Ekonomika ISSN 1392-1258 eISSN 2424-6166

2026, vol. 105(2), pp. 103–123 DOI: https://doi.org/10.15388/Ekon.2026.105.2.6

Assessing the Financial Impact of ESG Portfolio Optimization and Diversification in an Emerging Market: Evidence from Mexico

Paula Margarita Fosado Olvera

Faculty of Accounting and Administration, Autonomous University of Querétaro, Mexico

ORCID: https://orcid.org/0009-0000-3284-1558

ROR: https://ror.org/00v8fdc16

E-mail: pfosado08@alumnos.uaq.mx

Roberto Yoan Castillo Dieguez*

Faculty of Accounting and Administration, Autonomous University of Querétaro, Mexico

ORCID: https://orcid.org/0000-0002-3352-2265

ROR: https://ror.org/00v8fdc16

E-mail: roberto.castillo@uaq.mx

Abstract. This paper evaluates the financial implications of scaling and diversifying stock portfolios based on environmental, social, and governance (ESG) criteria in the Mexican Stock Exchange. By using a sample of firms from the S&P/BMV IPC index (2020–2024), four portfolios were constructed: High ESG, Low ESG, a Benchmark, and an Optimized ESG portfolio built through quantitative algorithms. Results from GARCH (1,1) models show that High ESG portfolios exhibited higher conditional volatility, particularly during periods of uncertainty such as 2020 and 2022, while the Optimized ESG portfolio achieved faster convergence to lower risk, signaling greater stability. Random Forest analysis identified governance, leverage, and lagged WACC as the strongest predictors of financing costs, surpassing aggregate ESG scores. Backtesting further revealed that High ESG portfolios faced more frequent breaches, whereas the Optimized ESG portfolio better contained volatility but struggled with extreme losses. ESG criteria enhance the portfolio design when combined with robust financial indicators.

Keywords: ESG, portfolio optimization, GARCH model, cost of capital, sustainable finance, volatility, emerging markets.

__________

* Correspondent author.

Received: 16/06/2025. Accepted: 16/03/2026

Copyright © 2026 Paula Margarita Fosado Olvera, Roberto Yoan Castillo Dieguez. Published by Vilnius University Press

This is an Open Access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

1. Introduction

In the last decade, sustainable investment based on Environmental, Social, and Governance (ESG) factors has grown exponentially in international financial markets. The popularity of ESG assets has sparked debate about their impact on performance, volatility, and cost of capital. While some studies suggest that ESG portfolios strengthen risk management (Peliu, 2024), others argue that excluding assets reduces diversification and expected returns (Beloskar & Nageswara Rao, 2024; Ravina & Persico, 2025).

Portfolio theory emphasizes diversification as a means of reducing risk without sacrificing returns. However, ESG criteria may limit this efficiency by introducing selection bias and higher exposure to systematic risk. Evidence is inconclusive on whether ESG portfolios lower the cost of capital compared to the traditional ones, as outcomes depend on how markets perceive corporate sustainability.

Sustainable investment has expanded rapidly through green bonds, ESG funds, and other instruments (Arévalo et al., 2024; Billio et al., 2024). Yet, in emerging economies like Mexico, the effectiveness of ESG integration remains uncertain due to regulatory incoherence, shallow markets, and risks of greenwashing. Institutional investors also face trade-offs between fiduciary duties and sustainability, particularly when financial returns are ambiguous or context-dependent.

This study addresses the following question: How does ESG portfolio optimization and diversification affect volatility, profitability, and cost of capital in Mexico? The objective is to analyze these relationships by using econometric and machine learning approaches.

Based on portfolio and stakeholder theory, we test whether: (i) High ESG portfolios exhibit higher conditional volatility than benchmarks, (ii) Optimized ESG portfolios reduce volatility persistence and dispersion, and (iii) Governance factors, rather than aggregate ESG scores, explain the cost of capital.

Unlike prior Latin American studies that mainly rely on static econometric tests, this research introduces a hybrid framework combining GARCH (1,1), Random Forest, and VaR backtesting to jointly evaluate volatility dynamics and the cost of capital.

The paper proceeds as follows: Section 2 reviews recent ESG literature; Section 3 describes the methodology, sample, and hypotheses; Section 4 reports results from GARCH, Random Forest, and backtesting; and Section 5 presents conclusions and implications.

2. Literature Review

Sustainable investment has expanded considerably in recent decades. With the growing relevance of Environmental, Social, and Governance (ESG) criteria, investors assess not only financial performance but also firms’ environmental and social footprint and governance quality (Marti et al., 2024). Early studies suggest that high-ESG portfolios may offer lower risk and greater resilience during crises, though evidence on their effect on profitability remains inconclusive (Gianfrate et al., 2024; Kaminskyi et al., 2025).

Key findings cluster around three dimensions. (1) Diversification and risk: ESG assets can reduce volatility in developed markets, but results in emerging economies are less clear (Al Amosh, 2024; Alvarez-Perez et al., 2024). (2) Optimization and profitability: while some studies show an improved performance through ESG-based portfolio optimization, others warn that restrictions may reduce returns (Alves & Meneses, 2024). (3) Cost of capital: firms with stronger ESG practices often access cheaper financing, though evidence remains mixed (Priem & Gabellone, 2024).

In emerging markets, results are heterogeneous. ESG portfolios sometimes outperform the traditional ones (Gangwani & Kashiramka, 2024; Vivek, 2024), and yet their benefits appear weaker than in developed economies, where institutions play a decisive role (Cankaya & Naeem, 2022). In Latin America, studies show partial advantages – such as improved diversification, profitability, and a lower cost of capital mainly through governance (Alvarez-Perez et al., 2024; Ramirez et al., 2022). In Asia and Africa, findings are mixed: ESG performance reduced volatility in India during COVID-19 (Beloskar & Rao, 2022), while social factors were found to dominate in Southeast Asia (Kartikasary et al., 2023); elsewhere, negative or sector-dependent effects emerged (Johnson, 2020)

By contrast, European studies highlight stronger benefits under robust regulation. The EU Taxonomy and SFDR have improved access to credit, portfolio resilience, and disclosure quality, though challenges in transition risk and metric standardization still persist (Alessi & Battiston, 2022; Cauthorn et al., 2023; Martinez-Meyers et al., 2024; Sautner et al., 2022). Comparative evidence confirms divergence: Europe shows consistent positive outcomes, while emerging economies report mixed or negative ones (Siddiqui et al., 2024). Exceptions in Brazil and India underline the role of regulatory maturity (H. Gupta & Chaudhary, 2023)

In sum, three trends emerge: (i) ESG assets yield stronger benefits in developed markets with consolidated regulation, especially in the EU; (ii) in Latin America and Asia, results are partial and inconsistent; and (iii) in emerging economies, institutional and governance factors weigh more than environmental or social ones. This reinforces the importance of analyzing the Mexican case, where shallow markets and regulatory gaps may condition ESG’s financial impact.

To structure these findings, Table 1 synthesizes recent evidence (2020–2024) by region and approach. It shows that, while consolidated frameworks generate consistent advantages, outcomes in Latin America, Asia, and Africa remain heterogeneous, underscoring the need for empirical testing in Mexico.

Table 1. Recent evidence on ESG performance in emerging and developed markets (2020–2024)

|

Region / Focus

|

Authors

|

Main Variables

|

Methods / Techniques

|

Main Findings

|

|

Emerging Markets (general)

|

Lerskullawat & Ungphakorn (2024)

|

ESG scores and disclosure – returns, risk, financial performance.

|

Portfolio models; GMM; panel regressions; GARCH.

|

ESG improves returns and reduces volatility in some cases; effects are stronger in developed markets and are also context-dependent.

|

|

Latin

America

|

(Alvarez-Perez et al., 2024; Ramirez et al., 2022)

|

ESG indices; E/S/G factors – returns, Sharpe ratio, cost of capital, ESG disclosure.

|

Monte Carlo, OLS panel, Tobit.

|

ESG indices enhance diversification; governance lowers cost of capital; disclosure is linked to board quality.

|

|

Asia

|

Beloskar & Rao (2022); Kartikasary et al., (2023)

|

ESG scores, disclosure, emissions – returns, market value, Tobin’s Q.

|

OLS; multiple regressions; DID; nonlinear models.

|

Mixed: ESG protects in crises (India); social pillar is strongest (SE Asia); negative/ non-linear impacts are observed in ASEAN.

|

|

Africa

|

Johnson (2020)

|

ESG disclosure – WACC.

|

OLS Panel, FE/RE.

|

ESG disclosure lowers WACC in consumption, but raises it in industrial sectors.

|

|

Global Comparisons (developed vs. emerging)

|

A. Gupta & Sharma (2023); Siddiqui et al., (2024)

|

ESG – value, returns, performance.

|

GLS panel; GARCH; panel regressions.

|

Developed markets show consistent benefits; emerging markets show mixed or negative results due to weak institutions.

|

|

Cost of capital and governance

|

Bilyay-Erdogan & Öztürkkal (2023); Dwomor & Mensah (2024)

|

ESG reporting and scores – cost of capital, profitability, ownership.

|

GLS panel; multivariate analysis.

|

ESG reporting reduces WACC and boosts performance; governance and ownership moderate the effect.

|

Source: Own elaboration.

Linking ESG research to the broader framework of sustainable finance and global governance is essential. Institutions such as the GRI, PRI, and OECD have established standards that align investments with sustainability objectives, shaping global capital allocation. The spread of green bonds and sustainable taxonomies has further encouraged emerging markets to adopt practices consistent with the 2030 Agenda and SDGs. In this context, the Mexican case demands an empirical approach that not only contrasts ESG and traditional portfolios but also tests whether ESG integration enhances efficiency or exposes structural constraints typical of emerging markets.

3. Methodology

3.1. Theoretical underpinnings of the methodological design

The modern portfolio theory (Markowitz, 1952; Sharpe, 1964) constitutes the analytical basis of this study, as it allows modeling the impact of diversification and optimization on the risk-return relationship. Recent studies in emerging markets have applied this framework to evaluate the superiority of ESG portfolios over the traditional ones, highlighting their resilience during turbulence (Vivek, 2024). However, these approaches mainly emphasize risk and return, without explicitly considering institutional and social elements that condition ESG integration in markets with a limited depth.

Complementarily, the stakeholder theory (Freeman, 2010) and its extension in emerging markets (Dwomor & Mensah, 2024) provides a framework to understand how ESG-based investment decisions transcend financial logic and align value creation with social, regulatory, and environmental expectations. Together, portfolio theory and stakeholder theory enable an empirical assessment of whether the benefits attributed to sustainable investment in emerging markets like Mexico are supported beyond rhetoric, accounting for diversification efficiency and institutional pressures.

3.2. Approach and methodological design

This research adopts a quantitative approach with an explanatory and correlational scope, analyzing the impact of ESG portfolio optimization on volatility, profitability, and cost of capital in Mexican listed firms. Advanced econometric tools and machine learning algorithms are employed to identify causal and non-linear relationships.

3.3. Sample and data sources

The sample includes the 35 companies of the S&P/BMV IPC index, which represent over 90% of the Mexican market value (Rossignolo, 2024). Only firms with complete annual financial statements and ESG scores in Refinitiv for 2020–2024 were considered. Financial indicators were drawn from reports and statements, while ESG scores (aggregate and subcomponents) were obtained from Refinitiv Eikon. Refinitiv was selected for its broad coverage of Latin American issuers and methodological consistency across the ESG pillars, although variations in scoring criteria relative to other providers (e.g., MSCI, Sustainalytics) may introduce comparability limitations. The chosen period captures shocks such as COVID-19 and regulatory shifts in sustainable finance.

3.4. Variables

Dependent variables are portfolio returns, volatility, and the cost of capital (WACC). Independent variables include diversification measures (Herfindahl-Hirschman index, correlations) and ESG ratings (aggregate and E, S, G pillars). Control variables cover leverage (D/E) and the firm size. Table 2 summarizes the variables and sources.

Table 2. Description of Variables

|

Variable

|

Description

|

Calculation/Source

|

Type

|

Representative authors

|

|

Rt

|

Annual logarithmic return of the portfolio

|

|

Dependent

|

Agarwal & Muppalaneni (2022)

|

|

Volatility

|

Standard deviation of returns

|

Statistical calculation on time series

|

Dependent

|

Dahlquist & Ibert (2024)

|

|

WACC

|

Weighted average cost of capital

|

Refinitiv / Financial statements

|

Dependent

|

Franc-Dąbrowska et al. (2021)

|

|

HHI

|

Portfolio concentration index

|

|

Independent

|

De Rosa et al. (2022)

|

|

Correlation

|

Average correlations between portfolio assets

|

Historical correlation matrix

|

Independent

|

De Rosa et al. (2022)

|

|

ESG Score

|

Total ESG score (0–100)

|

Refinitiv

|

Independent

|

Garcia-Bernabeu et al. (2024)

|

|

E, S, G Scores

|

Subcomponents of ESG performance

|

Refinitiv

|

Independent

|

Garrido-Merchán et al. (2023); Agliardi et al. (2023)

|

|

D/E

|

Debt-to-equity ratio

|

Total debt / Equity

|

Controlled

|

Franc-Dąbrowska et al. (2021)

|

|

Size

|

Company scale

|

Logarithm of total assets

|

Controlled

|

Melinda (2004)

|

Source: Own elaboration.

3.4.1. Justification for the selection of variables

The variable selection follows the principles of sustainable finance and empirical evidence. Portfolio returns (Rt) measure the financial performance, while volatility captures risk exposure – which is especially relevant in emerging markets that are prone to shocks and variance clustering (Dahlquist & Ibert, 2024). The Weighted Average Cost of Capital (WACC) reflects financing conditions and their sensitivity to governance and ESG practices (Franc-Dąbrowska et al., 2021).

Independent variables represent the portfolio structure and ESG attributes. The Herfindahl-Hirschman Index (HHI) and average correlations measure diversification, as concentration and interdependence determine ESG integration benefits (De Rosa et al., 2022). ESG ratings – both aggregate and by pillars (E, S, G) – assess whether sustainability dimensions relate systematically to financial outcomes (Agliardi et al., 2023; Garcia-Bernabeu et al., 2024).

Control variables mitigate firm-level bias. The Debt-to-Equity ratio (D/E) proxies leverage, influencing both risk and financing costs, while the firm size (log assets) accounts for scale advantages in its market access and visibility. Together, these variables allow a more precise assessment of ESG effects on performance and strengthen the validity of the empirical analysis.

3.5. Portfolio construction

To assess the impact of ESG considerations on financial performance in the Mexican stock market, four portfolios were constructed:

i) High ESG Portfolio, including the ten companies with the highest ESG scores (2020–2024), to test whether sustainability leaders outperform.

(ii) Low ESG Portfolio, with the ten lowest ESG scorers, serving as a control to evaluate penalties from weak ESG.

(iii) Benchmark Portfolio, replicating the S&P/BMV IPC index, used as a market proxy.

(iv) Optimized ESG Portfolio, built through quantitative selection and weighting methods – such as maximizing the Sharpe ratio under ESG constraints (Vasiliauskaitė, 2004) – so that to capture the added value of optimization.

Additional variants (e.g., sectoral or rolling ESG portfolios) were explored but omitted for feasibility and editorial conciseness. Together, these portfolios capture cross-sectional and temporal dynamics, providing a robust framework for emerging-market sustainable finance.

3.6. Analysis techniques

Empirical analysis is carried out in three complementary stages that aim to evaluate the robustness of the results:

Garch Model

To capture temporal dynamics and volatility clustering in financial series, we apply a GARCH model (Tsay, 2010). Let rt denote log returns of ESG portfolios:

(1)

(1)

with conditional variance:

(2)

(2)

where ϵt ~ i.i.d.(0,1), α0 > 0, αi ≥ 0, βj ≥ 0 , and ∑(αi + βj) < 1.

The GARCH (1,1) benchmark is suitable to assess volatility persistence (α+β) and to test whether High ESG portfolios exhibit systematically higher conditional variance than Low ESG or Optimized portfolios.

Random Forest Methodology

To identify predictors of financial performance, we employ Random Forest (Breiman, 2001), an ensemble method that builds multiple decision trees with bootstrap samples and random feature selection. Each tree estimates portfolio outcomes (volatility, return, WACC), and predictions are averaged across T trees:

(3)

(3)

Variable importance is evaluated through permutation and Gini metrics, allowing us to assess the relative contribution of ESG pillars (E, S, G), leverage, and past WACC. The model is validated with cross-validation and grid search to ensure predictive accuracy and avoid overfitting.

Financial backtesting

To test the robustness of ESG-oriented portfolio strategies, an ex-post backtesting procedure was applied using a rolling window for 2019–2024, following Value-at-Risk (VaR) validation methods (Kupiec, 1995). For each portfolio – i.e., High ESG, Low ESG, Benchmark, and Optimized ESG – a binary hit sequence was defined as:

The null hypothesis of correct conditional risk control is H0 = Et[It+1] = p, where p denotes the expected violation rate (e.g., 5%). This model-agnostic approach avoids restrictive distributional assumptions and evaluates whether ESG constraints reduce or amplify financial instability by analyzing the frequency and randomness of breaches.

4. Results

4.1. Composition and characteristics of portfolios (2020–2024)

Four portfolios were constructed: High ESG (top 10 scores), Low ESG (bottom 10), Benchmark (S&P/BMV IPC), and Optimized ESG (quantitative selection with ESG constraints). The detailed annual composition of portfolios (2020–2024) is provided in Annex 1 (Supplementary Material). This framework enables tracking issuer turnover, ESG consistency, and selection logic in the Mexican market.

Table 3. Descriptive statistics of the key variables used for portfolio analysis (2020–2024)

|

Variable

|

Means

|

Median

|

Standard deviation

|

Minimum

|

Maximum

|

|

ESG

|

3.52

|

3.69

|

1.41

|

0.63

|

6.10

|

|

E

|

3.03

|

3.02

|

2.44

|

0.00

|

8.07

|

|

S

|

3.68

|

3.61

|

2.17

|

0.00

|

8.22

|

|

G

|

3.99

|

3.93

|

0.81

|

2.56

|

5.78

|

|

Volatility

|

0.11

|

0.09

|

0.06

|

0.03

|

0.38

|

|

Company size

|

16278.47

|

9979.26

|

22048.65

|

419.75

|

134325.67

|

|

WACC (%)

|

10.59

|

11.48

|

2.72

|

4.45

|

14.18

|

|

Market capitalization

|

10458.06

|

5074.00

|

15358.25

|

770.00

|

154890.00

|

|

D/E

|

1.95

|

0.92

|

3.30

|

0.03

|

17.75

|

Source: Own elaboration.

Table 3 summarizes key financial variables. ESG performance is moderate on average, but highly dispersed, especially in the environmental and social pillars, while governance remains relatively stable. Financial indicators reveal heterogeneous risk and leverage profiles, with higher financing costs than those observed in developed markets.

Overall, High ESG portfolios are dominated by larger firms with stronger governance and a lower leverage, while Low ESG portfolios consist mainly of smaller, riskier issuers. This structural contrast underscores how the firm size and governance shape the volatility and financing patterns analyzed in the following sections.

4.2. Results of the GARCH model

In order to evaluate the temporal stability of financial risk in the different ESG portfolios designed, a GARCH (1,1) model was implemented on the daily logarithmic returns of each portfolio for the period of 2020–2024.

The GARCH (1,1) assumptions were verified through Augmented Dickey–Fuller and Ljung–Box tests, confirming stationarity and residual adequacy for all portfolios. Parameter estimates revealed strong volatility persistence in High ESG portfolios (α + β ≈ 0.97), indicating prolonged risk clustering in the Mexican market (see Annexes 1 and 2).

Comparison of conditional volatility

Table 4 presents the average conditional volatility by portfolio. High ESG portfolios show higher volatility than Low and Optimized ESG portfolios, although this gap narrows after 2022.

Table 4. Average conditional volatility (%) by year and portfolio type

|

Years

|

Benchmark

|

High_ESG

|

Low_ESG

|

Optimized_ESG

|

|

2020

|

1.06

|

1.38

|

1.10

|

1.29

|

|

2021

|

1.07

|

1.38

|

1.08

|

1.22

|

|

2022

|

1.06

|

1.34

|

1.14

|

1.18

|

|

2023

|

1.07

|

1.35

|

1.09

|

1.23

|

|

2024

|

1.07

|

1.35

|

1.09

|

1.23

|

Source: Own elaboration.

This pattern reflects the early sensitivity of sustainable assets to systemic shocks (e.g., COVID-19) and a gradual stabilization over time, confirming persistent volatility clustering across ESG profiles.

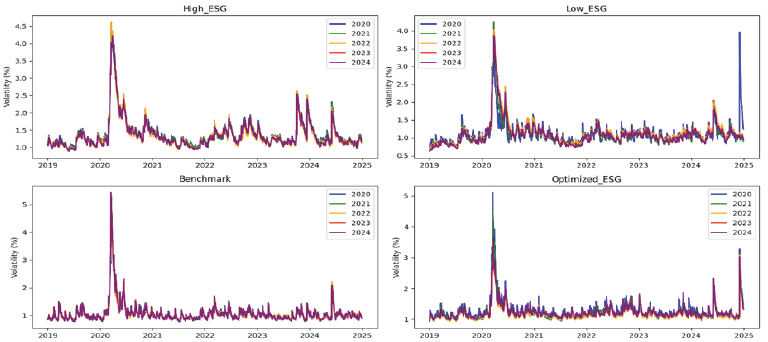

Evolution of Conditional Volatility

Figure 1 shows the evolution of conditional volatility estimated via GARCH (1,1) models for the four analyzed portfolios – High ESG, Low ESG, Benchmark, and Optimized ESG – during the years 2020–2024. Each subplot tracks daily volatility across the five years, enabling detection of patterns and anomalies by portfolio and year.

Figure 1. Estimated conditional volatility by portfolio for the period of 2020–2024

Source: Own elaboration based on GARCH estimates

Volatility spikes in 2020 and 2022 reflect periods of financial stress, which are most pronounced in the Benchmark and High ESG portfolios. In contrast, the Optimized ESG portfolio shows a lower dispersion and a faster risk convergence, indicating greater stability from its algorithmic, ESG-based design.

4.3. Results of the Random Forest model

A Random Forest Regressor modeled WACC by using ESG pillars, leverage, firm size, market value, and lagged WACC, capturing non-linear effects with cross-validated robustness.

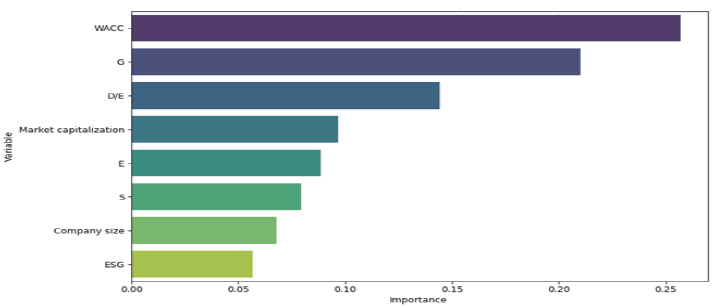

Variable Importance

Table 5 shows the relative importance of each predictor in estimating the WACC, which was calculated based on the reduction of the average mean squared error in the trees of the random forest.

Table 5. Importance of explanatory variables according to the Random Forest model

|

Variable

|

Importance

|

|

WACC

|

0.257

|

|

G

|

0.210

|

|

D/E

|

0.144

|

|

Market capitalization

|

0.097

|

|

E

|

0.088

|

|

S

|

0.079

|

|

Company size

|

0.068

|

|

ESG (Total)

|

0.057

|

Source: Own elaboration.

As observed in Figure 2, financial variables (especially the previous WACC, corporate governance, and leverage) have a predominant weight in predicting the cost of capital. However, ESG metrics, particularly the G component, also show a significant contribution, partially supporting their utility as a proxy for financial risk.

Figure 2. Relative importance of explanatory variables in the Random Forest model

Source: Own elaboration.

Visualization of the representative tree

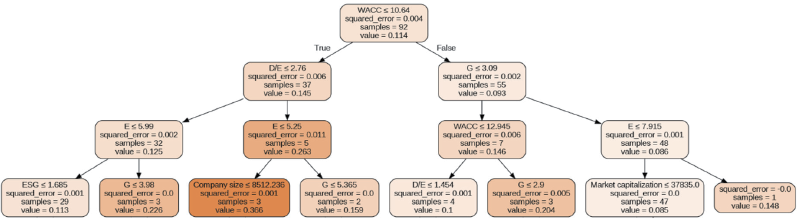

In addition to the importance analysis, a representative individual tree of the random forest is presented to visualize the segmentation logic (see Figure 3). The tree allows for the identification of critical thresholds of the most influential variables and decision paths that lead to different levels of estimated WACC.

Figure 3. Representative decision tree of the Random Forest model (max. depth = 5)

Source: Own elaboration.

Model fit was assessed through multiple metrics, showing strong performance, with an explained variance of 89.1%, low RMSE (0.0208), and acceptable MAPE (≈13%). These results confirm that the selected variables accurately estimate the cost of capital of the analyzed firms (see Annex 3).

4.4. Results of financial backtesting

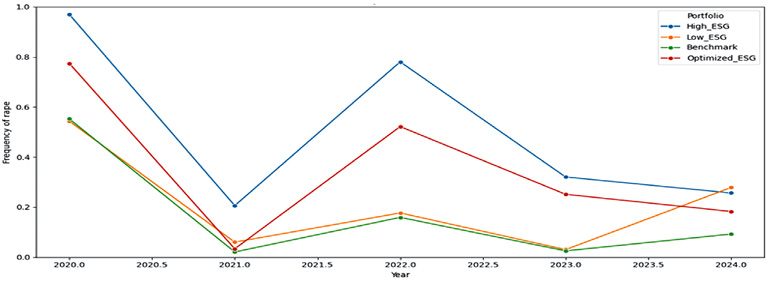

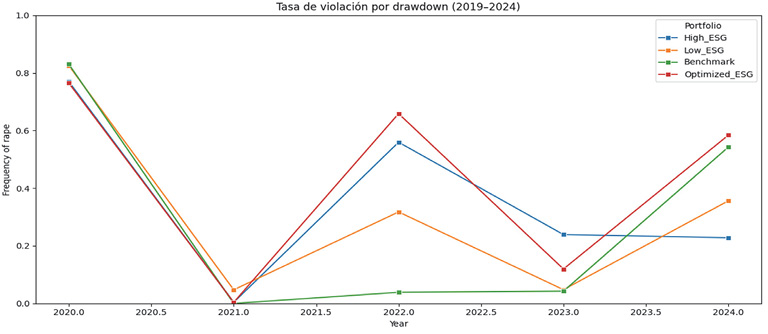

To test the robustness of ESG-based investment strategies, a Value-at-Risk (VaR) backtesting procedure following Kupiec (1995) and Christoffersen (1998) was applied. The analysis evaluates whether realized volatility and drawdowns exceed predefined limits through a binary violation system.

Frequency of violations by risk indicator

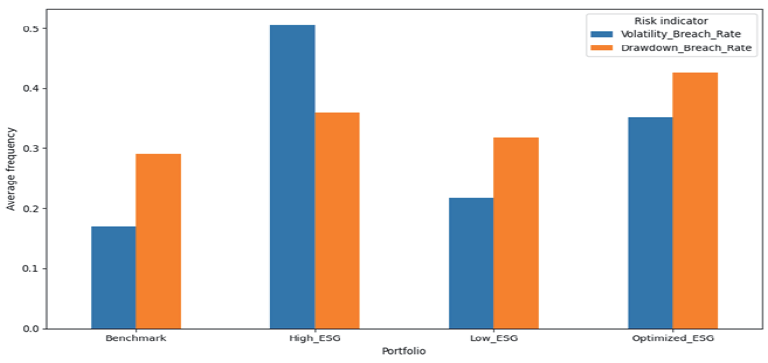

Table 6 summarizes the frequency of volatility and drawdown limit violations for the four portfolios (High ESG, Low ESG, Benchmark, and Optimized ESG) from 2020 to 2024. The High ESG portfolio records the highest violation rates for both volatility (50.7%) and drawdown (36.0%), followed by the Optimized ESG portfolio. In contrast, Benchmark and Low ESG portfolios show lower and more stable risk deviations.

Table 6. Average rate of violations by type of portfolio (2020–2024)

|

Portfolio

|

Violations due to Volatility

|

Violations due to Drawdown

|

|

Benchmark

|

0.1700

|

0.2908

|

|

High ESG

|

0.5066

|

0.3601

|

|

Low ESG

|

0.2177

|

0.3188

|

|

Optimized ESG

|

0.3526

|

0.4261

|

Source: Own elaboration.

Temporal evolution of violation rates

Figures 4 and 5 show the annual evolution of violation rates for each type of risk. Significant peaks are observed in the High ESG and Optimized ESG portfolios during the years 2020 and 2022, which is in line with periods of high global financial uncertainty. In contrast, the Benchmark and Low ESG portfolios maintain a more stable pattern, with a lower frequency of risk limit breaches.

Figure 4. Violation rate by volatility, 2020–2024

Source: Own elaboration.

Figure 5. Violation rate by drawdown, 2020–2024

Source: Own elaboration.

Aggregate Comparison between Portfolios

Figure 6 summarizes the average violation rates per portfolio. The Benchmark portfolio is positioned as the most stable, followed by the Low ESG portfolio. On the other hand, the High ESG and Optimized ESG portfolios show higher risk exposure, especially in terms of conditional volatility.

Figure 6. Average violation rates by portfolio type

Source: Own elaboration.

Statistical Evaluation of Control Quality

Finally, binomial tests were applied to assess whether the frequency of violations exceeded the expected 5% threshold under the null hypothesis of adequate risk control. The p-values reported in Annex 4 confirm that, in several cases, portfolios failed to maintain risk levels within the expected limits (p < 0.05).

Findings indicate that while ESG strategies enhance sustainability, their risk control depends on the portfolio design. Governance (G), leverage (D/E), and lagged WACC dominate capital cost prediction, supporting hybrid models like the Optimized ESG portfolio despite the persistent drawdown risk.

These results align only partly with prior literature. The higher volatility and breaches in High ESG portfolios mirror the findings of Alvarez-Perez et al. (2024) for Latin America, where sustainability indices do not consistently outperform the benchmarks. By contrast, they diverge from the European evidence of Gianfrate et al. (2024) and Siddiqui et al. (2024), which associates ESG integration with a lower systemic risk and a stronger firm value. The central role of governance and leverage in explaining WACC echoes Ramirez et al. (2022) for Latin America and Kim & Li (2021) globally, underscoring that institutional quality and firm fundamentals remain decisive. Overall, ESG effects in emerging markets appear context-dependent, shaped by the market maturity and regulatory depth. Comparable evidence in Asia shows mixed effects: while ESG performance reduces volatility in China and Indonesia (Kurniawan & Husodo, 2023; Liu et al., 2023), studies in India report persistent vulnerabilities during crises (Sharma et al., 2025)

5. Discussion

A central finding is the preeminence of governance (G) over aggregate ESG scores in explaining the cost of capital (WACC). This aligns with Ramirez et al. (2022) for Latin America, identifying governance as the most robust factor in reducing financing costs, and with Kim & Li (2021), globally, who show that the institutional quality and corporate control mechanisms weigh more heavily than environmental or social dimensions. In emerging markets, where WACC reflects creditors’ and investors’ perceptions of risk, transparency, board strength, and shareholder protection serve as clearer signals of stability than heterogeneous environmental or social metrics.

For Mexico, the implications are threefold. Investors should integrate ESG cautiously, by prioritizing governance and financial fundamentals over aggregated sustainability scores. Regulators must advance toward EU-style frameworks – such as the Taxonomy and SFDR – to improve the quality and comparability of ESG disclosure. Issuing firms, meanwhile, can reduce financing costs and attract capital more immediately through governance improvements, even in the absence of fully consolidated environmental or social metrics.

By contrast, the European Union illustrates a virtuous cycle between regulation, transparency, and resilience. Standardized metrics and ESMA supervision have enabled sustainable portfolios to capture growing investment flows while benefiting from lower debt costs and enhanced stability during crises (Cauthorn et al., 2023). The comparison highlights that the financial effects of ESG are not universal, but highly dependent on the institutional and regulatory quality.

However, the high volatility observed in ESG portfolios reveals structural and behavioral mechanisms beyond firm fundamentals. In Mexico’s relatively shallow capital market, ESG-labeled assets remain concentrated in few large issuers, generating sectoral clustering and limited diversification. Additionally, inconsistent disclosure and investor herding around sustainability narratives amplify short-term fluctuations, especially during global uncertainty episodes. These factors explain why volatility persistence remains strong despite optimization, indicating that ESG signals have not yet been fully internalized by the market. Over time, improved data standardization and broader participation could reduce this structural fragility and align Mexican ESG portfolios with the stability patterns observed in more mature economies.

This study faces certain limitations. The sample of 35 S&P/BMV IPC firms excludes medium-sized issuers, thereby limiting generalization. Dependence on Refinitiv ESG scores may introduce measurement bias, and the lack of sectoral or dynamic portfolios restricts cross-industry comparison. Future research should broaden the coverage, contrast multiple ESG databases, and test Sectoral and Rolling ESG configurations with the objective to capture heterogeneity and temporal dynamics in emerging markets.

In the Mexican context, ESG integration yields partial benefits shaped by governance and institutional quality. These findings do not invalidate ESG but highlight the need for hybrid approaches that combine sustainability metrics with robust financial fundamentals and stronger regulation so that to reproduce the successful outcomes observed in the European Union.

6. Conclusions

The results show that integration of ESG criteria into Mexican financial portfolios produces relevant but uneven effects on the risk, return, and cost of capital. High ESG portfolios display a greater systemic risk exposure, which is reflected in elevated conditional volatility and frequent backtesting breaches, suggesting that ESG commitment alone does not guarantee lower risk in emerging markets.

Random Forest analysis confirms that financial fundamentals – particularly lagged WACC, leverage (D/E), and governance (G) – are stronger determinants of capital costs than aggregate ESG scores. The Optimized ESG portfolio, however, demonstrates relative advantages in volatility control and balance between risk and sustainability, supporting hybrid approaches that combine quantitative methods with ESG constraints.

Despite its contributions, this study faces limitations: the sample is restricted to 35 S&P/BMV IPC firms, whereas the reliance on the Refinitiv scores may introduce bias, and the absence of sectoral or dynamic portfolios constrains heterogeneity analysis. These caveats nonetheless highlight avenues for future research and have clear implications: investors should integrate ESG cautiously alongside the financial fundamentals; regulators must strengthen the disclosure standards and market depth; and firms should prioritize governance and leverage management in order to reduce capital costs.

For investors, a few practical lessons emerge: (i) prioritize governance and leverage indicators over aggregate ESG ratings when selecting firms, as these directly affect the financing conditions; (ii) favor diversified, algorithmically optimized ESG portfolios rather than purely score-based ones in order to mitigate concentration and volatility risks; (iii) monitor consistency and transparency in ESG reporting as a signal of the risk management quality; and (iv) integrate the scenario analysis and backtesting so that to evaluate portfolio resilience under market shocks.

At the regulatory level, stronger disclosure standards and harmonized ESG taxonomies are needed to improve comparability and data reliability. For firms, strengthening of corporate governance and financial discipline remains the most direct path to lower capital costs and sustainable investor confidence.

References

Agarwal, S., & Muppalaneni, N. B. (2022). Portfolio optimization in stocks using mean–variance optimization and the efficient frontier. International Journal of Information Technology, 14(6), 2917–2926. https://doi.org/10.1007/s41870-022-01052-2

Agliardi, E., Alexopoulos, T., & Karvelas, K. (2023). The environmental pillar of ESG and financial performance: A portfolio analysis. Energy Economics, 120, 106598. https://doi.org/10.1016/j.eneco.2023.106598

Al Amosh, H. (2024). Exchange Rate Volatility and ESG Performance: An International Empirical Analysis. Journal of Corporate Accounting & Finance. https://doi.org/10.1002/jcaf.22774

Alessi, L., & Battiston, S. (2022). Two sides of the same coin: Green Taxonomy alignment versus transition risk in financial portfolios. International Review of Financial Analysis, 84, 102319. https://doi.org/10.1016/j.irfa.2022.102319

Alvarez-Perez, H., Diaz-Crespo, R., & Gutierrez-Fernandez, L. (2024). ESG investing versus the market: returns and risk analysis and portfolio diversification in Latin-America. Academia Revista Latinoamericana de Administración, 37(1), 78–100. https://doi.org/10.1108/ARLA-02-2023-0033

Alves, C. F., & Meneses, L. L. (2024). ESG scores and debt costs: Exploring indebtedness, agency costs, and financial system impact. International Review of Financial Analysis, 94, 103240. https://doi.org/10.1016/j.irfa.2024.103240

Arévalo, G., González, M., Guzmán, A., & Trujillo, M.-A. (2024). The value effect of sustainability: evidence from Latin American ESG bond market. Journal of Sustainable Finance & Investment, 14(3), 516–537. https://doi.org/10.1080/20430795.2024.2344527

Beloskar, V. D., & Nageswara Rao, S. V. D. (2024). Screening activity matters: Evidence from ESG portfolio performance from an emerging market. International Journal of Finance & Economics, 29(3), 2593–2619. https://doi.org/10.1002/ijfe.2798

Beloskar, V. D., & Rao, S. V. D. N. (2022). Did ESG Save the Day? Evidence From India During the COVID-19 Crisis. Asia-Pacific Financial Markets. https://doi.org/10.1007/s10690-022-09369-5

Billio, M., Costola, M., Hristova, I., Latino, C., & Pelizzon, L. (2024). Sustainable Finance: A Journey Toward ESG and Climate Risk. International Review of Environmental and Resource Economics, 18(1–2), 1–75. https://doi.org/10.1561/101.00000156

Bilyay-Erdogan, S., & Öztürkkal, B. (2023). The Role of Environmental, Social, Governance (ESG) Practices and Ownership on Firm Performance in Emerging Markets. Emerging Markets Finance and Trade, 59(12), 3776–3797. https://doi.org/10.1080/1540496X.2023.2223930

Breiman, L. (2001). Random Forests. Machine Learning, 45(1), 5–32. https://doi.org/10.1023/A:1010933404324

Cankaya, S., & Naeem, N. (2022). Does ESG performance affect the financial performance of environmentally sensitive industries A comparison between emerging and developed markets. Pressacademia, 14(1), 135–136. https://doi.org/10.17261/Pressacademia.2021.1509

Cauthorn, T., Klein, C., Remme, L., & Zwergel, B. (2023). Portfolio benefits of taxonomy orientated and renewable European electric utilities. Journal of Asset Management, 24(7), 558–571. https://doi.org/10.1057/s41260-023-00325-0

Christoffersen, P. F. (1998). Evaluating Interval Forecasts. International Economic Review, 39(4), 841. https://doi.org/10.2307/2527341

Dahlquist, M., & Ibert, M. (2024). Equity Return Expectations and Portfolios: Evidence from Large Asset Managers. The Review of Financial Studies, 37(6), 1887–1928. https://doi.org/10.1093/rfs/hhae008

De Rosa, M., Gainsford, K., Pallonetto, F., & Finn, D. P. (2022). Diversification, concentration and renewability of the energy supply in the European Union. Energy, 253, 124097. https://doi.org/10.1016/j.energy.2022.124097

Dwomor, E., & Mensah, E. (2024). THE ROLE OF COST OF CAPITAL IN THE LINK BETWEEN ESG REPORTING AND FIRM PERFORMANCE. Jurnal Akuntansi Dan Keuangan Indonesia, 21(2), 241–259. https://doi.org/10.21002/jaki.2024.11

Franc-Dąbrowska, J., Mądra-Sawicka, M., & Milewska, A. (2021). Energy Sector Risk and Cost of Capital Assessment—Companies and Investors Perspective. Energies, 14(6), 1613. https://doi.org/10.3390/en14061613

Freeman, R. E. (2010). Strategic Management: A Stakeholder Approach. Cambridge University Press. https://doi.org/10.1017/CBO9781139192675

Gangwani, M., & Kashiramka, S. (2024). Does ESG performance impact value and risk‐taking by commercial banks? Evidence from emerging market economies. Business Strategy and the Environment, 33(7), 7562–7589. https://doi.org/10.1002/bse.3882

Garcia-Bernabeu, A., Hilario-Caballero, A., Tardella, F., & Pla-Santamaria, D. (2024). ESG integration in portfolio selection: A robust preference-based multicriteria approach. Operations Research Perspectives, 12, 100305. https://doi.org/10.1016/j.orp.2024.100305

Garrido-Merchán, E. C., González Piris, G., & Coronado Vaca, M. (2023). Bayesian optimization of ESG (Environmental Social Governance) financial investments. Environmental Research Communications, 5(5), 055003. https://doi.org/10.1088/2515-7620/acd0f8

Gianfrate, G., Rubin, M., Ruzzi, D., & van Dijk, M. (2024). On the resilience of ESG firms during the COVID-19 crisis: evidence across countries and asset classes. Journal of International Business Studies, 55(8), 1069–1084. https://doi.org/10.1057/s41267-024-00718-2

Gupta, A., & Sharma, A. K. (2023). The role of institutional and governance factors in <scp>public–private</scp> partnerships infrastructure investments in emerging economies. Journal of Public Affairs, 23(4). https://doi.org/10.1002/pa.2874

Gupta, H., & Chaudhary, R. (2023). An Analysis of Volatility and Risk-Adjusted Returns of ESG Indices in Developed and Emerging Economies. Risks, 11(10), 182. https://doi.org/10.3390/risks11100182

Johnson, R. (2020). The link between environmental, social and corporate governance disclosure and the cost of capital in South Africa. Journal of Economic and Financial Sciences, 13(1). https://doi.org/10.4102/jef.v13i1.543

Kaminskyi, A., Osetskyi, V., Almeida, N., & Nehrey, M. (2025). Investigating the Relationship Between ESG Performance and Financial Performance During the COVID-19 Pandemic: Evidence from the Hotel Industry. Journal of Risk and Financial Management, 18(3), 126. https://doi.org/10.3390/jrfm18030126

Kartikasary, M., Paramastri Hayuning Adi, M., Marojahan Sitinjak, M., Hardiyansyah, & Yolanda Sari, D. (2023). Environmental, Social and Governance (ESG) Report Quality and Firm Value in Southeast Asia. E3S Web of Conferences, 426, 02087. https://doi.org/10.1051/e3sconf/202342602087

Kim, S., & Li, Z. (Frank). (2021). Understanding the Impact of ESG Practices in Corporate Finance. Sustainability, 13(7), 3746. https://doi.org/10.3390/su13073746

Kupiec, P. H. (1995). Techniques for verifying the accuracy of risk measurement models (Vol. 95, Issue 24). Division of Research and Statistics, Division of Monetary Affairs, Federal ….

Kurniawan, M., & Husodo, Z. A. (2023). The effect of ESG performance on stock price volatility: A study of emerging markets in Asia. BISMA (Bisnis Dan Manajemen), 28–46. https://doi.org/10.26740/bisma.v16n1.p28-46

Lerskullawat, P., & Ungphakorn, T. (2024). ESG Performance, Ownership Structure and Firm Value: Evidence from ASEAN-5. ABAC Journal, 44(4). https://doi.org/10.59865/abacj.2024.63

Liu, D., Gu, K., & Hu, W. (2023). ESG performance and stock idiosyncratic volatility. Finance Research Letters, 58, 104393. https://doi.org/10.1016/j.frl.2023.104393

Markowitz, H. (1952). Modern portfolio theory. Journal of Finance, 7(11), 77–91.

Marti, E., Fuchs, M., DesJardine, M. R., Slager, R., & Gond, J. (2024). The Impact of Sustainable Investing: A Multidisciplinary Review. Journal of Management Studies, 61(5), 2181–2211. https://doi.org/10.1111/joms.12957

Martinez-Meyers, S., Ferrero-Ferrero, I., & Muñoz-Torres, M. J. (2024). The European sustainable finance disclosure regulation (SFDR) and its influence on ESG performance and risk in the fund industry from a multi-regional perspective. Journal of Financial Reporting and Accounting. https://doi.org/10.1108/JFRA-03-2024-0150

Peliu, S.-A. (2024). Exploring the impact of ESG factors on corporate risk: empirical evidence for New York Stock Exchange listed companies. Future Business Journal, 10(1), 92. https://doi.org/10.1186/s43093-024-00378-6

Priem, R., & Gabellone, A. (2024). The impact of a firm’s ESG score on its cost of capital: can a high ESG score serve as a substitute for a weaker legal environment. Sustainability Accounting, Management and Policy Journal, 15(3), 676–703. https://doi.org/10.1108/SAMPJ-05-2023-0254

Ramirez, A. G., Monsalve, J., González-Ruiz, J. D., Almonacid, P., & Peña, A. (2022). Relationship between the Cost of Capital and Environmental, Social, and Governance Scores: Evidence from Latin America. Sustainability, 14(9), 5012. https://doi.org/10.3390/su14095012

Ravina, E., & Persico, N. (2025). ESG Choice with Polarized Investors. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.5086547

Rossignolo, A. F. (2024). Basel IV and the structural relationship between SA and IMA. Revista Mexicana de Economía y Finanzas, 19(2), 1–37. https://doi.org/10.21919/remef.v19i2.991

Sautner, Z., Yu, J., Zhong, R., & Zhou, X. (2022). The EU Taxonomy and the Syndicated Loan Market. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.4058961

Sharma, S., Aggarwal, V., Reepu, & Mehta, G. K. (2025). ESG performance and corporate volatility: an empirical exploration in an emerging economy. International Journal of Social Economics, 52(3), 467–483. https://doi.org/10.1108/IJSE-02-2024-0113

Sharpe, W. F. (1964). CAPITAL ASSET PRICES: A THEORY OF MARKET EQUILIBRIUM UNDER CONDITIONS OF RISK*. The Journal of Finance, 19(3), 425–442. https://doi.org/10.1111/j.1540-6261.1964.tb02865.x

Siddiqui, O., Khan, N., & Sohail, M. K. (2024). The Three ESG Pillars, Firm Value and Financial Performance: A Comparison of Developed and Emerging Markets. NICE Research Journal, 17(2), 1–14. https://doi.org/10.51239/nrjss.v17i2.446

Tsay, R. S. (2010). Analysis of financial time series (3ra Edition). John wiley & sons.

Vasiliauskaitė, D. (2004). Optimalaus vertybinių popierių portfelio sudarymo ypatumai. Ekonomika, 67(2). https://doi.org/10.15388/Ekon.2004.17387

Vivek, S. K. (2024). The Impact of ESG Investing on Portfolio Performance: An Empirical Study of Emerging Markets. Journal of Informatics Education and Research, 4(3). https://doi.org/10.52783/jier.v4i3.1916

Annex 1

Stationarity tests (ADF) and adequacy (Ljung-Box) for portfolio returns by year

|

Year

|

Portfolio

|

ADF p-value

|

Ljung-Box p-value

|

|

2020

|

High_ESG

|

0.0000

|

0.0853**

|

|

Low_ESG

|

0.0000

|

0.1876***

|

|

Benchmark

|

0.0000

|

0.3818***

|

|

Optimized_ESG

|

0.0000

|

0.1608***

|

|

2021

|

High_ESG

|

0.0000

|

0.033*

|

|

Low_ESG

|

0.0000

|

0.1331***

|

|

Benchmark

|

0.0000

|

0.4271***

|

|

Optimized_ESG

|

0.0000

|

0.0966**

|

|

2022

|

High_ESG

|

0.0000

|

0.1073***

|

|

Low_ESG

|

0.0000

|

0.031*

|

|

Benchmark

|

0.0000

|

0.4495***

|

|

Optimized_ESG

|

0.0000

|

0.5201***

|

|

2023

|

High_ESG

|

0.0000

|

0.0613**

|

|

Low_ESG

|

0.0000

|

0.132***

|

|

Benchmark

|

0.0000

|

0.4271***

|

|

Optimized_ESG

|

0.0000

|

0.2874***

|

|

2024

|

High_ESG

|

0.0000

|

0.0613**

|

|

Low_ESG

|

0.0000

|

0.132***

|

|

Benchmark

|

0.0000

|

0.4271***

|

|

Optimized_ESG

|

0.0000

|

0.2874***

|

Note: Significance levels refer to Ljung-Box test for residual autocorrelation. *** p > 0.10; ** 0.05 < p ≤ 0.10; * 0.01 < p ≤ 0.05; blank if p ≤ 0.01.

Annex 2

Estimated parameters of the GARCH model by year and portfolio type

|

Year

|

Portfolio

|

mu

|

omega

|

alpha[1]

|

beta[1]

|

|

2020

|

High_ESG

|

0.0380

|

0.0559

|

0.0633

|

0.9090

|

|

Low_ESG

|

-0.0047

|

0.1104

|

0.1220

|

0.7953

|

|

Benchmark

|

0.0329

|

0.0981

|

0.1073

|

0.8055

|

|

Optimized_ESG

|

0.0278

|

0.1708

|

0.0887

|

0.8110

|

|

2021

|

High_ESG

|

0.0401

|

0.0567

|

0.0613

|

0.9105

|

|

Low_ESG

|

0.0196

|

0.0490

|

0.0859

|

0.8733

|

|

Benchmark

|

0.0335

|

0.0991

|

0.1100

|

0.8040

|

|

Optimized_ESG

|

0.0257

|

0.0987

|

0.0694

|

0.8664

|

|

2022

|

High_ESG

|

0.0435

|

0.0615

|

0.0689

|

0.8982

|

|

Low_ESG

|

0.0258

|

0.0304

|

0.0634

|

0.9141

|

|

Benchmark

|

0.0361

|

0.1121

|

0.1085

|

0.7925

|

|

Optimized_ESG

|

0.0259

|

0.1502

|

0.0795

|

0.8162

|

|

2023

|

High_ESG

|

0.0495

|

0.0485

|

0.0624

|

0.9124

|

|

Low_ESG

|

0.0193

|

0.0282

|

0.0666

|

0.9105

|

|

Benchmark

|

0.0335

|

0.0991

|

0.1100

|

0.8040

|

|

Optimized_ESG

|

0.0294

|

0.1575

|

0.0764

|

0.8218

|

|

2024

|

High_ESG

|

0.0495

|

0.0485

|

0.0624

|

0.9124

|

|

Low_ESG

|

0.0193

|

0.0282

|

0.0666

|

0.9105

|

|

Benchmark

|

0.0335

|

0.0991

|

0.1100

|

0.8040

|

|

Optimized_ESG

|

0.0294

|

0.1575

|

0.0764

|

0.8218

|

Annex 3

Validation metrics of the Random Forest model

|

Metric

|

Value

|

|

RMSE

|

0.0208

|

|

MAE

|

0.0149

|

|

MAPE (%)

|

13.24

|

|

MedAE

|

0.0091

|

|

Explained variance

|

0.8912

|

|

OOB Score

|

0.1041

|

Annex 4

Binomial tests of volatility violation (2020–2024)

|

Year

|

Portfolio

|

p-value

|

Interpretation

|

|

2020

|

High ESG

|

0.0000

|

Significant violation

|

|

Low ESG

|

0.0000

|

Significant violation

|

|

Benchmark

|

0.0000

|

Significant violation

|

|

Optimized ESG

|

0.0000

|

Significant violation

|

|

2021

|

High ESG

|

0.0000

|

Significant violation

|

|

Low ESG

|

0.2812

|

No evidence of violation

|

|

Benchmark

|

0.9958

|

No evidence of violation

|

|

Optimized ESG

|

0.9384

|

No evidence of violation

|

|

2022

|

All portfolios

|

0.0000

|

Significant violation

|

|

2023

|

High ESG

|

0.0000

|

Significant violation

|

|

Low ESG

|

0.9704

|

No evidence of violation

|

|

Benchmark

|

0.9878

|

No evidence of violation

|

|

Optimized ESG

|

0.0000

|

Significant violation

|

|

2024

|

High ESG

|

0.0000

|

Significant violation

|

|

Low ESG

|

0.0000

|

Significant violation

|

|

Benchmark

|

0.0043

|

Significant violation

|

|

Optimized ESG

|

0.0000

|

Significant violation

|