Knygotyra ISSN 0204–2061 eISSN 2345-0053

2020, vol. 75, pp. 17–37 DOI: https://doi.org/10.15388/Knygotyra.2020.74.58

Publishing under COVID-19 in Small Book Markets: An Interim Report

Miha Kovač

Department for Library and Information Science and Book Studies,

Faculty of Arts, University of Ljubljana

Aškerčeva cesta 2, 1000 Ljubljana, Slovėnija

Email Mihael.Kovac@ff.uni-lj.si

Arūnas Gudinavičius

Vilniaus universiteto Komunikacijos fakulteto

Skaitmeninių kultūrų ir komunikacijos katedra

Universiteto g. 3, LT-0513 Vilnius, Lietuva

El. paštas arunas.gudinavicius@kf.vu.lt

Abstract. The paper is based on a survey that was conducted among publishers in Slovakia, Iceland, Lithuania and Slovenia in May and August 2020. The paper looks at how publishers reacted to the COVID-19 crisis in their respective countries, what was its impact on book sales and how did the publishers adapt the production of new books to changed circumstances. In addition, the paper analyses changed attitudes of publishers towards e-books and other digital book formats that become more popular in lockdown times. The research revealed that COVID-19 lockdowns resulted in decreased sales of printed books in all four small book markets. However, sales of e-books and audiobooks slightly increased during that period. This increase in digital sales did not contribute significantly to overall results of book industries due to its small market share in all four countries.

Keywords: publishing, small book markets, COVID-19, pandemic.

Leidyba COVID-19 pandemijos metu mažose knygų rinkose: tarpinė ataskaita

Santrauka. Straipsnyje pristatomas tyrimas remiasi 2020 m. gegužės ir rugpjūčio mėnesiais atlikta Slovakijos, Islandijos, Lietuvos ir Slovėnijos leidėjų apklausa. Straipsnyje aptariama, kaip skirtingi leidėjai reagavo į COVID-19 krizę savo šalyse, koks pastebėtas krizės poveikis knygų pardavimams ir kaip leidėjai prisitaikė prie pasikeitusių aplinkybių leisdami naujas knygas. Straipsnyje taip pat tiriamas pasikeitęs požiūris į elektronines knygas ir kitus skaitmeninius knygų formatus, kurių populiarumas karantino sąlygomis išaugo. Tyrimas parodė, kad COVID-19 ribojimai neigiamai paveikė spausdintų knygų pardavimus visose keturiose nagrinėtose knygų rinkose. Taip pat nustatyta, kad tuo pačiu metu elektroninių ir audioknygų pardavimai nežymiai padidėjo. Skaitmeninių knygų pardavimų nežymus padidėjimas reikšmingai neprisidėjo prie bendrų leidybos industrijų pelno rezultatų dėl savo smulkios dalies visose keturių šalių knygų rinkose.

Reikšminiai žodžiai: leidyba, mažos knygų rinkos, COVID-19, pandemija.

Received: 2020 10 23. Accepted: 2020 11 03

Copyright © 2020 Miha Kovač, Arūnas Gudinavičius. Published by Vilnius University Press. This is an Open Access journal distributed under the terms of the Creative Commons Attribution Licence, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

Introduction

We live in a world in which it is – mildly put – exciting to be a publisher. In the last two decades, e-books, audiobooks and online bookselling, in combination with omnipresent screen technologies, transformed consumer behaviour all around the globe and decreased sales of the majority of traditional book publishers. After years of decline, when the book market seemed to start stabilising in 2019, in early spring 2020 COVID-19 epidemics locked down the majority of brick and mortal bookstores and other sales points for printed books all around Europe. Consequently, almost all publishers faced a significant drop in sales, and traditional bookstores that were closed experienced the two worst months ever as their sales dropped to zero. Online sales thrived, but they were far from being able to substitute the drop in sales in physical retail.

All these changes were felt differently in digitally less developed book markets with a smaller number of native speakers, where the digital transformation took a slower pace than in digitally more developed and bigger markets, such as Sweden, Denmark and Norway, not to mention much the bigger markets such as those that exist in China, USA and in Spanish-speaking countries.

For the last few years, a small group of researchers is trying to understand the logic of structural changes that took place in small book markets as they exist in the Baltics, Scandinavia, South-Eastern Europe, and in many other parts of the world (in this context, we define small book markets as markets either with less than 10 million native speakers or with inhabitants that share the same language with bigger communities but are culturally specific). We do not see our efforts just as an academic exercise: we aim to produce data and an analysis that will be useful both for publishers and policy-makers in the field of literacy and culture.

This paper should be understood as a kind of intermediate report on COVID-19 and publishing: in the time of its publication, in Europe a second wave of the pandemic just started to take place. As of November 2020, in some of the countries (such as Slovenia) there was a lockdown similar as in the first wave, whilst in other EU countries, there was no absolute lock-down, but there were limitations on the number of customers that were allowed to be simultaneously in stores. In addition, shop visits were less pleasant than before, as wearing masks became compulsory almost everywhere in Europe. Consequently, in autumn 2020 all major European book fairs and book festivals migrated from brick and mortar to digital platforms. The second COVID-19 wave should therefore be seen as another push for digital transformation of publishing and bookselling. As the reviewing process of this paper was concluded in early November 2020, these changes were still in full swing and could not be fully assessed. The authors plan to analyse them in the first half of 2020, when yearly results of book industries (and country economic statistics) will be available and the end of the pandemic will be easier to predict.

Literature review

Just a few already published research results on publishing under COVID-19 were found on August 2020 and most of them were related to journal publishing.

Scholarly journals editors1 noticed that in the pandemic period they faced a strong growth in article submissions, and assumed that it could be associated with the relative ease of which writing up manuscripts for publication can be accomplished when working from home for some individuals. Such circumstances were a challenge especially for women editors, having one’s family at home all day, every day2. In biomedicine, due to obvious reasons, the median time from the reception to acceptance of a journal article from the PubMed database was 6 days, when the typical median is 100 days3. Preprints have become increasingly popular and influential, editors had to rethink workflows and “paradoxically—found a need to slow down” in order to avoid damaging consequences of rushed research, writing, and peer review4. A study5 of 14 medical journals’ publication processes assessed 669 articles and found that the COVID-19 pandemic has propelled the journal editors to drastically speed up (on an average by 49%) their publication process. This quick publishing resulted in some doubts on publication ethics and the quality of scientific output – there were examples when articles were published, but were quickly retracted with no clear cause of retraction6.

Various consequences appeared in trade book publishing. According to the Global Book Publishers Market 2020–2030 report7 the global book publishers market is expected to decline by -7.5% (from $92.8 billion in 2019 to $85.9 billion in 2020), the main reason for it being the COVID-19 outbreak.

Maria Pallante, CEO of the Association of American Publishers mentioned8 that between January and April 2020, print was still fairly strong in USA, and the biggest bump and decline was in April – It took a nearly 11% decline and hit in print sales.

In China a number of publishers opened up their digital resources for the public, published over 100 books and articles, and licensed over 40 titles on COVID-19 prevention in 27 languages9. According to an OpenBook (http://www.openbook.com.cn) analysis on the China book retail market in the first quarter of 2020, retail sales decreased by 15.93% over the same quarter of 2019, online channels increased by 3.02%, and physical bookstores dropped by 54.79%. As reported in Publishing Perspectives10 on July 17 2020, China’s book retail market was down for 9.29% in first half of 2020 in comparison with first half of 2019, but physical retail was down for 47.36% in this period.

Samuel Kolawole, chair of the African Publishers Network, suggested11 that the fact that most of books in Africa are print-based, it was the reason why the pandemic affected African publishers probably more than publishers in most other countries and continents.

The International Publishers Association created a regularly updated web page with COVID-19 related information on government support gathered from publishers’ associations and publishers (https://www.internationalpublishers.org/covid-reaction/168-covid-19/966-publishers-act-amid-covid19-pandemic).

In summer 2020, the Federation of European Publishers issued a report on the consequences of COVID-19 pandemics on European book markets12. The report stated that in spring 2020, bookshops were closed in the majority of EU book markets; accordingly, their sales dropped between 75% and 95% in most of the countries between mid-March and mid-April 2020. Consequently, the publishing industry turnover dropped too: for example, in France, overall publishing sales were down by 66%, in Italy, one third of publishers that took place in the FEP survey reported a 70% loss of turnover, and in Germany, the entire value chain expected 500 million euros in losses per lockdown month. Similarly, in Spain, the value chain expected 200 million euros loses per lockdown month. Due to such financial pressures, many publishers postponed and cancelled publication of new titles: the FEP report estimates that in member states, publication of more than 20,000 new titles was cancelled or postponed because of the COVID-19 crisis, corresponding in almost 50 million copies of books less printed. In some countries and especially in bigger cities, some booksellers creatively linked online sales with home delivery to their customers. Nevertheless, their loses were still exorbitant: in Italy, for example, such creative booksellers suffered a loss of 71% of sales in comparison to 85% of losses in the sector overall.

Not surprisingly, online sales doubled or tripled: nevertheless, as most of the books in Europe are sold in brick and mortar stores, this escalating growth could not compensate the losses of the industry.

In a few countries that bookstores were not forced to close down, the drop in sales was lower but still significant as people avoided frequenting stores as often as in normal times: bookstore sales in Denmark and Estonia were down by 30%, in Finland and Latvia 40%, and in Norway, Sweden and the Netherlands around 30%. In all these countries, online sales of printed and e-books were up, but they could not compensate for the loss of brick and mortar sales.

When the shops reopened in June and May, a relatively fast recovery followed in all markets; nevertheless, in the majority of EU countries, overall sales in the first two quarters of 2020 were 10–20% below in comparison to the same period in 2019. In a few lucky exceptions such as Finland, Sweden and the Netherlands, sales were equal to the sales in the same period in previous year, predominantly thanks to book stores that remained opened and ebook and audio book subscription services that got additional impetus in lockdown times.

In short, at least in Europe, the winning publishing formula in the times of pandemics seems to be a combination of opened bookshops (with all limitations that come with precaution measures) and a heavily digitised book industry with subscription services.

In a survey below, we looked more closely at four small book markets in the European north and south.

An Overview of Publishing in Small Language Countries: Iceland, Lithuania, Slovakia, and Slovenia

In Iceland, a country with a 0.36 million population13, in 2015, 1,488 book titles in print were published (4.5 books per 1,000 inhabitants), book market revenue in 2016 was 2.55 billion Icelandic krónur (16.2 million euros)14. The Icelandic Publishers Association had 40 members in 202015.

Lithuania, a country with a 2.80 million population16, have registered over 500 publishers which published at least one book after 1990, but just 65 publishers published more than 10 book titles in 201517. The Lithuanian Publishers Association (Lietuvos leidėjų asociacija) had 47 members in 202018, so if we add members of the Lithuanian Association of Small and Medium Publishers and few independent publishers, we can count about 80 active publishers in the country. Lithuanian retail book sales were almost 32 million euros in 201819 and 3,075 new book titles were published in 2018 (1.1 published books per 1,000 inhabitants), with a total print run of 4,7 million copies20.

In Slovakia, a country with a 5.46 million population21, 9891 new titles were published in the Slovak language in 2018 (1,8 book titles per 1000 inhabitants) and the total turnover of the book market was around 110 million euros. The Slovak Publishers and Booksellers Association (Združenie vydavateľov a kníhkupcov Slovenskej republiky) had around 90 members, of which 65 were publishers, 17 booksellers, 6 distributors and 5 printers. Two biggest bookselling chains represented more than half of Slovak book sales (Pantha rei's turnover was 47 millon euros, and Martinus' 25.5 in 201822.

In Slovenia – a country with a 2.01 million population23, 3321 new titles in Slovene were published in 2018 (1.6 titles per 1000 inhabitants). The Slovene Association of Publishers and Booksellers (Zbornica založnikov in knjigotržcev) had around 80 members and 65 of them published more than 10 book titles in 2018. The turnover was 62 million euros and the biggest player on the market was the Mladinska knjiga Group. Its book publishing arm’s turnover was 12 million euros. It is estimated than in 2018, around 4,5 million books in Slovene were printed.

Methodology

We sent two sets of questionnaires to respondents. In the first one, we asked respondents about the estimated impact of the lockdown on their business till May 1st, and in the second, till August 1st. The first survey took place between the 15th and 29th of May, the second between the 15th and 29th of August 2020.

For the first survey, we received 77 answers from four countries in total: 16 answers from Iceland, 38 from Lithuania, 11 from Slovakia, 12 from Slovenia. For the second survey, we received answers just from Lithuania (39) and Slovenia (14).

In Lithuania and Slovenia, questionnaires were dispatched with the help of Lithuanian and Slovene publishers’ associations. In Lithuania, we added a few non-associated publishers, so the total list of 79 respondents (active publishers) was created. We reached publishers in Iceland and Slovakia with the help of the Federation of European publishers.

The questionnaire was composed from 5 main questions: 4 of them were dedicated to sales of all books, e-books, audiobooks and direct sales to libraries, and the fifth question was about employment policies in the lockdown period (from March to May 15th in the first survey, and to August 15th in the second survey). Ten more questions about the structure of the book market and about the respondent’s publishing houses were added in order to better understand the publishing industries of each country (number of employees, turnover, publishing segment, ownership of brick and mortar bookstores/vertical integration of the market, online sales and direct sales to libraries. The last two questions tackled e-book and audiobook sales and national and international subsidies). To the second survey, we added two questions about publishing plans for the rest of 2020 and for the following year. All these questions were close-ended, only the last question about the expectations of the impact of the pandemic on future publishing strategies was open-ended.

The survey was compiled using Google Forms in Lithuanian, Slovenian and English languages. SPSS was used in order to visualise data into tables and charts and calculate statistical significances.

Descriptive statistics of respondents and of peculiarities of their respective book markets

Number of full-time employees. On average, slightly more than half (55.8%) of publishers that responded to our first survey had less than 10 employees and 22.1% of the respondents had only one employee. The distribution of such publishing companies was similar in all four countries. Slovenia had the highest number of respondents with a larger number of employees: 3 of 12 answered they have between 10 and 30 employees and one respondent had more than 100 employees. In Lithuania, 7 of 38 respondents had between 10 and 30 employees and one more than a hundred.

The turnover of the company. Overall, in the first survey, every third respondent (29.9%) from all four countries declared the turnover between 100.000 and 500.000 euros and every fourth (26.0%) declared the turnover less than 50.000 euros. Lithuania had a largest proportion (16 of 38) of respondents with turnover less than 50.000 euros. Slovakia (6 of 11) and Slovenia (3 of 12) had the largest proportion of respondents with a turnover of more than 1 million euros.

Categories of published books. When asked about the categories in which they publish books, half (50.6%) of all respondents answered they are generalists and do all kinds of everything. This tendency was especially strong in Slovakia, where 9 of 11 respondents categorized themselves as generalists. Almost a quarter (10 of 38) of Lithuanian respondents declared themselves as adult non-fiction publishers and every third (5 of 16) of Icelandic respondents was a children’s book publisher. Half (6 of 12) of Slovene respondents considered themselves as generalists, two as children’s book publishers and two as adult non-fiction publishers.

Brick and mortar bookstores the publishers own (vertical integration). Slovenia can be described as a country with the most vertical integrated publishers – 5 of 12 respondents also own brick and mortar bookstores. In Lithuania, that is the case with 8 of 38 publishers. In both countries, two biggest publishers also own two biggest bookstore chains. In Iceland, there are 2 of 16 vertically integrated publishers/booksellers, and in Slovakia just one of 1.

Online sales. On average, more than half (57.1%) of the respondents from all four countries generated less than 30% of their income from online sales and 15.6% did not sell online at all (however, all Slovenian respondents did sell online). Every fourth (10 of 38) of Lithuanian respondents generated more than 50% income from online sales; in Slovenia and Slovakia there were no such respondents, in Iceland just 2 of 16.

Income from e-books. On average 62.3% of respondents from all four countries did not publish e-books. The highest e-book incomes were generated in Lithuania: 5 of 38 Lithuanian respondents generated more than 5% income from e-book sales, in Iceland 1 of 16, and in Slovakia and Slovenia there were no such respondents; 4 of 12 Slovenian and 5 of 11 Slovakian publishers generate up to 5% income from e-book sales.

Income from audiobooks. Just 18.2% of respondents from all four countries published audiobooks. The leader was Iceland, where 2 of 16 respondents generated more than 5% income from audiobooks, whilst the second was Lithuania with only 2 of 38 respondents generating more than 5% of their income with audiobooks. In Slovenia and Slovakia there were no respondents with more that 5% income from audiobooks. In Slovakia there were 3 out of 11 respondents with less than 5% income from audiobooks, and in Slovenia there was only one respondent that publishes audiobooks and earned less than 1% of its income through audiobook sales.

Direct sales to libraries. Almost 30 percent of respondents from all four countries did not sell books directly to libraries. About half of all respondents generated up to 10% and about every fifth generated more than 10% of income from direct sales to libraries.

The leader of direct sales to libraries was Slovenia, where 6 of 12 respondents generated more than 20% income from direct sales to libraries; 3 of 11 respondents from Slovakia generated more than 10% income via direct sales to libraries. The smallest number (5% or less) of income from direct sales to libraries goes to Lithuanian (17 of 38) and Icelandic respondents (7 of 16).

National and international subsidies. Respondents form Slovakia and Slovenia declared the lowest level of subsidies as the percentage of their turnover – 8 of 11 Slovakian and 8 of 12 Slovenian respondents reported not receiving any regular national subsidies. Respondents from Iceland and Lithuania were receiving subsidies more often, as just 5 of 16 respondents from Iceland and 11 from 38 respondents from Lithuania were not receivers of regular national subsidies. Similarly, none of the Slovakian respondents in Slovakia admitted to receive any international subsidies, while international subsidies seemed to be reaching Lithuania quite well – 14 of 38 respondents from Lithuania said they received international subsidies.

COVID-19 Impact on Four Markets

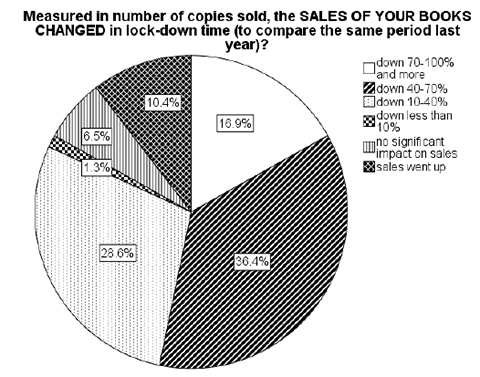

Sales of all books. In May 2020, sales of all books decreased in all four markets: 28.6% of 77 respondents answered that their sales were down 10–40%, 36.4% – were down 40–70%, 16.9% – were down 70–100%, and 1.3% – were down less than 10% (Fig. 1). Rather surprisingly, 6.5% of respondents answered that COVID-19 had no significant impact on sales and 10.4% of respondents reported increased sales.

Fig. 1. Change of sales of all books in Iceland, Lithuania, Slovakia and Slovenia, May 2020.

Regarding the impact of COVID-19, there are significant differences between the four countries. Iceland and Lithuania were the only two countries in which a small set of respondents reported increased sales (2 out of 16 and 6 out of 38 respondents accordingly) in May 2020 (Fig. 2). Two out of 11 Slovakian respondents and 3 out of 38 Lithuanian respondents reported no significant impact on changes during the lock-down.

As it seems, the most affected country was Slovenia, where more than half (6 out of 12) respondents reported sales down to 70–100%, five respondents reported 40–70% and one – 10–40% decrease of sales of all books. The least affected country was Lithuania, with only approx. two thirds of publishers (29 out of 38) reporting a decrease in sales.

It is worth noting that there was a correlation between the lockdown performance and size of publishing companies: only those Lithuanian (9 of 38), Slovenian (2 of 12) and Icelandic (2 of 16) that had less than 10 employees reported no significant impact on sales or even had increased sales during the first months of the lockdown.

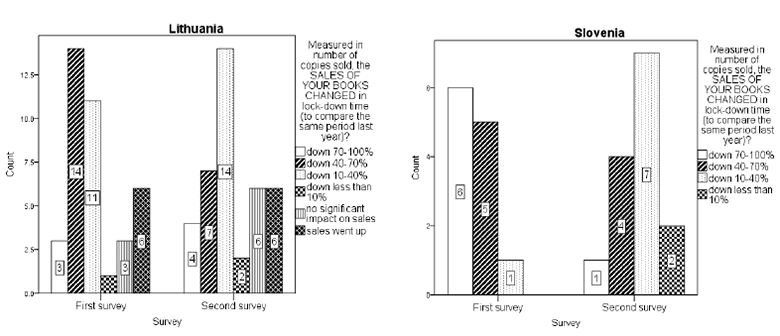

In August 2020 we again sent out a small survey about book sales in summer, but we got enough responses just from Lithuania and Slovenia. In the Lithuanian case, a Wilcoxon signed-ranks test indicated no significant differences in both survey answers (Z =-0.7, p=0.496). However, the situation changed significantly in Slovenia (Z =-2.6, p=0.008): the sales of all books improved during three summer months. In May, in terms of percentages, 11 of 12 respondents reported a 40–100% sales down and one a 10–40% down, but in August just 5 of 14 respondents reported 40–100% decreases in sales, seven reported 10–40% decreases, and two just less than a 10% decrease.

Fig. 2. Change of sales of all books in Lithuania and Slovenia in May and August 2020 (after three-month interval)

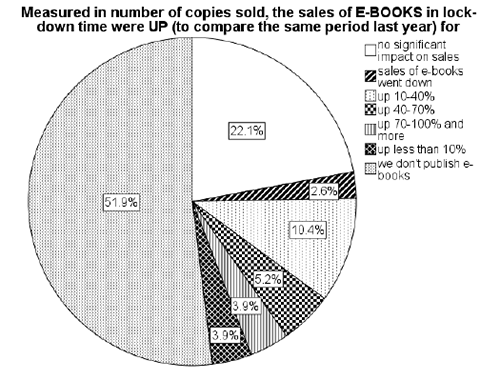

Sales of e-books. Just about half of the respondents (48.1%) publish e-books. It seems that the publishing of e-books depends on the population of a country – 44.7% of Lithuanian and 45.5% of Slovakian respondents do not publish e-books, while this number is higher in smaller countries – in Slovenia 58.3% of respondents do not publish e-books, and in Iceland – 68.8% (Fig. 3).

Fig. 3. Change of sales of e-books in Iceland, Lithuania, Slovakia and Slovenia in May 2020

Less affected from the lockdown in May 2020 were the Lithuanian publishers of e-books – 13 of 21 of respondents who publish e-books answered that no significant impact on sales was noticed, while 6 reported increased sales by up to 40% and two reported a decline; 3 of 5 respondents from Iceland reported no impact on sales, and 2 publishers reported a sales growth by 70–100%. The most positively affected was Slovakia, where all 6 e-book publishers reported increased sales by 10–70%, and Slovenia, where 2 of 5 e-book publishers reported a 10–40%, two – a 40–100% sales growth, while one declared no impact.

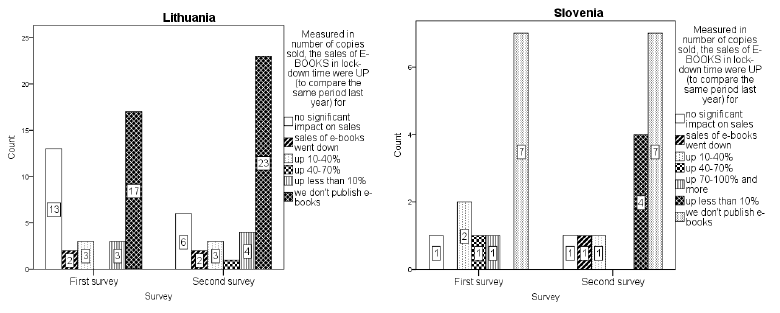

In Slovenia, no significant differences (Z =-1.6, p=0.250) on e-book sales was noticed in August 2020 to compare with May. However, the situation during the three months changed in Lithuania (Z =-2.1, p=0.039), as the number of respondents who reported no significant impact on e-book sales decreased, while the number of respondents who reported increased sales increased significantly (Fig. 4).

Fig. 4. Change of sales of e-books in Lithuania and Slovenia in May and August 2020 (after a three-month interval)

Sales of audiobooks. Of all, 79.2% (61 of 77) of all respondents answered they do not publish audiobooks. The largest number of respondents that publish also audiobooks was in Slovakia (4 of 11) and Iceland (5 of 16). In Lithuania, there were 6 audio publishers out of 38 respondents and Slovenia, just one publisher published audiobooks.

Most positively affected by the growth of audiobook sales in May 2020 was Iceland, where 2 publishers reported a 10–40%, and two – a 40–100% increase in sales, while one reported no significant increase. Two publishers from Slovakia reported a 40–100% increase and two publishers no impact. Quite similar answers came from Lithuania – two publishers reported 10–70% increases and four publishers felt no impact. In Slovenia, the one and only audio respondent reported a decline in sales of audiobooks.

Fig. 5. Change of sales of audiobooks in Iceland, Lithuania, Slovakia and Slovenia in May 2020

Due to the small number of audio publishers in Lithuania and Slovenia, we did not perform any statistical tests to compare the audio sales before and after lockdown in the two countries.

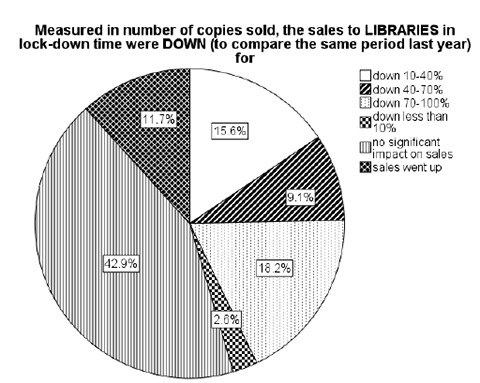

Sales to libraries. Overall, 42.9% (33 of 77) of publishers from all four countries reported no impact on sales to libraries in May 2020; 45.5% reported declines in library sales and 11.7% reported increased sales.

The most positively affected country was Lithuania, as 9 of 38 respondents declared increased sales to libraries, 3 respondents reported a decline in library sales, and the remaining ones (16) reported no significant impact. While 11 of 16 respondents from Iceland declared no significant change in library sales during the COVID-19 crisis, 5 respondents faced a decline in sales. Six of eleven respondents from Slovakia declared a decline on sales to libraries and the remaining 5 reported no impact. Most negatively affected was Slovenia, where 11 of 12 respondents reported a decline in library sales (6 of them even up to 70–100%), while just one reported no impact (Fig. 6).

Fig. 6. Change of sales to libraries in Iceland, Lithuania, Slovakia and Slovenia in May 2020

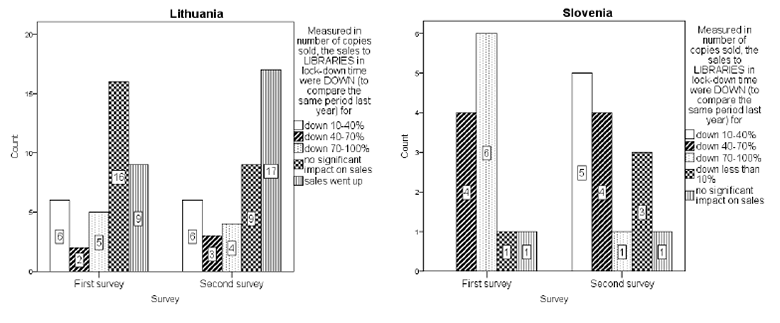

After three months there was no statistically significant changes (Z =-2.1, p=0.206) in sales to libraries in Lithuania, but answers biased towards increased sales. In Slovenia, some statistically significant (Z =-1.6, p=0.039) changes were registered. The number of respondents (6 of 12) who reported a 70–100% downturn in library sales in May decreased in August significantly (to 1 of 14), and the number of respondents who reported a softer drop increased from 1 of 12 in May to 7 of 14 in August, 2020.

Fig. 7. Change of sales to libraries in Lithuania and Slovenia in May and August 2020 (after a three-month interval)

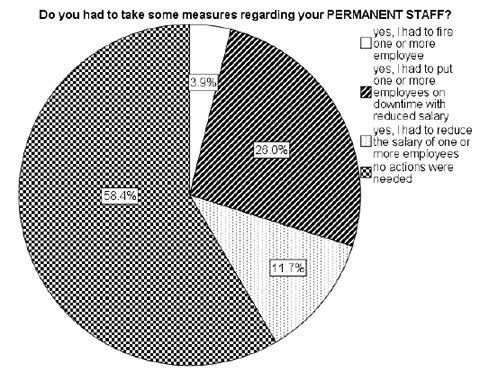

Measures regarding permanent staff. Overall, about half (58.4%) of respondents from all four countries answered that no serious cuts were needed regarding their permanent staff in May 2020 (Fig. 8). The worst situation was in Iceland – 7 of 16 respondents had to put one or more employees on downtime with reduced salary, 5 respondents had to reduce the salary of one or more employees, and one respondent had to dismiss one or more employee. Four of twelve Slovenian respondents had to put one or more employees on downtime with reduced salary, one had to reduce the salary of one or more employees and two had to dismiss one or more employee. A better situation was in Lithuania – 8 of 38 publishers had to put one or more employees on downtime with reduced salary, and two had to reduce the salary of one or more employees. Slovakia was less affected – two publishers of 11 had to reduce the salary of one or more employees.

In the first months of the lockdown just three respondents had to dismiss one or more employees – two (of 12) from Slovenia, both with 10 to 30 employees and one (of 16) from Iceland with less than 10 employees. During next months, in August, nine respondents reported that they dismissed employees – three (of 14) from Slovenia (two with less than 10 and one with 10–30 employees) and three (of 39) from Lithuania (one with just one employee, one with less than 10 and one between 10 and 30). Slovakia reported no fired employees at all.

Fig. 8. Measures regarding permanent staff in Iceland, Lithuania, Slovakia and Slovenia in May 2020

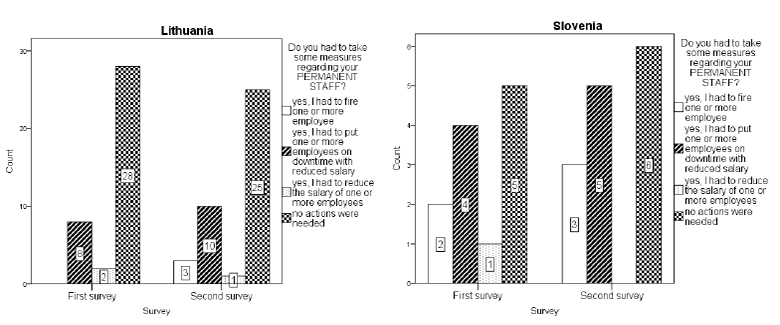

In August, some statistically significant (Z =-2.1, p=0.038) changes were noticed in Lithuania regarding permanent staff – in August, more respondents answered they had to put one or more employees on downtime with a reduced salary or even dismiss one or more employees. There was no statistically significant (Z =-0.4, p=1.000) changes regarding the permanent staff in Slovenia after three months (Fig. 9).

Fig. 9. Change measures regarding the permanent staff of respondents in Lithuania and Slovenia in May and August 2020 (after a three-month interval)

Prognosis for the future. In May 2020 we asked respondents about the future impact of the lockdown – how do they expect that pandemic will impact their future publishing strategies (open-ended question)? Respondents expected they will:

• be more cautious about what to publish (Iceland, Lithuania, Slovakia),

• probably publish less new titles (Lithuania, Slovakia, Slovenia), especially travel books (Iceland),

• publish more audiobooks (Iceland) and e-books (Iceland, Lithuania)

• publish more books for children (Iceland)

• sales will be more focused on online bookstores (Lithuania) and online marketing (Lithuania).

In addition, in August, 2020 we asked respondents in Lithuania and Slovenia about their plans for the current year (2020) and the following year. Answers revealed that respondents from Lithuania were more optimistic in comparison to Slovenia. Almost half (19 of 39) of Lithuanian respondents were sure they will publish all new titles they planned before the lockdown, whilst only about one fifth (3 of 14) Slovenian respondents thought the same. Another 19 of 39 of Lithuanian and even 10 of 14 Slovenian respondents were expecting to publish up to 20% less of new titles than planned. One respondent in each country expected to publish 0–20% of more new titles than planned.

Plans for the year 2021 revealed a similar picture: respondents from Lithuania were more optimistic than their Slovene counterparts. Almost a quarter (9 of 39) of Lithuanian respondents were sure they will publish more new titles than planned in 2020, and just one of 14 Slovenian respondents had the same expectations. Most of (10 of 14) Slovenian and about half (20 of 39) Lithuanian respondents were expecting to publish a similar number of titles next year. Also, 3 of 14 Slovenian and 10 of 39 Lithuanian respondents were expecting to publish up to 20% less new titles next year.

Discussion and conclusions

The COVID-19 lockdown until May 2020 resulted in decreased sales of all books in all four small book markets (Lithuania, Iceland, Slovakia and Slovenia): half (53.3%) of respondents reported that their sales were down for more than 40%, every third (29.9%) respondent was down up to 40% and just 17.1% of respondents answered that the COVID-19 lockdown had no significant impact on sales or even reported an increase in sales. Also, there were significant differences between the four countries, as Iceland and Lithuania were the only two countries in which a small set (around 15%) of respondents reported increased sales of all books. There were no such respondents in Slovakia and Slovenia.

The most affected country by sales decline seems to be Slovenia, where all respondents reported decreased sales. The least affected country was Lithuania with only approx. two thirds of respondents reporting decreased sales. After three months of opened bookstores, in August 2020, book sales improved in Slovenia, but remained more or less the same in Lithuania. Also, it seems that the drop in sales was felt least among publishers with less than 10 employees.

Results revealed that the publishing of e-books might depend on the population of a country – the largest proportion of e-book publishers (55.3%) was found in Lithuania and Slovakia (54.5%), two countries with the largest population in survey. The largest growth of e-book sales took place in Slovakia and Slovenia, where most respondents reported an increase in e-book sales. Respondents from Lithuania and Iceland reported mostly no impact on sales or just slightly increased sales. In August, the situation with e-book sales improved in Lithuania, but remained more or less the same in Slovenia.

Just every fifth respondent publishes audiobooks in all four countries, but overall audiobook sales increased, especially in Iceland, where the audio market is the most developed.

Lithuania was the only country with increased sales to libraries as almost every fourth respondent declared increase in sales. This could be explained by the fact that Lithuanian Government reacted to the COVID-19 lockdown by an increased funding for libraries.

More than half (58.4%) of respondents from all four countries reported that no actions were needed regarding their permanent staff in May 2020. The worst situation was in Iceland, where almost half of respondents had to put one or more employees on downtime with reduced salaries, reduce the salaries or had to dismiss one or more employee. Slovakia was less affected as just two respondents (of 11) reported that they had to reduce the salary of one or more employees.

In general, respondents in two countries with the highest online sales and highest audiobook and ebook income (Lithuania and Iceland) were less struck with the COVID-19 lockdown than the respondents in two countries (Slovakia and Slovenia) that rely more on traditional book formats and sales channels. Additionally, the opening of the brick and mortar bookstores in August had higher positive impact in less digital Slovenian publishing landscape that in Lithuania: nevertheless, Slovene publishers were less optimistic about the last quarter of 2020 than their more multi-channel Lithuanian counterparts.

Although such results indicate that there might be a correlation between the digitisation of book industries and their performances, we do not have enough data to confirm or reject such a hypothesis. More clear answers on how strong and sustainable the corona push towards the digitisation of book industries will be likely provided by the second wave of pandemics that we – hopefully! – plan to analyse in the first part of 2021.

Acknowledgements

We are grateful to the Lithuanian and Slovenian Publishers’ Associations and the Federation of European Publishers for their help in reaching publishers.

Literature

1. AGORAMOORTHY, Govindasamy et al. Queries on the COVID‐19 quick publishing ethics. In Bioethics [interaktyvus]. 2020, vol. 34, no. 6, p. 633–634. Prieiga per internetą: <https://onlinelibrary.wiley.com/doi/abs/10.1111/bioe.12772>.

2. ANDERSON, Porter. China’s Book Retail Market: Down 9.29 Percent in First Half of 2020. In Publishing Perspectives [interaktyvus]. 2020. Prieiga per internetą: <https://publishingperspectives.com/2020/07/china-book-retail-market-down-9-29-percent-in-first-half-of-2020-covid19/>.

3. FRANKLIN, Daniel. A global pandemic: publishing in the COVID-19 era and beyond. In Australian Journal of Forensic Sciences [interaktyvus]. 2020. Vol. 52, no. 4, p. 369–370. Prieiga per internetą: <https://www.tandfonline.com/doi/full/10.1080/00450618.2020.1774145>.

4. HORBACH, P.J.M. Serge. Pandemic Publishing: Medical journals drastically speed up their publication process for Covid-19. In bioRxiv [interaktyvus]. 2020. Prieiga per internetą: <http://biorxiv.org/content/early/2020/04/18/2020.04.18.045963.abstract>.

5. INTERNATIONAL PUBLISHERS ASSOCIATION African Publishing during the COVID-19 Pandemic. In IPA in Conversation with … [interaktyvus]. 2020. Prieiga per internetą: <https://www.internationalpublishers.org/copyright-news-blog/990-african-publishing-during-the-covid-19-pandemic>.

6. INTERNATIONAL PUBLISHERS ASSOCIATION Publishing in China during the COVID-19 Pandemic. In IPA in Conversation with … [interaktyvus]. 2020. Prieiga per internetą: <https://www.internationalpublishers.org/copyright-news-blog/1006-publishing-in-china-during-the-covid-19-pandemic>.

7. INTERNATIONAL PUBLISHERS ASSOCIATION Publishing in the USA during the COVID-19 Pandemic. In IPA in Conversation with … [interaktyvus]. 2020. Prieiga per internetą: <https://www.internationalpublishers.org/images/aa-content/other-ipa-events/other-ipa-events-2020/IPA-in-conversation-with/IPA_interview_series-_Maria_Pallante.pdf>.

8. LIETUVOS LEIDĖJŲ ASOCIACIJA Knygų leidybos sektoriaus vystymasis Lietuvoje: apžvalga. Vilnius: Lietuvos leidėjų asociacija, 2017, 39 p.

9. LIETUVOS STATISTIKOS DEPARTAMENTAS Oficialiosios statistikos portalas. In [interaktyvus]. 2019. Prieiga per internetą: <http://osp.stat.gov.lt>.

10. MARKEVIČIENĖ, Rita. TAMULYNIENĖ, Laima. Vilnius, 2019, [interaktyvus]. Prieiga per internetą: <https://www.lnb.lt/media/public/leidiniai/elektroniniai/lietuvos-spaudos-statistika/statistika2018.pdf>.

11. PALAYEW, Adam. et al. Pandemic publishing poses a new COVID-19 challenge. In Nature Human Behaviour [interaktyvus]. 2020, vol. 4, no. 7, p. 666–669. Prieiga per internetą: <http://www.nature.com/articles/s41562-020-0911-0>.

12. PANDA, Saumya. Publishing in the time of pandemic: Editorial policy of a dermatology journal during COVID-19. In Indian Journal of Dermatology, Venereology and Leprology [interaktyvus]. 2020, vol. 86, no. 4, p. 337. Prieiga per internetą: <http://www.ijdvl.com/text.asp?2020/86/4/337/285640>.

13. STATISTICS ICELAND [interaktyvus]. 2017. Prieiga per internetą: <https://statice.is/publications/news-archive/media/book-publishing-1999-2015/>.

14. THE BUSINESS RESEARCH COMPANY [interaktyvus]. 2020. Prieiga per internetą: <https://www.researchandmarkets.com/reports/5022380/book-publishers-global-market-report-2020-30>.

15. THE LANCET GLOBAL HEALTH Publishing in the time of COVID-19. In The Lancet Global Health [interaktyvus]. 2020, vol. 8, no. 7, p. e860. Prieiga per internetą: <https://linkinghub.elsevier.com/retrieve/pii/S2214109X20302606>.

16. TURRIN, Enrico. FEP SECRETARIAT [interaktyvus]. 2020. Prieiga per internetą: <http://europeanwriterscouncil.eu/fep-report-covid-booksector/>.

1 FRANKLIN, Daniel. A global pandemic: publishing in the COVID-19 era and beyond. Australian Journal of Forensic Sciences, 2020, vol. 52, no. 4, p. 369–370. Prieiga per internetą: <https://www.tandfonline.com/doi/full/10.1080/00450618.2020.1774145>

2 PANDA, Saumya. Publishing in the time of pandemic: Editorial policy of a dermatology journal during COVID-19. Indian Journal of Dermatology, Venereology and Leprology, 2020, vol. 86, no. 4, p. 337. Prieiga per internetą: <http://www.ijdvl.com/text.asp?2020/86/4/337/285640>

3 PALAYEW, Adam, et al. Pandemic publishing poses a new COVID-19 challenge. Nature Human Behaviour, 2020, vol. 4, no. 7, p. 666–669. Prieiga per internetą: <http://www.nature.com/articles/s41562-020-0911-0>

4 THE LANCET GLOBAL HEALTH. Publishing in the time of COVID-19. The Lancet Global Health, 2020, vol. 8, no. 7, p. e860. Prieiga per internetą: <https://linkinghub.elsevier.com/retrieve/pii/S2214109X20302606>

5 HORBACH, P.J.M. Serge. Pandemic Publishing: Medical journals drastically speed up their publication process for Covid-19. BioRxiv, 2020. Prieiga per internetą: <http://biorxiv.org/content/early/2020/04/18/2020.04.18.045963.abstract>

6 AGORAMOORTHY, Govindasamy, et al. Queries on the COVID‐19 quick publishing ethics. Bioethics, 2020, vol. 34, no. 6, p. 633–634. Prieiga per internetą: <https://onlinelibrary.wiley.com/doi/abs/10.1111/bioe.12772>

7 THE BUSINESS RESEARCH COMPANY. Book Publishers Global Market Report 2020-30: COVID-19 Impact and Recovery, 2020. Prieiga per internetą: <https://www.researchandmarkets.com/reports/5022380/book-publishers-global-market-report-2020-30>

8 INTERNATIONAL PUBLISHERS ASSOCIATION. Publishing in the USA during the COVID-19 Pandemic. IPA in Conversation with …, 2020. Prieiga per internetą: <https://www.internationalpublishers.org/images/aa-content/other-ipa-events/other-ipa-events-2020/IPA-in-conversation-with/IPA_interview_series-_Maria_Pallante.pdf>

9 INTERNATIONAL PUBLISHERS ASSOCIATION. Publishing in China during the COVID-19 Pandemic. IPA in Conversation with …, 2020. Prieiga per internetą: <https://www.internationalpublishers.org/copyright-news-blog/1006-publishing-in-china-during-the-covid-19-pandemic>

10 ANDERSON, Porter. China's Book Retail Market: Down 9.29 Percent in First Half of 2020. Publishing Perspectives, 2020. Prieiga per internetą: <https://publishingperspectives.com/2020/07/china-book-retail-market-down-9-29-percent-in-first-half-of-2020-covid19/>

11 INTERNATIONAL PUBLISHERS ASSOCIATION. African Publishing during the COVID-19 Pandemic. IPA in Conversation with …, 2020. Prieiga per internetą: <https://www.internationalpublishers.org/copyright-news-blog/990-african-publishing-during-the-covid-19-pandemic>

12 TURRIN, Enrico; FEP SECRETARIAT. Consequences Of The COVID-19 Crisis On The Book Market, 2020. Prieiga per internetą: <http://europeanwriterscouncil.eu/fep-report-covid-booksector/>

14 STATISTICS ICELAND, 2017. Prieiga per internetą: <https://statice.is/publications/news-archive/media/book-publishing-1999-2015/>

17 LIETUVOS LEIDĖJŲ ASOCIACIJA. Knygų leidybos sektoriaus vystymasis Lietuvoje; apžvalga. Vilnius: Lietuvos leidėjų asociacija, 2017. 39 p. <http://www.kulturostyrimai.lt/wp-content/uploads/2017/08/Knygu_leidybos_sektoriaus_vystymasis_Lietuvoje_apzvalga.pdf>

19 LIETUVOS STATISTIKOS DEPARTAMENTAS. Oficialiosios statistikos portalas, 2019. Prieiga per internetą: <http://osp.stat.gov.lt>

20 LIETUVOS LEIDĖJŲ ASOCIACIJA. Knygų leidybos sektoriaus vystymasis Lietuvoje: apžvalga. Vilnius: Lietuvos leidėjų asociacija, 2017. 39 p. <http://www.kulturostyrimai.lt/wp-content/uploads/2017/08/Knygu_leidybos_sektoriaus_vystymasis_Lietuvoje_apzvalga.pdf>