Organizations and Markets in Emerging Economies ISSN 2029-4581 eISSN 2345-0037

2025, vol. 16, no. 1(32), pp. 133–154 DOI: https://doi.org/10.15388/omee.2025.16.6

Does Fintech Usage Alter the Relationships Between Financial Literacy, Behaviour and Well-Being? Evidence from India

Shamli Prabhakaran (corresponding author)

CHRIST (deemed to be) University, India

shamli.p@res.christuniversity.in

https://orcid.org/0000-0003-4502-7357

https://ror.org/022tv9y30

Mynavathi L

CHRIST (deemed to be) University, India

l.mynavathi@christuniversity.in

https://ror.org/022tv9y30

Abstract. The emergence of fintech has rapidly transformed the way people manage their finances, yet its impact on personal financial outcomes remains relatively understudied. This study aims to examine how fintech usage (FTU) influences the relationship between financial literacy (FL) and financial well-being (FWB) through financial behaviour (FB) using a moderated mediation model. Using a proprietary dataset, the hypothesised relationships are analysed applying the PROCESS macro in IBM SPSS Statistics. The analysis reveals that FB is a partial mediator in the FL-FWB equation, while FTU negatively moderates the relationship between FL and FB. However, FTU does not significantly moderate the relationship between FL and FWB. The findings carry significant implications for policymakers and fintech service providers. Policymakers should strive to include a digital literacy component in financial education programs to better equip individuals to navigate today’s digitalised society, while fintech companies should focus on designing products that complement users’ FL and facilitate the adoption of financially healthy behaviours.

Keywords: financial literacy, financial behaviour, fintech usage, financial well-being

Received: 26/11/2024. Accepted: 28/2/2025

Copyright © 2025 Shamli Prabhakaran, Mynavathi L. Published by Vilnius University Press. This is an Open Access article distributed under the terms of the Creative Commons Attribution Licence, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

1. Introduction

The concept of financial well-being (FWB), which refers to an individual’s perceived competence in meeting their immediate and future financial obligations (CFPB, 2015), has gained substantial scholarly attention in recent years. This increased interest can be attributed to a combination of social and economic changes, including the shifting responsibility for retirement planning from governments to individuals, rising debt levels and economic instability highlighted by events such as the Great Recession and the COVID-19 pandemic. Beyond these financial reasons, FWB also has a notable impact on individuals’ mental health, general well-being and overall quality of life (Netemeyer et al., 2018), as emphasised by the UN Sustainable Development Goals 2030. As such, the health and economic implications of financially stable denizens and society highlight the need for understanding and fostering FWB.

Historically, an individual’s FWB has been primarily associated with their knowledge of basic financial concepts, commonly referred to as Financial Literacy (FL) (Joo& Grable, 2004). However, recent studies suggest that the relationship between FL and FWB is more complex than previously understood. They claim that a direct relationship between FL and FWB may not exist and identify several factors that can influence and potentially alter the connection between FL and FWB (Lee et al., 2020; Riitsalu & Murakas, 2019). Financial Behaviour (FB), which relates to any personal money management practice (Xiao, 2008), has emerged as particularly noteworthy in this context. Researchers argue that while FL provides the foundational knowledge to manage finances effectively, it is individuals’ actual behaviours – how they put that knowledge to use – that considerably influence their financial health (Bhatia & Singh, 2024; Gutter & Copur, 2011). Hence, this paper aims to explore the significance of FB by examining if it mediates the FL–FWB relationship.

In addition to FL and FB, recent studies have observed how the evolution of financial technology (fintech) has also affected individuals’ FWB. Fintech is an umbrella term that covers a diverse range of financial services accessed and delivered digitally, including but not limited to payments, lending, insurance, wealth management, cryptocurrency and regulatory technology and has essentially transformed the industry in a short period (Thakor, 2020). Emerging studies indicate that fintech usage (FTU) can have a positive impact on consumer finances (Carlin et al., 2019; French et al., 2020; S. A. Rahman et al., 2020), possibly by providing users with timely advice or innovative tools to manage their finances more efficiently. Fintech can even assist financial institutions in enhancing their decision-making processes by leveraging big data analytics to identify patterns, mitigate risks and optimise operations (Aldulaimi et al., 2022). At the societal level, fintech can lead to greater financial inclusion by offering affordable and secure access to financial services (Arner et al., 2020). While the benefits of fintech cannot be negated, there have also been several risks and negative consequences associated with FTU, especially for users who lack the necessary financial acuity to use them responsibly (Ahn & Nam, 2022; Ooi et al., 2024; Panos & Wilson, 2020). Given the rapid rise of fintech and its divergent outcomes, it is imperative to understand how FTU interacts with users’ financial knowledge and skills and impacts their financial outcomes. This enquiry is especially important in a country like India, where fintech adoption has risen exponentially, but FL remains low (BFSI, 2023). Hence, this study aims to assess the moderating role of FTU in the relationships between FL and FB and between FL and FWB.

The objective of this study is twofold: (1) to determine whether FB mediates the relationship between FL and FWB and (2) to examine if FTU moderates the FL–FB and FL–FWB relationships. Primary data were collected using self-administered questionnaires from Indian citizens aged 21 and above to meet these objectives. The first objective was addressed using a mediation analysis conducted with Model 4 from the PROCESS macro in SPSS, while the second objective utilises a moderated mediation framework, analysed using the PROCESS Model 8. The results reveal that FL is related to FWB, and FB partially mediates this relationship. The latter model establishes that FTU negatively moderates the relationship between FL and FB. These findings highlight the need for digital financial literacy programs that promote prudent financial decision-making and responsible technology use. Unlike previous studies that focused on the direct impact of fintech on financial outcomes (de Bassa Scheresberg et al., 2020; Zhang & Fan, 2024), this study takes into account the FL levels of fintech users and examines how FTU moderates the relationship between FL, FB, and FWB. This nuanced approach highlights how financially unsophisticated users are vulnerable to fintech tools available in the market and how irresponsible FTU could impair their financial health. This study also makes a substantial contribution to the growing literature on fintech by highlighting the negative consequences of FTU in a developing country and recommends actionable strategies for policymakers and fintech service providers to improve individuals’ financial outcomes and resilience in this technology-driven era.

2. Literature Review and Hypotheses Development

2.1 Financial Literacy and Well-being

The importance of FL in today’s world cannot be overstated. There is ample research linking FL to numerous positive financial outcomes like higher savings rates (Babiarz & Robb, 2014), wealth accumulation (van Rooij et al., 2012), financial security in retirement (Lusardi & Mitchell, 2011, 2007), reduced financial stress (Kadoya et al., 2018), improved ability to navigate financial markets (Lusardi & Messy, 2023) and overall better financial decision-making (Klapper et al., 2013; Lusardi, 2012). Conversely, poor FL can lead to various adverse consequences such as excessive borrowing (Gathergood, 2012), increased vulnerability to financial scams (Rey-Ares et al., 2024) and a greater likelihood of experiencing financial hardships (Karakara et al., 2022), which can result in financial instability and diminished living standards. Given the significant role of FL in enhancing financial outcomes, it is evident that it is also a driving factor in improving FWB. Therefore, this study hypothesises that:

H1: There is a positive relationship between FL and FWB.

2.2 The Mediating Role of Financial Behaviour

While the ultimate goal of FL is to elevate individuals’ FWB, some studies suggest that higher FL may not automatically translate to improved FWB (Mahdzan et al., 2019; Utkarsh et al., 2020). Some researchers argue that the practical application of financial knowledge through healthy FBs is more crucial in elevating FWB than merely acquiring and accumulating knowledge (Kumar et al., 2023; Sabri et al., 2023). Hence, examining the relationship between FL, FB, and FWB is essential, as effective FB is often seen as an intermediary that channels the benefits of FL into tangible improvements in FWB.

Higher levels of FL can foster responsible FBs, such as regularly budgeting, saving, and investing (Allgood & Walstad, 2016). Therefore, this study posits that:

H2: There is a positive relationship between FL and FB.

These healthy behaviours, in turn, contribute to an individual’s FWB by promoting discipline, reducing uncertainties and building financial resilience (M. Rahman et al., 2021). Thus, the following hypotheses are set forth to validate the proposition that FB acts as a conduit through which FL translates into FWB:

H3: There is a positive relationship between FB and FWB.

H4: FB mediates the relationship between FL and FWB.

2.3 The Moderating Role of Fintech Usage

The advent of fintech over the past decade has revolutionised the financial landscape, considerably changing how individuals manage their finances. It has transformed traditional financial practices by making financial transactions more accessible, efficient, and user-friendly (Gomber et al., 2017). It has also spurred greater transparency in banks and financial institutions, as digital channels have streamlined the disclosure of financial information to clients and stakeholders while simultaneously helping companies strengthen their sustainability efforts and promote green finance (Al Alkawi & B. J. A. Ali, 2022; Alaoui & Samir Mohamed, 2024; Li et al., 2024). Fintech advancements have played a significant role in facilitating financial inclusion, particularly among underserved and marginalised populations, by providing them with tools to manage their finances more effectively (Salampasis & Mention, 2018). They have also expanded the reach of alternative financing methods, enabling individuals and small businesses to raise capital without traditional financial intermediaries and at relatively lower costs (Abdeldayem & Aldulaimi, 2023; Shehadeh et al., 2024).

Additionally, fintech innovations offer numerous benefits that can positively impact personal financial outcomes. Yoo and Fisher (2017) and French et al. (2020) stated that using fintech applications was associated with financially capable behaviours as they improve financial knowledge, optimise financial management, and provide tools for more informed decision-making. These applications offer many useful features like real-time expense tracking, automated savings, and personalised financial advice, which help users develop healthier FBs and make smarter financial choices (Carlin et al., 2019).

While the advantages of fintech are substantial, over-reliance on technology may also lead to unintended negative consequences on FB. For example, the convenience of digital payments and instant credit access have been linked to impulsive spending and increased debt levels among fintech users (Ahn & Nam, 2022; Relja et al., 2024; Yue et al., 2022). De Bassa Scheresberg et al. (2020) found that mobile payment users in the US were more likely to engage in detrimental FBs, such as overspending, borrowing from alternative sources, and withdrawing from retirement accounts. These findings were corroborated by Garrett et al. (2014) and Walsh and Lim (2020), underscoring the potential downsides associated with adopting fintech.

Such divided perspectives highlight the need for further investigation into the impact of FTU on financial outcomes. In the same study, Mahdzan et al. (2023) reported that fintech use weakened the effect of FB and FWB while mitigating the negative impact of financial stress on FWB. The conflicting findings suggest that FTU could either amplify or weaken the effects of FL on FB and FWB. Hence, the study proposes that:

H5: FTU moderates the relationship between FL and FB.

H6: FTU moderates the relationship between FL and FWB.

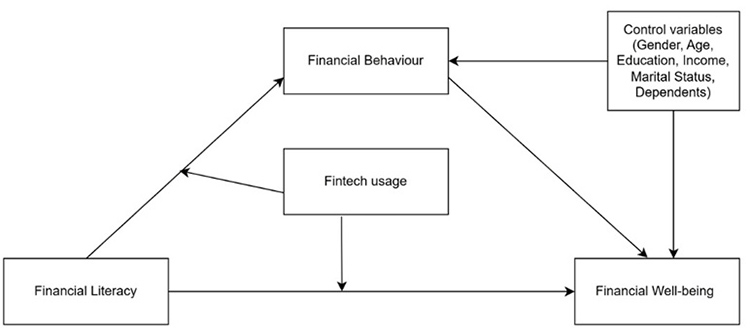

Figure 1 illustrates the proposed moderated mediation model, examining the relationship between FL and FWB, with FB mediating this relationship and FTU moderating the paths from FL to FB and FWB. The analysis also controls for socio-demographic variables.

Figure 1

Research Model

3. Methodology

The study employs a cross-sectional research design to investigate the moderating role of FTU on the relationship between FL and FWB through FB. For this purpose, primary data were collected from Indian residents aged 21 years or older, as they are more likely to be in charge of their financial decisions. Given the lack of recent census data and a complete sampling frame, convenience sampling was used. Despite its limitations and potential biases, this approach has been widely used in research, as it allows the researchers to collect data from readily accessible participants, making it the practical choice (Jager et al., 2017). Data were collected through a Google Form distributed via various social media platforms between April 2024 and June 2024. Participants were informed about the voluntary nature of the study and assured of anonymity. No identifying information was collected to encourage respondents’ honesty and reduce the likelihood of response bias. The digital questionnaire comprised five sections: socio-demographic characteristics, FL, FTU, FB and FWB. Out of the 502 responses received, incomplete responses and outliers were excluded, resulting in a final sample of 474 for analysis.

The proposed research model specified FL as the independent variable, FWB as the outcome variable, FB as the mediating variable and FTU as the moderating variable. Socio-demographic characteristics such as age, gender, education, income, marital status, and financial dependents were included as control variables to ensure that these factors did not confound the relationships observed between the focal variables. The scales used to measure the focal variables are detailed in the following section.

3.1 Measures

1. FL was measured using a set of five questions covering key financial concepts, collectively recognised as the “Big 5” due to their extensive replication and adaptation (Hastings et al., 2013; Robb et al., 2012). An additive scale was constructed, with the total number of correct answers representing each respondent’s FL score, ranging from 0 to 5.

2. FB was measured using a set of 12 questions covering a wide range of money management practices adapted from Dew and Xiao (2011). Respondents were asked to rate how frequently they engaged in financial activities like making prompt bill payments, sticking to a budget, saving and investing, etc., using a 5-point Likert scale, with five indicating “always” and one indicating “never”. The scale’s reliability was measured using Cronbach’s alpha, which yielded a value of 0.87, indicating good internal consistency among the items.

3. FTU was measured based on the respondents’ frequency of using three major fintech services: mobile banking, payments, and lending. In line with the approach taken by Kakinuma (2002), this study focuses on the actual usage of fintech services, recognising that the utility and impact of fintech services are best understood through direct usage experience rather than mere intent. Using these three distinct fintech services offers a broader scope to examine respondents’ engagement with fintech applications than previous studies that used a single measure. Cronbach’s alpha of 0.901 demonstrates a strong internal consistency.

4. FWB was assessed using the abbreviated version of the FWB scale developed by the Consumer Financial Protection Bureau (CFPB, 2015). This scale includes five items designed to capture key aspects of FWB, including financial security, perceived financial control, and the ability to meet financial goals. Cronbach’s alpha was 0.85.

3.2 Data Analysis

The present study uses Hayes’s (2017) PROCESS macros to assess the mediating role of FB and the moderating role of FTU in the FL–FWB equation. This method was employed for its flexibility in handling degree of freedom restrictions and smaller sample sizes and for providing accurate results without complex programming like structural equation modelling (Hayes et al., 2017). It also provides an overall moderated mediation index that helps statistically validate the proposed research model. Although it estimates each equation’s parameters separately, the PROCESS results do not significantly differ from those of SEM.

The variables for FB, FTU and FWB were formed by calculating the mean of their respective scale items, while the additive scale created for FL was used as is. Subsequently, Pearson correlation analysis was performed to examine the relationship among the key variables. Next, the PROCESS macro for SPSS Model 4 was used to analyse the mediating effect of FB in the relationship between FL and FWB. Hayes (2009) advocated for the use of this method to overcome the statistical limitations of the traditional mediation analysis approach proposed by Baron and Kenny (1986). PROCESS Model 8 was then used to assess the combined moderated mediating effect of FTU and FB. A non-parametric, distribution-free bootstrapping technique with 5,000 resamples was employed in both models to obtain the 95% confidence intervals. This approach was deemed acceptable by Hayes (2017), as it addresses Type 1 error concerns. The following section presents the results of the data analysis.

4. Results

Table 1

Demographic Profile of the Respondents

|

Variable |

N |

% |

|

Gender |

||

|

Male Female |

227 247 |

47.9 52.1 |

|

Education |

||

|

Pre-University Course Undergraduate Postgraduate or higher |

23 332 118 |

4.9 70.3 24.9 |

|

Annual income |

||

|

Less than INR 5,00,000 INR 5,00,001 – 10,00,000 INR 10,00,001 – 15,00,000 INR 15,00,001 – 20,00,000 More than INR 20,00,000 |

181 137 69 34 53 |

38.2 28.9 14.6 7.2 11.2 |

|

Number of dependents |

||

|

None 1 2 3 or more |

182 80 126 86 |

38.4 16.9 26.6 18.1 |

|

Marital status |

||

|

Single Married |

221 253 |

46.6 53.4 |

Table 1 provides an overview of the respondents’ socio-demographic characteristics – 47.9% of the sample identified as male and 52.1% as female. Most respondents have college-level education, indicating a highly literate sample population. 38.2% of the respondents earn less than INR 5,00,000 annually, while 11.2% fall into the highest income bracket of more than INR 20,00,000. 38.4% of the respondents have no financial dependents in the form of children or elderly family members. The marital status distribution indicates a nearly even split between single (46.6%) and married (53.4%) individuals. The minimum age of respondents is 21, and the maximum is 67, with a mean value of 32.

Table 2

Summary Statistics and Correlation Matrix

|

Variable |

Mean |

SD |

(1) |

(2) |

(3) |

|

(1) Financial Literacy |

2.99 |

1.539 |

|||

|

(2) Financial Behaviour |

3.47 |

0.860 |

0.389*** |

||

|

(3) Fintech Usage |

2.20 |

1.407 |

0.083* |

-0.120** |

|

|

(4) Financial Well-being |

3.49 |

0.929 |

0.423*** |

0.506*** |

-0.281*** |

Note. *** denotes p < 0.01, ** signifies p < 0.05, * denotes p < 0.1.

Table 2 presents the descriptive statistics and correlations among the focal variables. The results indicate a relatively high FL and FB score, below-average levels of FTU and elevated levels of FWB. The standard deviations show the variability within the sample for each variable. Correlation analysis reveals a significant relationship among the key variables. FL positively correlates with all other variables, whereas FTU negatively correlates with FB and FWB. These correlations suggest that higher FL and better FB are associated with greater FWB, while FTU is negatively associated with FB and FWB. Before proceeding with the analysis, variance inflation factor (VIF) values were calculated to assess multicollinearity. All values were well below the acceptable threshold recommended by Hair et al. (2010), indicating no multicollinearity concerns.

Table 3 summarises the findings from the PROCESS Model 4. This model employs a three-step approach to investigate the mediating effect of FB on the relationship between FL and FWB while controlling for the effects of age, gender, income, marital status, and the number of dependents. Firstly, it assesses the total effect of FL on FWB. Secondly, it examines the impact of FL on FB. At last, it evaluates the direct effect of FL on FWB, controlling for FB. The results show that FL is a significant predictor in all three steps, supporting hypotheses H1 and H2. The results also indicate that FB is a significant predictor of FWB, and the mediation effect accounts for 38% of the total effect of FL on FWB. These findings support H3 and H4, implying a strong partial mediating role of FB in the association between FL and FWB. Additionally, the analysis reveals that females, older individuals and high-income earners seem to engage in healthier FBs and enjoy greater FWB. In contrast, those with more dependents tend to have lower levels of FWB, possibly due to additional financial obligations. The total effect model explains 28.1% variance in FWB (adjusted R2 = 0.270 after accounting for the number of predictors in the model), whereas the model predicting FB explains 27.6% variance (adjusted R2 = 0.265). The final mediation model explains 37.5% variance in FWB (adjusted R2 = 0.364), indicating a significant improvement in the model’s explanatory power when accounting for FB. Similar R2 values have been reported by studies in social sciences research (Muttar et al., 2021; Riitsalu & Murakas, 2019; Tahir et al., 2021), supporting the adequacy of this model’s explanatory power.

Table 3

Result of the PROCESS Model 4 (Mediation Analysis)

|

Variable |

Financial Well-being |

Financial Behaviour |

Financial Well-being |

||||||

|

Coefficient |

LB |

UB |

Coefficient |

LB |

UB |

Coefficient |

LB |

UB |

|

|

Age |

0.014(0.006)** |

0.002 |

0.025 |

0.019(0.006)*** |

0.008 |

0.030 |

0.006(0.006) |

-0.005 |

0.018 |

|

Female |

0.183(0.078)** |

0.030 |

0.337 |

0.112(0.072) |

-0.030 |

0.254 |

0.140(0.073)* |

-0.004 |

0.283 |

|

Education |

0.134(0.073)* |

-0.009 |

0.277 |

0.083(0.068) |

-0.050 |

0.216 |

0.102(0.068) |

-0.032 |

0.235 |

|

Income |

0. 217(0.031)*** |

0.157 |

0.277 |

0.128(0.028)*** |

0.072 |

0.184 |

0.167(0.029)*** |

0.110 |

0.225 |

|

Marital Status |

-0.086(0.095) |

-0.272 |

0.100 |

0.117(0.088) |

-0.056 |

0.290 |

-0.131(0.089) |

-0.305 |

0.043 |

|

Dependents |

-0.084(0.036)** |

-0.155 |

-0.012 |

0.046(0.034) |

-0.020 |

0.112 |

-0.101(0.034)** |

-0.168 |

-0.035 |

|

FL |

0.188(0.025)*** |

0.138 |

0.238 |

0.183 (0.024)*** |

0.137 |

0.230 |

0.117(0.025)*** |

0.067 |

0.166 |

|

FB |

0.389(0.047)*** |

0.297 |

0.480 |

||||||

|

N |

474 |

474 |

474 |

||||||

|

R2 |

0.281 |

0.276 |

0.375 |

||||||

|

Adjusted R2 |

0.270 |

0.265 |

0.364 |

||||||

|

F |

26.032*** |

25.334*** |

34.865*** |

||||||

|

Mediation effect |

-38% |

||||||||

Note. Column I shows the total effects of FL on FWB, Column II shows the results of regressing FL on FB, and Column III shows the direct effect of FL on FWB while controlling for FB. ***=p < 0.01, **=p < 0.05, *=p < 0.1. Coefficients are unstandardised, and standard errors are in parentheses. LB and UB denote the lower bound and upper bound, respectively.

Table 4 displays the results of the PROCESS Model 8, which evaluates the moderated mediation effects of the variables while accounting for the influence of socio-demographic factors. This analysis involves running two separate regressions to assess the moderating role of FTU in the association between FL and FB and between FL and FWB. The results from these regressions show that the interaction between FL and FTU is statistically significant and negative in the case of FB but not FWB. This finding suggests that FTU negatively moderates the FL–FB relationship, such that higher FTU weakens the relationship between FL and FB, thereby supporting hypothesis H5. However, H6 is unsupported, as FTU does not moderate the FL–FWB relationship. Among the control variables, age positively impacts FB, and income significantly impacts both FB and FWB. In contrast, having more dependents negatively affects one’s FWB. The model explains 29.2% of the variance in FB (adjusted R2 = 0.278) and 45.8% of the variance in FWB (adjusted R2 = 0.446), both of which are deemed acceptable (Ozili, 2023).

Table 4

Results of the PROCESS Model 8 (Moderated Mediation Analysis)

|

Variable |

Financial Behaviour |

Financial Well-being |

||||

|

Coefficient |

LB |

UB |

Coefficient |

LB |

UB |

|

|

Age |

0.014(0.006)** |

0.003 |

0.025 |

-0.003(0.005) |

-0.014 |

0.008 |

|

Gender - Female |

0.098(0.074) |

-0.047 |

0.244 |

0.016(0.070) |

-0.122 |

0.154 |

|

Education |

0.093(0.067) |

-0.039 |

0.225 |

0.108(0.064)* |

-0.017 |

0.233 |

|

Income |

0.126(0.028)*** |

0.070 |

0.181 |

0.178(0.027)*** |

0.124 |

0.232 |

|

Marital Status |

0.124(0.087) |

-0.047 |

0.296 |

-0.128(0.083) |

-0.291 |

0.035 |

|

Dependents |

0.040(0.034) |

-0.026 |

0.106 |

-0.121(0.032)*** |

-0.184 |

-0.059 |

|

FL |

0.177(0.024)*** |

0.131 |

0.224 |

0.135(0.024)*** |

0.088 |

0.182 |

|

FTU |

-0.053(0.026)** |

-0.104 |

-0.002 |

-0.208(0.025)*** |

-0.257 |

-0.159 |

|

FL x FTU |

-0.049(0.018)** |

-0.085 |

-0.013 |

-0.013(0.017) |

-0.047 |

0.021 |

|

Financial behaviour |

0.355(0.044)*** |

0.268 |

0.441 |

|||

|

N |

474 |

474 |

||||

|

R2 |

0.292 |

0.458 |

||||

|

Adjusted R2 |

0.278 |

0.446 |

||||

|

F |

21.230*** |

39.068*** |

||||

Note. *** represents p < 0.01, ** denotes p < 0.05, * signifies p < 0.1. Coefficients are unstandardised, and standard errors are in parentheses. LB and UB denote the lower bound and upper bound, respectively.

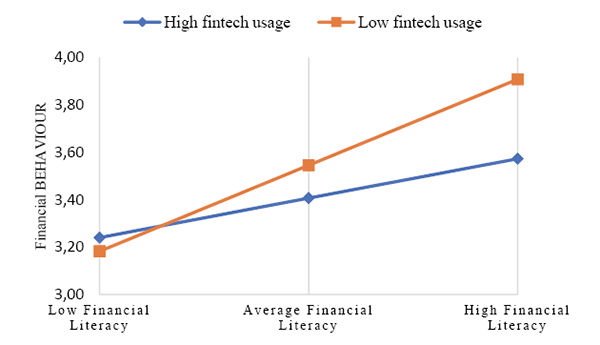

Figure 2

Plot of Interaction Between FL and FTU on FB

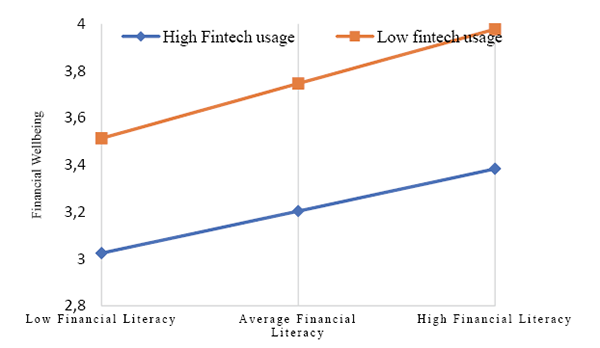

Figure 3

Plot of Interaction Between FL and FTU on FWB

Additionally, the predicted FB and FWB scores were plotted against FL for both high and low levels of FTU. Figure 2 displays the predicted FB scores and indicates a positive association between FL and FB, which is more pronounced for individuals with low FTU than those with high FTU. For respondents with low FTU, FB significantly improves with increasing FL. In contrast, while FB also improves with increasing FL for those with high FTU, the improvement is less substantial.

Figure 3 presents the predicted FWB scores. The graph shows a consistent positive relationship between FL and FWB for high and low FTU groups. However, individuals with low FTU experience a higher baseline FWB level across all FL levels than those with high FTU. The slopes of the lines for high and low FTU are parallel, suggesting that fintech usage does not change the strength of the relationship between FL and FWB, i.e., FWB increases with FL regardless of the level of FTU. These findings imply that improving FL could enhance FB and FWB, while FTU needs to be approached cautiously to avoid potential negative impacts on financial outcomes.

Table 5

Summary of Indirect Effects at Different Levels of FTU

|

Financial Well-being |

|||

|

Coefficient |

LB |

UB |

|

|

Conditional indirect effect of FL on FWB |

|||

|

Lesser FTU (-1.196) |

0.084(0.016) |

0.056 |

0.117 |

|

Mean FTU |

0.063(0.012) |

0.042 |

0.089 |

|

Higher FTU (1.407) |

0.038(0.015) |

0.012 |

0.069 |

|

Overall index of moderated mediation |

-0.017(0.007) |

-0.032 |

-0.005 |

Note. Standard errors are in parentheses. LB and UB denote the lower bound and upper bound, respectively. If no “0” exists between the LB and UB values, the indirect effect is considered statistically significant at the 5% level.

Table 5 presents the pathways between FL and FWB via FB at different levels of FTU. The findings indicate that the indirect effect is the strongest at low FTU, weaker at average usage, and the weakest at high usage. These conditional indirect effects are statistically significant as their confidence intervals do not include zero, demonstrating that the level of FTU moderates the strength of the indirect effect of FL on FWB. Specifically, as FTU increases, the positive impact of FL on FWB via FB decreases. The overall index of moderated mediation is negative and statistically significant, further supporting the conclusion that FTU has a dampening effect on the indirect pathway from FL to FWB through FB.

4. Discussion

This paper unravels the pathways between FL and FWB through FB and investigates how this relationship is affected by FTU. The study’s findings affirm the positive relationship between FL and FWB by lending support to previous research (Lusardi & Messy, 2023; Philippas & Avdoulas, 2020; Tahir et al., 2021). In other words, financially literate individuals are more likely to attain greater levels of FWB. While this relationship has been extensively studied, there is a dearth of research examining the mediators and moderators that could impact it. This study addresses the gap by establishing the mediating role of FB and the moderating role of FTU in the association between FL and FWB.

The Organisation for Economic Co-operation and Development defines FL as a combination of awareness, knowledge, skill, attitude and behaviour necessary to make sound financial decisions and ultimately achieve individual financial well-being (OECD, 2020). This study, however, keeps the concepts of “financial literacy” and “financial behaviour” distinct to examine how the former can lead to FWB, with the latter playing an intervening role. Hence, this paper purports FL to represent the knowledge of basic financial concepts (Lusardi & Mitchell, 2008), while FB denotes the actions taken based on that knowledge to manage personal finances and improve financial health (Dew & Xiao, 2011). The study findings point to a positive association between FL and desirable FBs, such as responsible cash and credit management, timely bill payments, and consistent budgeting and saving, congruent with the findings of Allgood and Walstad (2016).

Another positive relationship is observed between FB and FWB, consistent with the literature (Joo & Grable, 2004; Netemeyer et al., 2018). These studies state that FB is the most important determinant of one’s FWB, as it helps individuals achieve their long-term financial goals, thereby reducing financial stress and improving their overall financial satisfaction. This relationship indicates that the proposed mediation is partial and complementary since FL is also positively associated with FWB.

The second model studies the moderating role of FTU in the relationships between FL and FB, as well as FL and FWB, which has not been considered in previous research. The first set of findings reveals that FTU is significantly and negatively associated with FB and FWB. These results are in accordance with previous studies (de Bassa Scheresberg et al., 2020; Meyll & Walter, 2019; Walsh & Lim, 2020), which state that overuse of fintech products can lead to irresponsible FBs, such as overspending and over-reliance on costly credit, which could lead to poor financial health. While fintech offers countless benefits, its misuse can adversely affect FBs and diminish overall FWB (Zhang & Fan, 2024).

The findings also state that FTU negatively moderates the relationship between FL and FB. This is a notable contribution to the literature, as it demonstrates that while FL typically improves FB, excessive FTU can undermine this effect. This negative impact may stem from fintech users’ increased exposure to high-interest credit and buy-now-pay-later (BNPL) options that are designed to encourage consumer spending. This access may lead individuals, even those financially literate, to engage in spending habits that detract from responsible FB. As a result, the intended influence of FL on prudent financial management is attenuated. Similar observations were made by Powell et al. (2023), who stated that BNPL users are prone to impulsive spending behaviours.

Moreover, the constant use of payment applications could also deter users from engaging in sound financial practices. Shah et al. (2024) noticed that consumers spent more when using digital payments than physical cash. Popular payment applications also try to incentivise frequent transactions by offering cash-back offers and other rewards, which can subtly encourage spending and make it more difficult for users to resist unnecessary purchases (Ahn & Nam, 2022; An et al., 2024). While these features may seem convenient and rewarding, the frequent prompts to earn or save through spending can overwhelm users, leading to a state of cognitive overload, which might weaken users’ ability to apply their financial knowledge in practice and maintain disciplined FBs.

On the contrary, there is no significant moderation effect of FTU in the FL-FWB equation, indicating that the positive impact of FL on FWB remains robust irrespective of the level of FTU. However, in the indirect relationship between FL and FWB via FB, FTU’s negative influence is notable. This finding suggests that fintech tools reduce users’ reliance on financial knowledge and skills, potentially leading to unfavourable outcomes (Bi et al., 2021; Zhang & Fan, 2023); hence, they should be used with caution.

5. Practical Implications

5.1 For Policymakers and Educators

The importance of FL in shaping both FB and FWB reaffirms the importance of promoting FL initiatives to empower individuals with the knowledge and skills necessary to make pragmatic financial decisions. Given that trust and power are known to influence financial behaviours and compliance (Batrancea et al., 2023; Kogler et al., 2023), it is incumbent on the government and policymakers to foster an environment that encourages FL and responsible FB. Mandated FL programs should be integrated into formal education curricula, starting from schools, so the upcoming generations will be equipped to deal with the changing financial landscape. Tailored financial education courses for adults can address financial challenges and needs at different life stages, ensuring continuous financial learning. These initiatives should prioritise fostering healthy FBs over the theoretical understanding of financial concepts to ensure that the participants can effectively apply their knowledge in the real-world context and achieve better financial outcomes. The negative consequences associated with FTU highlight the need for a digital-oriented approach to financial education. FL curricula should incorporate a digital literacy component to help individuals use fintech tools effectively while ensuring they do not become overly reliant on them to make critical financial decisions.

5.2 For Fintech Service Providers

Fintech companies should focus on developing products that complement and enhance users’ financial knowledge to facilitate better financial management. They should incorporate additional features within the applications, like goal-tracking and spending analytics, which can provide personalised insights on their finances and foster responsible FBs. Also, spending caps and in-app nudges can prompt users toward mindful spending, while rewards for sticking to budgets could further encourage financial discipline. Introducing gamification elements or interactive features such as earning points and unlocking achievements could make budgeting and saving more engaging, especially for younger users, and motivate them to stay committed to their financial goals. They can also integrate educational platforms, similar to the “Varsity” initiative by Zerodha, a leading wealthtech firm in India, to offer FL courses and resources, helping users gain knowledge and make informed decisions (Business Today, 2024). Ultimately, fintech service providers should adopt ethical practices and prioritise users’ financial well-being over short-term profits, as this approach is more likely to cultivate customer loyalty and facilitate long-term growth.

5.3 For Regulators

The risks associated with fintech products underscore the need for stricter regulatory frameworks. Regulators should ensure that fintech products available to consumers are ethically marketed, easy to understand and transparent, especially when it comes to high-cost credit options. Greater oversight and stronger consumer protection laws are required to protect users from predatory practices and security issues.

5.4 For Consumers

Consumers should exercise caution and educate themselves about the potential pitfalls associated with FTU. They must use due diligence when opting for fintech tools to ensure that all product-related information is thoroughly reviewed, especially hidden fees, security and data privacy concerns. They must balance the benefits of fintech with sound financial practices to avoid overreliance on technology and adverse effects on their finances. Ultimately, the onus is on the individuals to make prudent financial decisions and safeguard their FWB.

6. Conclusion and Limitations

The study provides novel insights into the association between FL and FWB through FB, highlighting the previously unexplored moderating role of FTU. The findings reaffirm the importance of FL in shaping financial outcomes. However, the growing reliance on fintech undermines its impact, highlighting the urgent need for digital financial literacy, which has become a critical part of empowerment in this digital age. India presents a uniquely compelling case as a trailblazer for technological advancements in finance (Migozzi et al., 2023), yet has an alarmingly low rate of FL (NCFE, 2019). This study underscores the importance of bridging this gap to ensure positive financial outcomes for all citizens. Empowering individuals through comprehensive digital financial education and fostering a safer fintech ecosystem will not only enhance personal financial health but also contribute to a more resilient and stable economy.

Despite this study’s substantial contribution, it is not without limitations. The cross-sectional design limits the ability to draw causal conclusions. Future studies should consider longitudinal designs to understand the long-term implications of fintech adoption on individuals’ financial outcomes. The study also used convenience sampling, which resulted in a sample skewed mainly towards urban, educated participants, limiting the generalisability of the findings. Similar research should be conducted with diverse samples to ensure the generalisability of the study’s findings. Comparative studies across different socioeconomic and geographic groups can provide valuable insights into the complex nexus between FTU and financial outcomes. Also, while the study considers three major fintech services widely used in India, it does not differentiate between the segments or examine how each segment may impact FB and FWB separately. Future research could refine the analysis by investigating specific types of fintech services and their unique effects on financial outcomes or by expanding the scope to include a broader range of fintech offerings as the industry keeps evolving rapidly. In short, extensive probing is required to understand how the advancements in fintech have impacted and will continue to impact individuals’ financial management behaviours and well-being.

References

Abdeldayem, M., & Aldulaimi, S. (2023). Developing an Islamic crowdfunding model: A new innovative mechanism to finance SMEs in the Middle East. International Journal of Organizational Analysis, 31(6), 2623–2644. https://doi.org/10.1108/IJOA-02-2022-3159

Ahn, S. Y., & Nam, Y. (2022). Does mobile payment use lead to overspending? The moderating role of financial knowledge. Computers in Human Behavior, 134. https://doi.org/10.1016/j.chb.2022.107319

Al Alkawi, T., & Ali, B. J. A. (2022). Electronic Financial Disclosure level on the Commercial Bank Sector of Bahrain Bourse. International Journal of Green Management and Business Studies, 2(2). https://doi.org/10.56830/GGAQ2504

Alaoui, A., & Samir Mohamed, S. (2024). The Impact of Corporate Social Responsibility on Financial Performance: A Comparative Study of Green and Non-Green Firms. International Journal of Green Management and Business Studies, 4(1). https://doi.org/10.56830/IJGMBS06202403

Aldulaimi, S. H., Ali, B. J. A., Yas, Q. M., Abdeldayem, M. M., Aswad, A. R., & Hammad, A. M. (2022). Application of Big Data Analysis to Foresight the Future: A Review of Opportunities, Approaches, and New Research Directions. 2022 ASU International Conference in Emerging Technologies for Sustainability and Intelligent Systems (ICETSIS), 346–354. https://doi.org/10.1109/ICETSIS55481.2022.9888841

Allgood, S., & Walstad, W. B. (2016). The effects of perceived and actual financial literacy on financial behaviors. Economic Inquiry, 54(1), 675–697. https://doi.org/10.1111/ecin.12255

An, T., Xiao, J. J., Porto, N., & Cruz, L. (2024). Mobile payment, financial behavior and financial anxiety: A multi-group structural equation modeling study. International Journal of Bank Marketing, 43(3), 549–568. https://doi.org/10.1108/IJBM-07-2024-0402

Arner, D. W., Buckley, R. P., Zetzsche, D. A., & Veidt, R. (2020). Sustainability, FinTech and Financial Inclusion. European Business Organization Law Review, 21(1), 7–35. https://doi.org/10.1007/s40804-020-00183-y

Babiarz, P., & Robb, C. A. (2014). Financial Literacy and Emergency Saving. Journal of Family and Economic Issues, 35(1), 40–50. https://doi.org/10.1007/s10834-013-9369-9

Baron, R. M., & Kenny, D. A. (1986). The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173–1182. https://doi.org/10.1037/0022-3514.51.6.1173

Batrancea, L. M., Kudła, J., Błaszczak, B., & Kopyt, M. (2023). A dataset on declared tax evasion attitudes of students and entrepreneurs from Poland under the slippery slope framework. Data in Brief, 48, 109183. https://doi.org/10.1016/j.dib.2023.109183

BFSI. (2023). India has highest FinTech adoption rate, gains 3rd place in payments, highlights Economic Survey, BFSI News, ET BFSI. https://bfsi.economictimes.indiatimes.com/budget/union-budget-2023/india-has-highest-fintech-adoption-rate-gains-3rd-place-in-payments-highlights-economic-survey/97495949

Bhatia, S., & Singh, S. (2024). Exploring financial well-being of working professionals in the Indian context. Journal of Financial Services Marketing, 29, 474–487. https://doi.org/10.1057/s41264-023-00215-x

Bi, Q., Dean, L. R., Guo, T., & Sun, X. (2021). The impact of using financial technology on positive financial behaviors. Financial Services Review, 29(1), 29–54. https://doi.org/10.61190/fsr.v29i1.3442

Business Today. (2024). „Instead of just listening to experts, you can...“: Nithin Kamath introduces Varsity Live, takes stock market education beyond lectures - BusinessToday. https://www.businesstoday.in/india/story/instead-of-just-listening-to-experts-you-can-nithin-kamath-introduces-varsity-live-takes-stock-market-education-beyond-lectures-431097-2024-05-27

Carlin, B. I., Olafsson, A., & Pagel, M. (2019). FinTech and Consumer Financial Well-Being in the Information Age. https://api.semanticscholar.org/CorpusID:209442841

CFPB. (2015). Measuring financial well-being: A guide to using the CFPB Financial Well-Being Scale (December). https://files.consumerfinance.gov/f/201512_%0Acfpb_financial-well-being-user-guide-scale.pdf

De Bassa Scheresberg, C., Hasler, A., & Lusardi, A. (2020). Millennial mobile payment users: A look into their personal finances and financial behavior (ADBI Working Paper No. 1074). https://hdl.handle.net/10419/238431

Dew, J., & Xiao, J. J. (2011). The financial management behavior scale: Development and validation. Journal of Financial Counseling and Planning, 22(1), 43–59. https://ssrn.com/abstract=2061265

French, D., McKillop, D., & Stewart, E. (2020). The effectiveness of smartphone apps in improving financial capability. The European Journal of Finance, 26(4–5), 302–318. https://doi.org/10.1080/1351847X.2019.1639526

Garrett, J. L., Rodermund, R., Anderson, N., Berkowitz, S., & Robb, C. A. (2014). Adoption of Mobile Payment Technology by Consumers. Family and Consumer Sciences Research Journal, 42(4), 358–368. https://doi.org/10.1111/fcsr.12069

Gathergood, J. (2012). Self-control, financial literacy and consumer over-indebtedness. Journal of Economic Psychology, 33(3), 590–602. https://doi.org/10.1016/j.joep.2011.11.006

Gomber, P., Koch, J.-A., & Siering, M. (2017). Digital Finance and FinTech: Current research and future research directions. Journal of Business Economics, 87(5), 537–580. https://doi.org/10.1007/s11573-017-0852-x

Gutter, M., & Copur, Z. (2011). Financial Behaviors and Financial Well-Being of College Students: Evidence from a National Survey. Journal of Family and Economic Issues, 32(4), 699–714. https://doi.org/10.1007/s10834-011-9255-2

Hair, J. F., Black, W. C., Babin, B. J., & Anderson, R. E. (2010). Multivariate Data Analysis (7th ed.). Pearson Education Limited.

Hastings, J. S., Madrian, B. C., & Skimmyhorn, W. L. (2013). Financial literacy, financial education, and economic outcomes. Annual Review of Economics, 5, 347–373. https://doi.org/10.1146/annurev-economics-082312-125807

Hayes, A. F. (2009). Beyond Baron and Kenny: Statistical Mediation Analysis in the New Millennium. Communication Monographs, 76(4), 408–420. https://doi.org/10.1080/03637750903310360

Hayes, A. F. (2017). Introduction to Mediation, Moderation, and Conditional Process Analysis: A Regression-Based Approach. Guilford Publications. www.guilford.com/ebooks

Hayes, A. F., Montoya, A. K., & Rockwood, N. J. (2017). The Analysis of Mechanisms and Their Contingencies: PROCESS versus Structural Equation Modeling. Australasian Marketing Journal, 25(1), 76–81. https://doi.org/10.1016/j.ausmj.2017.02.001

Jager, J., Putnick, D. L., & Bornstein, M. H. (2017). More than Just Convenient: The Scientific Merits of Homogeneous Convenience Samples. Monographs of the Society for Research in Child Development, 82(2), 13–30. https://doi.org/10.1111/mono.12296

Joo, S., & Grable, J. E. (2004). An Exploratory Framework of the Determinants of Financial Satisfaction. Journal of Family and Economic Issues, 25(1), 25–50. https://doi.org/10.1023/B:JEEI.0000016722.37994.9f

Kadoya, Y., Khan, M. S. R., Hamada, T., & Dominguez, A. (2018). Financial literacy and anxiety about life in old age: Evidence from the USA. Review of Economics of the Household, 16(3), 859–878. https://doi.org/10.1007/s11150-017-9401-1

Kakinuma, Y. (2022). Financial literacy and quality of life: A moderated mediation approach of fintech adoption and leisure. International Journal of Social Economics, 49(12), 1713–1726. https://doi.org/10.1108/IJSE-10-2021-0633

Karakara, A. A.-W., Sebu, J., & Dasmani, I. (2022). Financial literacy, financial distress and socioeconomic characteristics of individuals in Ghana. African Journal of Economic and Management Studies, 13(1), 29–48. https://doi.org/10.1108/AJEMS-03-2021-0101

Klapper, L., Lusardi, A., & Panos, G. A. (2013). Financial literacy and its consequences: Evidence from Russia during the financial crisis. Journal of Banking & Finance, 37(10), 3904–3923. https://doi.org/10.1016/j.jbankfin.2013.07.014

Kogler, C., Olsen, J., Kirchler, E., Batrancea, L. M., & Nichita, A. (2023). Perceptions of trust and power are associated with tax compliance: A cross-cultural study. Economic and Political Studies, 11(3), 365–381. https://doi.org/10.1080/20954816.2022.2130501

Kumar, J., Rani, V., Rani, G., & Sarker, T. (2023). Determinants of the financial wellbeing of individuals in an emerging economy: An empirical study. International Journal of Bank Marketing, 41(4), 860–881. https://doi.org/10.1108/IJBM-10-2022-0475

Lee, J. M., Lee, J., & Kim, K. T. (2020). Consumer Financial Well-Being: Knowledge is Not Enough. Journal of Family and Economic Issues, 41(2), 218–228. https://doi.org/10.1007/s10834-019-09649-9

Li, B., Guo, F., Xu, L., & Meng, S. (2024). Fintech business and corporate social responsibility practices. Emerging Markets Review, 59, 101105. https://doi.org/10.1016/j.ememar.2023.101105

Lusardi, A. (2012). Numeracy, financial literacy, and financial decision-making (NBER Working Paper No. 17821).

Lusardi, A., & Messy, F.-A. (2023). The importance of financial literacy and its impact on financial wellbeing. Journal of Financial Literacy and Wellbeing, 1(1), 1–11. https://doi.org/10.1017/flw.2023.8

Lusardi, A., & Mitchell, O. (2011). Financial Literacy and Planning: Implications for Retirement Wellbeing (NBER Working Paper No 17078).

Lusardi, A., & Mitchell, O. S. (2007). Baby Boomer retirement security: The roles of planning, financial literacy, and housing wealth. Journal of Monetary Economics, 54(1), 205–224. https://doi.org/10.1016/j.jmoneco.2006.12.001

Lusardi, A., & Mitchell, O. S. (2008). Planning and financial literacy: How do women fare? American Economic Review, 98(2), 413–417. https://doi.org/10.1257/aer.98.2.413

Mahdzan, N. S., Sabri, M. F., Husniyah, A. R., Magli, A. S., & Chowdhury, N. T. (2023). Digital financial services usage and subjective financial well-being: Evidence from low-income households in Malaysia. International Journal of Bank Marketing, 41(2), 395–427. https://doi.org/10.1108/IJBM-06-2022-0226

Mahdzan, N. S., Zainudin, R., Sukor, M. E. A., Zainir, F., & Wan Ahmad, W. M. (2019). Determinants of Subjective Financial Well-Being Across Three Different Household Income Groups in Malaysia. Social Indicators Research, 146(3), 699–726. https://doi.org/10.1007/s11205-019-02138-4

Meyll, T., & Walter, A. (2019). Tapping and waving to debt: Mobile payments and credit card behavior. Finance Research Letters, 28, 381–387. https://doi.org/10.1016/j.frl.2018.06.009

Migozzi, J., Urban, M., & Wójcik, D. (2023). „You should do what India does“: FinTech ecosystems in India reshaping the geography of finance. Geoforum, 103720. https://doi.org/10.1016/j.geoforum.2023.103720

Muttar, A. K., Alansari, S., Aldulaimi, S., Abdeldayem, M., & AlKubaisi, M. (2021). New Paradigm of Behavioral Finance in Islamic Banks: The Role of Leadership to Facilitate Creative Behavior. 2021 International Conference on Sustainable Islamic Business and Finance, 1–7. https://doi.org/10.1109/IEEECONF53626.2021.9686314

NCFE. (2019). Financial Literacy and Inclusion in India: Final Report on the Survey Results. National Centre for Financial Education.

Netemeyer, R. G., Warmath, D., Fernandes, D., & Lynch, J. G. (2018). How Am I Doing? Perceived Financial Well-Being, Its Potential Antecedents, and Its Relation to Overall Well-Being. Journal of Consumer Research, 45(1), 68–89. https://doi.org/10.1093/jcr/ucx109

OECD. (2020). Recommendation of the Council on financial literacy (OECD/LEGAL/0461) - OECD Legal Instruments. https://legalinstruments.oecd.org/en/instruments/OECD-LEGAL-0461

Ooi, K.-B., Cham, T.-H., Tan, G. W.-H., Al-Emran, M., & Tang, Y.-C. (2024). Guest editorial: The dark side of FinTech: unintended consequences and ethical consideration of FinTech adoption. International Journal of Bank Marketing, 42(1), 1–6. https://doi.org/10.1108/IJBM-02-2024-619

Ozili, P. K. (2023). The acceptable R-square in empirical modelling for social science research. Social Research Methodology and Publishing Results: A Guide to Non-Native English Speakers, 115769, 134–143. https://doi.org/10.4018/978-1-6684-6859-3.ch009

Panos, G. A., & Wilson, J. O. S. (2020). Financial literacy and responsible finance in the FinTech era: Capabilities and challenges. European Journal of Finance, 26(4–5), 297–301. https://doi.org/10.1080/1351847X.2020.1717569

Philippas, N. D., & Avdoulas, C. (2020). Financial literacy and financial well-being among generation-Z university students: Evidence from Greece. European Journal of Finance, 26(4–5), 360–381. https://doi.org/10.1080/1351847X.2019.1701512

Powell, R., Do, A., Gengatharen, D., Yong, J., & Gengatharen, R. (2023). The relationship between responsible financial behaviours and financial wellbeing: The case of buy‐now‐pay‐later. Accounting & Finance, 63(4), 4431–4451. https://doi.org/10.1111/acfi.13100

Rahman, M., Isa, C. R., Masud, M. M., Sarker, M., & Chowdhury, N. T. (2021). The role of financial behaviour, financial literacy, and financial stress in explaining the financial well-being of B40 group in Malaysia. Future Business Journal, 7(1), 1–18. https://doi.org/10.1186/s43093-021-00099-0

Rahman, S. A., Didarul Alam, M. M., & Taghizadeh, S. K. (2020). Do mobile financial services ensure the subjective well-being of micro-entrepreneurs? An investigation applying UTAUT2 model. Information Technology for Development, 26(2), 421–444. https://doi.org/10.1080/02681102.2019.1643278

Relja, R., Ward, P., & Zhao, A. L. (2024). Understanding the psychological determinants of buy-now-pay-later (BNPL) in the UK: A user perspective. International Journal of Bank Marketing, 42(1), 7–37. https://doi.org/10.1108/IJBM-07-2022-0324

Rey-Ares, L., Fernández-López, S., & Álvarez-Espiño, M. (2024). The role of financial literacy in consumer financial fraud exposure (via email) and victimisation: Evidence from Spain. International Journal of Bank Marketing, 42(6), 388–1413. https://doi.org/10.1108/IJBM-03-2023-0169

Riitsalu, L., & Murakas, R. (2019). Subjective financial knowledge, prudent behaviour and income. International Journal of Bank Marketing, 37(4), 934–950. https://doi.org/10.1108/IJBM-03-2018-0071

Robb, C. A., Babiarz, P., & Woodyard, A. (2012). The demand for financial professionals’ advice: The role of financial knowledge, satisfaction, and confidence. Financial Services Review, 21(21), 291–305.

Sabri, M. F., Anthony, M., Law, S. H., Rahim, H. A., Burhan, N. A. S., & Ithnin, M. (2023). Impact of financial behaviour on financial well-being: Evidence among young adults in Malaysia. Journal of Financial Services Marketing, 29, 788–807. https://doi.org/10.1057/s41264-023-00234-8

Salampasis, D., & Mention, A.-L. (2018). FinTech: Harnessing Innovation for Financial Inclusion. In Handbook of Blockchain, Digital Finance, and Inclusion, Volume 2 (pp. 451–461). Elsevier. https://doi.org/10.1016/B978-0-12-812282-2.00018-8

Shah, M. U. D., Khan, I. U., & Khan, N. U. (2024). The role of digital payments in overspending behavior: A mental accounting perspective. International Journal of Emerging Markets, ahead of print. https://doi.org/10.1108/IJOEM-08-2023-1313

Shehadeh, M., Abu-AlSondos, I. A., Ajouz, M., Aldulaimi, S. H., Atta, A. A. B., & Abdeldayem, M. (2024). Digital Transformation and its Implications for the Future of Financial Intermediation in Islamic Institutions. 2024 ASU International Conference in Emerging Technologies for Sustainability and Intelligent Systems (ICETSIS), 130–134. https://doi.org/10.1109/ICETSIS61505.2024.10459524

Tahir, M. S., Ahmed, A. D., & Richards, D. W. (2021). Financial literacy and financial well-being of Australian consumers: A moderated mediation model of impulsivity and financial capability. International Journal of Bank Marketing, 39(7), 1377–1394. https://doi.org/10.1108/IJBM-09-2020-0490

Thakor, A. V. (2020). Fintech and banking: What do we know? Journal of Financial Intermediation, 41, 100833. https://doi.org/10.1016/j.jfi.2019.100833

Utkarsh, Pandey, A., Ashta, A., Spiegelman, E., & Sutan, A. (2020). Catch Them Young: Impact of financial socialisation, financial literacy and attitude towards money on financial well-being of young adults. International Journal of Consumer Studies, 44(6), 531–541. https://doi.org/10.1111/ijcs.12583

van Rooij, M. C. J., Lusardi, A., & Alessie, R. J. M. (2012). Financial Literacy, Retirement Planning and Household Wealth. The Economic Journal, 122(560), 449–478. https://doi.org/10.1111/j.1468-0297.2012.02501.x

Walsh, B., & Lim, H. (2020). Millennials’ adoption of personal financial management ( PFM ) technology and financial behavior. Financial Planning Review, 3(3), 1–17. https://doi.org/10.1002/cfp2.1095

Xiao, J. J. (2008). Applying Behavior Theories to Financial Behavior. In Handbook of Consumer Finance Research (pp. 69–81). Springer New York. https://doi.org/10.1007/978-0-387-75734-6_5

Yoo, J. H., & Fisher, P. J. (2017). Mobile Financial Technology and Consumers’ Financial Capability in the United States. Journal of Education & Social Policy, 7(1), 80–93.

Yue, P., Korkmaz, A. G., Yin, Z., & Zhou, H. (2022). The rise of digital finance: Financial inclusion or debt trap? Finance Research Letters, 47, 102604. https://doi.org/10.1016/j.frl.2021.102604

Zhang, Y., & Fan, L. (2023). An Examination of Mobile Fintech Utilization From a Stress-Coping Perspective. Journal of Financial Counseling and Planning, 34(3), 354–366. https://doi.org/10.1891/JFCP-2022-0061

Zhang, Y., & Fan, L. (2024). The nexus of financial education, literacy and mobile fintech: Unraveling pathways to financial well-being. International Journal of Bank Marketing, 42(7), 1789–1812. https://doi.org/10.1108/IJBM-09-2023-0531