rate, unemployment rate, and other macroeconomic and financial instruments that are not included in this work). As a result, more research is advised to incorporate all of these elements, as well as to extend the study to other parts of the world.

AL-Qudah, A.M. (2021). The determinants of tax revenues: Empirical evidence from Jordan. International Journal of Financial Research, 12(3), 43-54. https://doi.org/10.5430/ijfr.v12n3p43.

Anastasiou, A., Kalligosfyris, C., & Kalamara, E. (2022). Determinants of Tax Revenue Performance in European Countries: A Panel Data Investigation. International Journal of Public Administration, 47(4), 227–242. https://doi.org/10.1080/01900692.2022.2111578.

Bah, M. (2024). Tax revenue mobilization and institutional quality in sub-Saharan Africa: An Empirical investigation. African Development Review, African Development Bank, 36(2), 201-221. https://doi.org/10.1111/1467-8268.12752.

Beer, S., Mark, G., & Klemm, A. (2023). Tax distortions from inflation: What are They? How to Deal with Them? IMF Working Paper WP/23/18. https://www.imf.org/en/Publications/WP/Issues/2023/01/27/Tax-Distortions-from-Inflation-What-are-They-How-to-Deal-with-Them-528666.

Chamisa, M.G., & Sunde, T. (2024). Key determinants of tax revenue in Zimbabwe: assessment Using autoregressive distributed lag (ARDL) approach. Cogent Economics & Finance, 12(1), 1-21. https://doi.org/10.1080/23322039.2024.2386130.

Danchev, S., Gatopoulos, G., & Vettas, N. (2020). Penetration of digital payments in Greece after Capital controls: Determinants and impact on VAT revenues. CESifo Economic Studies, 2020, 198-220. DOI: 10.1093/cesifo/if2019.

Dung, N. D. (2024). How Productivity and Trade Liberalization Can Affect the Economies of Developing Nations is Illustrated by the Vietnamese Manufacturing Sectors Case. Organizations and Markets in Emerging Economies, 15(1(30), 109-126. https://doi.org/10.15388/omee.2024.15.6.

Gökpınar, S. (2023). Monetary and macroeconomic determinants of tax revenue: The case of Türkiye. Journal of Economics Business and Political Researches, 8(Special Issue), 202-216. https://doi.org/10.25204/iktisad.1302035.

Ha, M.N., Minh, P.T, & Binh, Q.M.Q. (2022). The determinants of tax revenue: A study of Southeast Asia. Cogent Economics & Finance, 10(1). https://doi.org/10.1080/23322039.2022.2026660.

Hamdan, S., & Rana, F. (2021). Determinants of tax revenue in emerging countries. Palarch’s Journal of Archaeology of Egypt/Egyptology, 18(13), 98-106. https://archives.palarch.nl/index.php/jae/article/view/8073/7545.

Ihuarulam, G.I., Sanusi, G.P., & Oderinde, L.O. (2021). Macroeconomic determinants of tax Revenue in economic community of West African States. The European Journal of Applied Economics, 18(2), 62-75. DOI: 10.5937/EJAE18-30727.

IMF (2023). IMF/Sub-Saharan Africa’s Regional Economic Outlook. Retrieved on September 28, 2024 From: https://mediacenter.imf.org/news/imf---sub-saharan-africa-s-regional-economic-outlook/s/f49aa94a-c5ca-489f-bfba-46523ff3d1bc.

Kalivoshko, O., Kraevsky, V., & Payanok, T. (2020). Assessment of Factors Influencing the Volume of Personal Income Tax Revenues. IEEE International Conference on Problems of Infocommunications. Science and Technology (PIC S&T), Kharkiv, Ukraine, 2020, 279-282. DOI: 10.1109/PICST51311.2020.9468000.

Komurcuoglu, O.F., & Akyazi, H. (2024). Novel analysis on the impact of fintech developments For monetary policy: The case of Turkiye. Ekonomika, 103(3), 70-90. https://doi.org/10.15388/Ekon.2024.103.3.5.

Maganya, M.H. (2020). Tax revenue and economic growth in developing country: an Autoregressive distribution lags approach. Central European Economic Journal, 7(54), 205-217. https://doi.org/10.2478/ceej-2020-0018.

Maryantika, D.D., & Wijaya, S. (2022). Determinants of tax revenue in Indonesia with economic Growth as a mediation variable. Jurnal Penelitian Pendidikan Indonesia, 8(2), 450-465. http://dx.doi.org/10.29210/020221522.

Mebratu, A.A. (2023). Tax revenue inefficiency and political risk factors: The Hen or The egg? Cogent Business & Management, 10(1), 1-19, https://doi.org/10.1080/23311975.2023.2167546.

Neog, Y., & Gaur, A.K. (2020). Macro-economic determinants of tax revenue in India: an Application of dynamic simultaneous equation model. International Journal of Economic Policy in Emerging Economies, 13(1), 13-35. https://doi.org/10.1504/IJEPEE.2020.106679.

Nikiema, R., & Zore, M. (2024). Tax revenue instability in Sub-Saharan Africa: Does institutional Quality matter? The American Journal of Economics and Sociology, 2024, 1-25. https://doi.org/10.1111/ajes.12598.

Nyiko, W.H., Daw, O.D., & Mixo, S. (2022). Determinants of taxation in South Africa: an Econometric approach. Munich Personal RePEc Archive No. 114962. https://mpra.ub.uni-muenchen.de/114962/.

OECD (2024). Foreign direct investment (FDI). Retrieved on October 16, 2024 from: https://doi.org/10.1787/9a523b18-en.

OECD (2024). Base erosion and profit shifting (BEPS). Retrieved on November 29, 2024 from: https://www.oecd.org/en/topics/policy-issues/base-erosion-and-profit-shifting-beps.html

Omotosho, B.S. (2022). Monetary and fiscal policy interactions in resource-rich emerging Economies. Macroeconomics and Finance in Emerging Market Economies, 17(2), 249–270. https://doi.org/10.1080/17520843.2022.2042974.

Oner, C. (2024). Inflation: Prices on the rise. IMF Finance and Development Magazine. Retrieved On September 29, 2024. https://www.imf.org/en/Publications/fandd/issues/Series/Back-to-Basics/Inflation.

Okine, C. K. R., Appiah, M., & Tetteh, D. (2023). The Linkage Between Fiscal Policy and Financial Development: Exploring the Moderating Role of Institutional Quality in Emerging Economies. Organizations and Markets in Emerging Economies, 14(3), 670–695. https://doi.org/10.15388/omee.2023.14.10.

Queku, Y.N., Seidu, B.A., Attom, B.E., Carsamer, E., Adam, A.M., Fayeme, M., Acquah, S. (2024). Tax Revenue Performance in Africa: Does Macroeconomic Environment Matter? Journal of Tax Reform, 10(2), 271–291. https://doi.org/10.15826/jtr.2024.10.2.169.

Raouf, E. (2022). The impact of financial inclusion on tax revenue in EMEA countries: A threshold regression approach. Borsa Istanbul Review, 22(6), 1158-1164. https://doi.org/10.1016/j.bir.2022.08.003.

Tarawalie, A.B., & Hemore, S. (2021). Determinants of tax revenue in Sierra Leone: Application of the ARDL framework. Journal of Economics and Management Sciences, 4(4), 25 – 34. https://doi.org/10.30560/jems.v4n4p25.

Wahyudi, W. (2020). The relationship between government spending and economic growth Revisited. International Journal of Economic and Financial Issues, 10(6), 84 – 88. https://doi.org/10.32479/ijefi.10614.

Saptono, P.B. & Mahmud, G. (2021). Macroeconomic Determinants of Tax Revenue and Tax Effort in Southeast Asian Countries. Journal of Developing Economies, 6(2), 253-274.

Yeboah, E. (2025). The Effect of Foreign Direct Investment, Domestic Investment, and Trade on Economic Growth: Evidence from the Baltic Countries. Ekonomika, 103(4), 129-150. https://doi.org/10.15388/Ekon.2024.103.4.8.

Zahid, J., Jadoon, A.K., Hamza, B., & Ali, M. (2024). Macroeconomics determinants of fiscal Sustainability in the Asian countries. Bulletin of Business and Economics, 13(1), 193 – 201. https://doi.org/10.61506/01.00188.