Organizations and Markets in Emerging Economies ISSN 2029-4581 eISSN 2345-0037

2025, vol. 16, no. 2(33), pp. 246–269 DOI: https://doi.org/10.15388/omee.2025.16.10

The Role of Green Financial Instruments, Monetary Policy, and Foreign Direct Investment in Promoting Sustainable Development in Developing ASEAN Countries

Ezri Chen Eunike Mendrofa

Universitas Sriwijaya, Indonesia

ezrimendrofa@gmail.com

https://orcid.org/0009-0002-5739-7320

https://ror.org/030bmb197

Sri Andaiyani (corresponding author)

Universitas Sriwijaya, Indonesia

sriandaiyani@fe.unsri.ac.id

https://orcid.org/0000-0002-4275-0059

https://ror.org/030bmb197

Abstract: The global focus on sustainable development intensified with the introduction of the Sustainable Development Goals (SDGs) in 2015, with the primary aim of balancing economic growth, social well-being, and environmental responsibility. This research explores how green bonds, interest rate policies, and foreign direct investment (FDI) contribute to the progress of SDGs in four developing ASEAN nations: Indonesia, Malaysia, the Philippines, and Thailand. Using quarterly data from 2018 to 2023, the study applies the Panel Vector Error Correction Model (PVECM) to uncover the dynamics at work. The findings reveal that green bonds and foreign direct investment have a notable and positive effect on the SDG index in both the short and long term. On the other hand, the impact of policy interest rates is negative, though statistically insignificant, particularly when rates are high. These results provide valuable guidance for policymakers seeking to enhance the effectiveness of financial tools and investments in driving sustainable development. Furthermore, the study stresses the importance of well-rounded policy frameworks that integrate economic, social, and environmental objectives. Theoretically, this study contributes to the refinement of Ecological Modernization Theory by empirically demonstrating how green financing and FDI serve as pivotal instruments in advancing sustainable development within emerging ASEAN economies.

Keywords: SDGs, green bonds, foreign direct investment (FDI), policy interest rates

Received: 7/2/2025. Accepted: 20/10/2025

Copyright © 2025 Ezri Chen Eunike Mendrofa, Sri Andaiyani. Published by Vilnius University Press. This is an Open Access article distributed under the terms of the Creative Commons Attribution Licence, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

1. Introduction

Since the United Nations established the Sustainable Development Goals (SDGs) in 2015, sustainable development has become a cornerstone of global discourse. Achieving these goals demands a delicate balance between fostering economic growth, improving social welfare, and protecting the environment to ensure a prosperous future for generations. However, Southeast Asian developing nations face substantial challenges in reconciling economic expansion with environmental preservation, particularly in meeting the ambitious 2030 SDG targets (Holzhacker & Agussalim, 2019; Mahmood et al., 2023).

This research seeks to address the question: What role do economic tools such as green bonds, interest rate policies, and foreign direct investment (FDI) play in overcoming these challenges and advancing the SDG agenda in developing ASEAN countries? By focusing on Indonesia, Malaysia, the Philippines, and Thailand, which exhibit diverse economic landscapes and policy approaches, this study provides a comparative perspective on the interplay between financial instruments and sustainable development. These four countries were selected primarily because they represent a significant portion of the economic output of ASEAN and have shown a growing commitment to sustainable development. Moreover, they are among the few ASEAN nations with relatively complete and accessible quarterly data on green bonds, FDI, and policy interest rates. Although the ideal scope would encompass all developing ASEAN nations, data limitations particularly the unavailability and inconsistency of green bond data in other ASEAN members such as Vietnam, Cambodia, and Laos necessitated a focus on these four countries. This ensures analytical rigor while still offering insights applicable to broader ASEAN contexts.

The study period of 2018–2023 was chosen to capture recent developments in sustainable finance and policy shifts. While this may appear short for long-term panel analysis, it reflects the period when green bonds began gaining traction in ASEAN, allowing this research to capture the initial dynamics of their integration into sustainable development frameworks. Expanding the dataset was constrained by the limited historical availability of green bond issuance data, a common challenge in emerging markets.

The hypothesis of this study posits that green bonds and FDI have a significant positive impact on SDG attainment, while interest rate policies, if misaligned, may exert negligible or even adverse effects. This proposition is motivated by the transformative potential of green financial instruments and FDI, as identified in the research (Azhgaliyeva et al., 2020; Ye & Rasoulinezhad, 2023). However, the specific roles of these tools in developing ASEAN nations remain underexplored. Furthermore, the macroeconomic impacts of interest rate policies in balancing growth and sustainability require deeper investigation.

Theoretically, this study builds upon the framework of sustainable development, which emphasizes the integration of economic, social, and environmental goals. Green bonds are designed to fund environmentally friendly projects, facilitating renewable energy investments and climate action (Zhao et al., 2022). FDI promotes sustainable development by enhancing production capacities and transferring green technologies (Yousaf et al., 2020). Meanwhile, interest rate policies shape macroeconomic conditions, influencing investments in green sectors (Mohsen et al., 2022). By integrating these theoretical lenses, this study offers a nuanced understanding of how financial instruments and macroeconomic policies intersect with sustainable development goals in unique institutional and socio-economic contexts of ASEAN.

The SDG index used in this study is a composite measure encompassing the 17 goals outlined by the United Nations. Recognizing its multidimensional nature, we acknowledge that economic tools such as green bonds, FDI, and interest rate policies may influence different SDG goals in varying degrees. However, the use of a composite index is justified on two grounds: first, it allows for a holistic assessment of sustainable development progress in alignment with global benchmarks; and second, it facilitates comparative cross-country analysis within the ASEAN context. Although a disaggregated analysis of each SDG goal would offer deeper granularity, data constraints and methodological consistency necessitate the use of an aggregate index. Future research is encouraged to explore the differentiated effects of economic instruments on individual SDG components.

Methodologically, this study employs a Panel Vector Error Correction Model (PVECM) to capture the short- and long-term dynamics between green bonds, interest rate policies, FDI, and SDG indices using quarterly data from 2018 to 2023. Preliminary findings suggest that green bonds and FDI exert significant positive effects on the SDG index, while the impact of interest rate policies is statistically insignificant, particularly when rates are high.

This research makes a novel contribution by providing empirical evidence on the nexus between financial instruments, monetary policies, and sustainable development in developing ASEAN countries. Unlike prior studies that predominantly focus on developed economies or global trends, this research contextualizes its findings within the socio-economic and environmental dynamics of ASEAN. It addresses a significant research gap by highlighting how green bonds and FDI cornerstones of modern sustainable finance function within the emerging markets of the ASEAN bloc, where institutional capacities and policy landscapes differ from those of developed nations. By identifying specific policy implications, this study bridges the gap in understanding the potential of economic tools in aligning with SDG targets, offering actionable recommendations tailored to the challenges and opportunities faced by the ASEAN nations.

2. Literature Review

The realization of sustainable development is shaped by the intricate interplay between economic, social, and environmental factors. Numerous elements can either accelerate or impede a nation’s progress in achieving the Sustainable Development Goals (SDGs), ultimately determining how effectively the country reaches these objectives.

2.1 Key Determinants of Sustainable Development

Younis and Chaudhary (2020) identified key factors that serve as transmission channels for sustainable development, including institutional quality, technological advancement, globalization, and social inclusivity. Furthermore, Singh and Kumar (2022) emphasized that key factors like foreign direct investment inflows, capital investment, GDP per capita, employment rates, labor force participation, adoption of renewable energy, green technologies, high-tech exports, ICT products, and investments in research and development are crucial in fostering economic, social, and environmental progress. Together, these factors fuel innovation in science and technology, which is vital for achieving sustainable development.

Additionally, Mun et al. (2023) highlighted that governance and institutional quality are critical determinants of sustainable development. In high-income countries, this factor is supported by capital investments, fiscal expansion, and the enforcement of democracy. In middle-income countries, governance effectiveness plays a significant role, while in low-income nations, fiscal spending and sound institutions are pivotal in supporting sustainability. Borowski and Patuk (2021) revealed that environmental, social, and economic factors, such as age composition, CO2 emissions, renewable energy, and natural resource depletion, also influence sustainable development achievements. In the ASEAN context, Sadiq et al. (2023) noted that environmental, social, and governance factors, as well as economic growth, positively impact the progress of ASEAN countries on sustainable development goals.

While these studies underscore the multidimensionality of sustainable development, this research uses a composite SDG index as a practical and widely adopted proxy for tracking overall progress. We acknowledge that different economic tools may influence specific SDG goals differently. However, due to data availability and methodological constraints, the use of a composite index enables a more consistent and holistic cross-country comparison. This approach aligns with prior empirical studies using aggregated SDG metrics, while offering the scope for future disaggregated analyses on g oal-specific impacts.

2.2 Green Finance and Green Bonds

In this context, green finance emerges as a key element in achieving sustainable development goals (SDGs) by channeling investments into environmentally friendly projects and technologies (Kwilinski et al., 2023). A study by Xiong and Dai (2023) demonstrated that green finance positively impacts sustainable development and negatively affects pollution levels. Ronaldo and Suryanto (2022) noted that green finance serves as a catalyst for green technology innovation and the growth of green-focused micro-enterprises, helping to achieve both environmental and economic sustainability goals. Nevertheless, its influence on sustainable development differs between regions, highlighting the need for region-specific policies and alternative funding mechanisms like green bonds (Kwilinski et al., 2023).

Green bonds play a significant role in achieving SDGs by directing funds toward environmentally friendly projects (Bisultanova, 2023). Research conducted by Alamgir and Cheng (2023) and Rasoulinezhad and Taghizadeh-Hesary (2022) revealed that green bonds significantly reduce carbon emissions and support renewable energy production, thereby facilitating SDG achievements. Similarly, Ahmed et al. (2024) observed positive abnormal stock returns following green bond announcements, reflecting investor support for climate action.

However, Sinha et al. (2021) argued that green bond financing might negatively impact environmental and social responsibility, suggesting that it does not directly contribute to achieving SDGs. This concern is further elucidated by Kwilinski et al. (2023), who noted that while green finance and green bonds generally contribute positively to sustainable development, potential adverse effects, such as resource diversion, greenwashing risks, negative impacts on economic growth, and negative spillover effects, must be considered.

Recent studies have examined the development of green bonds in ASEAN countries, highlighting their growing importance for financing renewable energy and energy efficiency projects (Azhgaliyeva et al., 2020). While green bonds have gained traction, particularly in issuance of green bonds in top three green bond issuing countries in ASEAN (Indonesia, Malaysia, and Singapore), regulatory challenges and market immaturity still limit their full potential.

2.3 Monetary Policy and Sustainable Development

Many researchers have investigated how monetary policy influences the progress toward achieving sustainable development goals. Chuba and Yusuf (2022) highlighted that policy interest rates play a crucial role in influencing economic growth and the achievement of SDGs. Specifically, expansionary monetary policies—those that increase the money supply and reduce interest rates—have been shown to support progress toward sustainable development goals. For example, Isibor et al. (2023) demonstrated in the case of Nigeria that monetary policy tools such as interest rate adjustments, inflation management, and money supply regulation can effectively help countries achieve sustainable economic growth.

2.4 Foreign Direct Investment (FDI) and Sustainable Development

Foreign Direct Investment (FDI) is crucial for advancing the achievement of the Sustainable Development Goals (SDGs). According to Aust et al. (2020), FDI positively influences SDG scores, particularly in areas such as infrastructure, water, sanitation, and renewable energy. Venâncio and Pinto (2020) added that by enhancing access to capital and knowledge, FDI positively contributes to SDG attainment, underscoring the importance of foreign investment in driving sustainable and inclusive growth.

Azam et al. (2022) demonstrated that foreign direct investment (FDI) and economic growth are pivotal in strengthening the connection between institutional market quality and sustainable development. Dhahri and Omri (2020) further highlighted that FDI, along with specific forms of foreign aid, contributes positively to reducing poverty and improving food security in developing nations by enhancing agricultural output. Conversely, FDI is not without drawbacks; it can also lead to adverse environmental outcomes. Singhania and Saini (2021) observed that in developing economies, FDI significantly exacerbates environmental degradation, posing challenges to the realization of sustainable development goals.

2.5 Synthesis and Research Gap

The literature consistently underscores the importance of green finance, FDI, and monetary policy as critical tools for sustainable development. While there is general agreement that green finance and FDI positively influence SDGs, concerns around governance, environmental risks, and policy misalignment persist. Notably, prior research has predominantly focused on either developed economies or specific sectors within ASEAN. Few studies comprehensively examine the dynamic interplay between green bonds, monetary policy, and FDI within the ASEAN context using robust econometric models.

Moreover, existing studies often rely on annual data, limiting insights into short-term dynamics. This study addresses these gaps by employing a PVECM approach with quarterly data (2018–2023) to capture both short-term and long-term effects, providing novel insights into the financial mechanisms that drive sustainable development in developing ASEAN nations. By doing so, it contributes to both theory by reinforcing the relevance of Ecological Modernization Theory and practice, offering policy-relevant findings tailored to the ASEAN context.

3. Methodology and Data

This study employs the Panel Vector Error Correction Model (PVECM) to explore the relationship between green financial tools, such as green bonds, policy interest rates, and foreign direct investment (FDI) in relation to the Sustainable Development Goals (SDGs) index in four ASEAN countries: Indonesia, Malaysia, the Philippines, and Thailand. The PVECM method is ideal for this analysis as it captures short-term interactions while also providing valuable insights into how the system adjusts toward long-term stability. This approach enables a thorough examination of how various interconnected macroeconomic factors influence one another.

The initial phase of the analysis entails performing a unit root test to verify that the data is stationary, a necessary step to prevent inaccurate conclusions from spurious regressions. Once stationarity is confirmed, the Johansen cointegration test is applied to identify any long-term relationships between the green bonds, policy interest rates, FDI, and the SDGs index, which supports the use of the Vector Error Correction Model. To determine the optimal number of lags, criteria such as the Akaike Information Criterion (AIC) and the Schwarz Bayesian Criterion (SBC) are used, resulting in a lag length of four, which ensures that the model effectively captures the influence of past data.

Next, the PVECM is designed to capture both the short-term dynamics and the long-term corrections between these variables. The error correction term (ECT) in the model quantifies the speed at which the system returns to equilibrium after short-term disturbances, providing insight into the dynamics of economic stability. Additionally, this study incorporates Impulse Response Function (IRF) analysis to track how shocks in one variable affect the system over time and influence other factors.

The data for this research are obtained from reliable sources: green bond information is derived from Asian Bonds Online, policy interest rates are gathered from the BIS Data Portal, FDI figures are sourced from Trading Economics, and the SDGs index is retrieved from the SDGs Transformation Centre. The SDGs index was chosen because it provides a comprehensive and aggregated measure of sustainable development performance, encompassing 17 key goals that reflect economic, social, and environmental progress. This index captures multidimensional aspects of development and aligns with the theoretical framework of the Sustainable Development Theory, which emphasizes the interconnectedness of these dimensions (Diaz-Sarachaga et al., 2018). Therefore, it serves as an appropriate dependent variable to assess how financial instruments and macroeconomic policies influence holistic sustainable outcomes.

Regarding the independent variables, green bonds represent the commitment to financing environmentally friendly projects and are grounded in Ecological Modernization Theory (Mol et al., 2013), which posits that financial mechanisms can effectively drive environmental improvements. FDI is incorporated based on the theories of Development Economics, particularly the idea that foreign capital enhances production capacity and facilitates technology transfer (Mei, 2023). Interest rate policy, a fundamental tool in Monetary Theory, has a hysterical impact on macroeconomic investment under both certainty and uncertainty, affecting the effectiveness of central bank policy (Belke & Göcke, 2019). These theoretical underpinnings justify the selection of variables and their expected interactions with sustainable development outcomes.

As the SDGs index is available only annually, linear interpolation was performed to convert it into quarterly data, ensuring consistency with the frequency of the other variables. This interpolation was necessary because the PVECM framework requires balanced panel data with consistent time intervals to produce valid estimations. While interpolating annual data into quarterly data introduces the risk of smoothing out actual fluctuations and may potentially bias short-term dynamics (Chen & Andrews, 2008), it allows the model to capture temporal interactions across variables on a more granular level. The decision to use linear interpolation follows established practices in time series analysis, where higher-frequency data is needed to align variables (Friedman, 1962). To mitigate risks, we ensured that the interpolation process preserved long-term trends and carefully interpreted short-term results with caution, acknowledging this limitation as part of the study’s robustness assessment. These steps, combined with the chosen lag length of four, ensure the robustness and comprehensiveness of the PVECM analysis in capturing the dynamic interplay between the variables under study.

This study utilizes the Panel Vector Error Correction Model (PVECM) to explore the relationships and interactions between various variables within a panel data setting. The PVECM is a robust econometric technique that effectively analyzes both the short-term variations and long-term equilibrium connections among variables that are interrelated. This method is particularly well-suited for analyzing scenarios where variables influence one another and demonstrate the potential for sustained long-run connections. The PVECM integrates the features of Vector Autoregression (VAR) for short-term dynamics and error correction for modeling long-term adjustments, making it a relevant approach for this study. In the context of this study, the equation is specified as:

In this equation:

• ΔSDGiit represents the first difference of the SDG index, indicating the changes in sustainable development outcomes for country iii at time ttt. This serves as the dependent variable.

• αi is the country-specific fixed effect, accounting for unobserved heterogeneities across countries in the panel.

•  captures the short-term effects of lagged changes in the SDG index itself.

captures the short-term effects of lagged changes in the SDG index itself.

•  represents the short-term effects of lagged changes in the natural logarithm of green bonds issued.

represents the short-term effects of lagged changes in the natural logarithm of green bonds issued.

•  measures the short-term effects of lagged changes in interest rates.

measures the short-term effects of lagged changes in interest rates.

•  captures the short-term effects of lagged changes in the natural logarithm of foreign direct investment.

captures the short-term effects of lagged changes in the natural logarithm of foreign direct investment.

• Π is the error correction term coefficient, quantifying the speed of adjustment toward the long-term equilibrium relationship.

• ECTi, t–1 is the error correction term, derived from the cointegration equation, which measures deviations from the long-term equilibrium in the previous period.

• ϵitt is the error term, accounting for unexplained variations in the dependent variable.

This equation captures the core of the PVECM framework, where the short-term behavior of the SDG index is shaped by its lagged changes along with the variations in the independent variables (green bonds, interest rates, and FDI). Moreover, the incorporation of the error correction term guarantees that any deviations from the long-term balance are progressively corrected over time.

The PVECM is ideally suited for this analysis because it allows for modeling the interrelationships between variables within a panel data structure. By incorporating both short-term fluctuations and long-term trends, this approach offers a robust framework to explore how financial instruments like green bonds interact with macroeconomic factors and influence sustainable development. The error correction term ECTi,t–1 plays a vital role in this process as it measures how swiftly and effectively the system adjusts back to its equilibrium after experiencing a short-term disruption. This combined emphasis on both immediate interactions and long-term corrections makes PVECM an invaluable tool for exploring the intricate dynamics between financial and economic elements in the pursuit of sustainability.

4. Results and Discussion

4.1 Results

This study investigates how green bonds, policy interest rates, and foreign direct investment (FDI) influence the achievement of Sustainable Development Goals (SDGs) in Indonesia, Malaysia, the Philippines, and Thailand, using quarterly data spanning from 2018 to 2023. The analysis employs the Panel Vector Error Correction Model (PVECM) to explore both the short-term relationships and the long-term adjustments between these variables, providing a comprehensive view of their interconnected dynamics.

The initial phase of the analysis involves performing descriptive statistical assessments to better understand the distribution and features of the variables being examined. This step helps uncover patterns in the data, determine the central tendencies, and assess the variability of each variable green bonds, policy interest rates, FDI, and the SDG index. Descriptive statistics, including the mean, maximum, minimum, and standard deviation, are computed for each quarter over the 2018–2023 period. These preliminary results offer valuable insights into the role of each variable in driving sustainability and highlight how their interactions may impact progress toward achieving the SDGs. A summary of these descriptive statistics is presented in Table 1.

Table 1

Descriptive Statistical Test Results

|

SDGI |

GB |

IR |

FDI |

|

|---|---|---|---|---|

|

Mean |

69.21250 |

7.650430 |

3.062500 |

20.39052 |

|

Median |

68.32344 |

7.570602 |

3.000000 |

21.44028 |

|

Maximum |

74.85000 |

9.150897 |

6.500000 |

23.25988 |

|

Minimum |

65.23438 |

6.155441 |

0.500000 |

15.78281 |

|

Std. Dev. |

2.801797 |

0.656295 |

1.687025 |

2.564713 |

Table 1 displays the descriptive statistics, offering insights into the distribution of each variable in the study. From the analysis, the Sustainable Development Goals Index (SDGI) has an average of 69.21 and a standard deviation of 2.80, indicating a relatively tight dispersion around the mean. The median value closely aligns with the mean, suggesting a symmetric data distribution. The SDGI range spans from 65.23 to 74.85, reflecting moderate variability.

The Green Bond (GB) variable shows an average value of 7.65 and a median of 7.57, nearly identical, which points to a balanced distribution. The highest value recorded is 9.15, with a minimum of 6.16, and a standard deviation of 0.66, indicating relatively low fluctuation in the green bond market during the period. For the Interest Rate (IR) variable, the mean stands at 3.06, with a larger standard deviation of 1.68, suggesting more variation. The range of interest rates spans from 0.5 to 6.5, highlighting considerable fluctuations.

Regarding Foreign Direct Investment (FDI), the average is 20.39, while the median of 21.44 suggests a slight left skew. The highest value of FDI is 23.26, with a minimum of 15.78, and a standard deviation of 2.56, indicating moderate variation in investment levels, which may reflect the changing attractiveness of these countries to foreign investors over time. Overall, this initial descriptive analysis provides a clear picture of the data distribution, offering a solid foundation for the more advanced analyses to follow.

After conducting the descriptive statistics, the study advanced to the Panel Vector Error Correction Model (PVECM) approach, beginning with a unit root test to verify the stationarity of the data, ensuring that non-stationary data did not lead to misleading results.

Table 2

Unit Root Test Results

|

Variable |

Level |

1st Diference |

2nd diference |

|---|---|---|---|

|

Index SDG |

0.9689 |

0.3179 |

0.0002*** |

|

Green Bond |

0.8513 |

0.0000*** |

0.0000*** |

|

Suku Bunga Kebijakan |

0.3769 |

0.0988* |

0.0000*** |

|

FDI |

0.0001*** |

0.0000*** |

0.0000*** |

Note. * = a 10% significance level. ** = a 5% significance level. *** = a 1% significance level.

The results of the Augmented Dickey-Fuller (ADF) test for stationarity reveal that, at the initial level, only the FDI variable is stationary at a 1% significance level, while the SDGI, GB, and IR variables exhibit non-stationarity. Following first differencing, both GB and IR become stationary at a 1% significance level, with IR also becoming stationary at a 10% level. However, the SDGI index remains non-stationary. After performing second differencing, all variables achieve stationarity at a 1% significance level, confirming they are free from unit root problems and are appropriate for further analysis. The subsequent stage of the analysis focuses on estimating the model using data that has been transformed through second-order differencing.

Additionally, a lag selection procedure was carried out to identify the optimal lag length using the Akaike Information Criterion (AIC). Proper lag selection is crucial to ensure that the model accurately reflects the dynamics between variables while avoiding issues such as overfitting or underfitting.

Table 3

Optimum Lag Test Results

|

Lag |

LogL |

LR |

FPE |

AIC |

SC |

HQ |

|---|---|---|---|---|---|---|

|

0 |

-58.34020 |

NA |

9.39e-05 |

2.078007 |

2.217630 |

2.132621 |

|

1 |

-19.07197 |

71.99175 |

4.33e-05 |

1.302399 |

2.000514* |

1.575470 |

|

2 |

7.365721 |

44.94408 |

3.08e-05 |

0.954476 |

2.211083 |

1.446004 |

|

3 |

30.95989 |

36.96420 |

2.44e-05 |

0.701337 |

2.516436 |

1.411322 |

|

4 |

59.44831 |

40.83339* |

1.67e-05* |

0.285056* |

2.658647 |

1.213498* |

|

5 |

70.30722 |

14.11659 |

2.10e-05 |

0.456426 |

3.388508 |

1.603325 |

|

6 |

76.48710 |

7.209857 |

3.19e-05 |

0.783763 |

4.274338 |

2.149119 |

|

7 |

100.7972 |

25.12047 |

2.77e-05 |

0.506759 |

4.555825 |

2.090571 |

In time series econometrics, it is essential to ensure that all variables are stationary, particularly at the I(0) level, to avoid spurious regression results and invalid statistical inference. Since the PVECM framework assumes that the first differences of the variables are stationary and that there exist stable long-run relationships among them, transforming the variables into I(0) was necessary. By applying second-order differencing, the analysis meets the stationarity requirement, ensuring that the dynamic interactions captured in the PVECM are valid and reliable.

The lag selection test suggests that Lag 4 is the most appropriate for this analysis, as indicated by the Akaike Information Criterion (AIC). With Lag 4, the model demonstrates a marked enhancement in its ability to explain the data and exhibits the smallest prediction error. This is marked by the presence of an asterisk (*) in the LR test and other criteria, indicating that Lag 4 provides statistically significant results compared to other lags. Furthermore, the model at Lag 4 achieves an optimal balance between data fit and model complexity. Consequently, Lag 4 is chosen as the ideal lag for estimating the VAR or VECM model, guaranteeing a reliable, precise, and effective analysis.

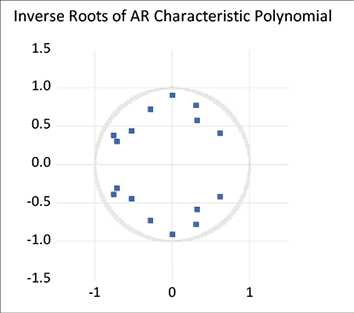

The following step involves conducting the VAR stability test. A VAR model is deemed stable if the roots of its characteristic polynomial fall within the unit circle. When stability is achieved, any shocks within the system will gradually fade, enabling reliable impulse response analysis and variance decomposition. Conversely, an unstable VAR model may produce unreliable estimates, complicating the interpretation of results and possibly leading to misleading conclusions.

Figure 1

VAR Stability Test Results

Based on Figure 1, all polynomial roots lie inside the unit circle (with a modulus less than one), indicating that the VAR model satisfies the stability condition. This means that any shocks occurring within the system will dissipate over time, allowing the variables to gradually return to their equilibrium levels. Consequently, the model is deemed stable, and the subsequent analysis can proceed reliably.

Following the stability verification, the next step involves examining whether one or more cointegration relationships exist among the variables using the Johansen Cointegration Test. The presence of cointegration suggests that the variables share a long-term equilibrium relationship. In this case, the Panel Vector Error Correction Model (PVECM) is more appropriate than the Panel VAR (PVAR) model as it captures both the short-term dynamics and the long-term adjustments inherent in the system.

Table 4

Cointegration Test Results

|

Hypothesized |

Eigenvalue |

Trace Statistic |

0.05 |

Prob. ** |

|

None |

0.558618 |

148.0854 |

47.85613 |

0.0000 |

|

At most 1 * |

0.427247 |

92.47193 |

29.79707 |

0.0000 |

|

At most 2 * |

0.395411 |

54.57547 |

15.49471 |

0.0000 |

|

At most 3 * |

0.258718 |

20.35746 |

3.841465 |

0.0000 |

Based on the cointegration test results, a significant long-term relationship among the variables was identified. This is indicated by a trace statistic value of 148.0854, which exceeds the critical value of 47.85613 at a 5% significance level, with a probability of 0.0000. The results clearly demonstrate a significant and enduring connection among the variables, highlighting their long-term relationship. Therefore, the most appropriate method for further analysis is the P-VECM.

Table 5

P-VECM Estimation Results in the Long Run

|

Variable |

Coefficient |

T-stastistic |

|---|---|---|

|

Green Bond |

3.034390 |

5.44482 |

|

Policy Interest Rate |

-0.025476 |

-0.19532 |

|

FDI |

0.276932 |

3.25907 |

Table 4 presents the results of the long-term analysis using the PVECM. The Green Bond variable exhibits a positive coefficient of 4.03, with a T-statistic of 5.44, surpassing the critical T-value of 1.986. This indicates a strong and statistically meaningful positive association between Green Bonds and the SDG index in the long run, suggesting that an increase in green bond issuance generally contributes to the progress of sustainable development goals.

On the other hand, the Policy Interest Rate variable shows a negative coefficient of -0.025 and a T-statistic that falls below the critical value of 1.986. This suggests a negative yet statistically inconclusive relationship with the SDG index over the long term. In other words, while higher interest rates could slow down the achievement of sustainable development goals, the effect is not deemed statistically relevant.

As for Foreign Direct Investment (FDI), the coefficient is 3.259, with a T-statistic exceeding the critical value of 1.986. This points to a positive and meaningful link between FDI and the SDG index, implying that greater foreign investment is associated with improved progress toward achieving sustainable development goals.

Table 6

P-VECM Estimation Results in the Short Run

|

Variable |

Coefficient |

T-stastistic |

|---|---|---|

|

SDGs Index(-1),4 |

-0.418612 |

-3.42086 |

|

SDGs Index(-2),4 |

-0.360650 |

-2.78660 |

|

SDGs Index(-3),4 |

-0.169643 |

-1.31340 |

|

SDGs Index(-4),4 |

-0.280173 |

-2.86559 |

|

Green Bond (-1),4 |

0.618210 |

2.81659 |

|

Green Bond (-2),4 |

0.497177 |

2.85686 |

|

Green Bond (-3),4 |

0.398723 |

3.25166 |

|

Green Bond (-4),4 |

0.007700 |

0.10652 |

|

Policy Interest Rate (-1),4 |

-0.016535 |

-0.74387 |

|

Policy Interest Rate (-2),4 |

-0.009744 |

-0.36803 |

|

Policy Interest Rate (-3),4 |

-0.016717 |

-0.60674 |

|

Policy Interest Rate (-4),4 |

-0.023913 |

-0.95439 |

|

FDI (-1),4 |

0.064331 |

3.01594 |

|

FDI (-2),4 |

0.046663 |

2.63465 |

|

FDI (-3),4 |

0.031148 |

2.40679 |

|

FDI (-4),4 |

0.016005 |

2.14984 |

Based on the results of the short-term PVECM analysis, the SDG index from previous periods (lags -1, -2, and -4) has significant negative coefficients of -0.418612, -0.360650, and -0.280173, with t-statistic values of -3.42086, -2.78660, and -2.86559, all smaller than -1.986086 (the t-table value). This indicates that a decline in the SDG index in previous periods negatively affects the current SDG index. At lag (-3), the coefficient is -0.169643 with a t-statistic of -1.31314, which is lower than the critical value, indicating an insignificant relationship.

For the Green Bond variable, the results indicate a significant positive effect at lags (-1), (-2), and (-3), with coefficients of 0.618210, 0.497177, and 0.398723, and t-statistics of 2.81659, 2.85686, and 3.25166, respectively, all surpassing the critical t-value of 1.986086. These findings suggest that increased green bond issuance in previous periods significantly enhances the current SDG index. However, at lag (-4), the coefficient is 0.007700 with a t-statistic of 1.10652, which is below the critical value, signifying no significant relationship.

The policy interest rate variable shows no significant impact on the SDG index in the short term. Across all lags from (-1) to (-4), the t-statistics remain below the critical t-value (1.986086), with coefficients such as -0.016535 at lag (-1) and -0.023913 at lag (-4), suggesting that policy interest rate changes do not significantly influence the SDG index.

In contrast, Foreign Direct Investment demonstrates a consistently significant positive correlation with the SDG index across all lags. The coefficients at lags (-1), (-2), (-3), and (-4) are 0.064331, 0.046663, 0.031148, and 0.016005, respectively, with t-statistics of 3.01594, 2.63465, 2.40679, and 2.14984, all exceeding the critical t-value (1.986086). This consistent positive relationship highlights that FDI inflows continue to positively impact the SDG index, contributing to sustainable development in countries like Indonesia, Malaysia, the Philippines, and Thailand.

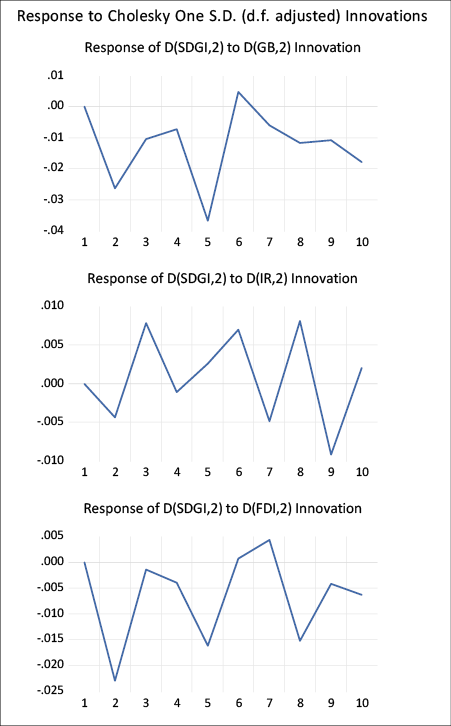

To further analyze the dynamics and causal relationships among the variables, the Impulse Response Function (IRF) is employed, focusing on the SDG index as the dependent variable. The IRF explores how the SDG index responds over time to shocks in the independent variables, including green bond issuances, policy interest rates, and foreign direct investment (FDI). This analysis provides deeper insights into the short- and medium-term effects of these shocks, complementing the PVECM results and enhancing our understanding of their impact on sustainable development outcomes.

Figure 2 illustrates the extent to which the SDG index responds to shocks from the variables Green Bond, Policy Interest Rate, and Foreign Direct Investment (FDI). Initially, shocks from these variables do not impact the SDG index. However, the SDG index begins to respond in subsequent periods. From the 2nd to the 5th period, shocks from the Green Bond variable have a negative effect on the SDG index, but this effect reverses in the 6th period, becoming positive. However, in the following periods, from the 7th to the 10th, the negative relationship begins to fade, although it has not yet turned positive.

Figure 2

Impulse Response Function (IRF) Test Results

To enhance the reliability of the Impulse Response Function (IRF) analysis, a 95% confidence interval was incorporated. This confidence interval provides a statistical boundary within which the true impulse responses are expected to fall, allowing for a more robust interpretation of the results. It ensures that the conclusions drawn regarding the impact of shocks on the SDG index are statistically supported rather than solely based on point estimates.

This dynamic indicates that the implementation of green bonds takes time to have a significant impact on sustainable development. This is supported by Bhutta et al. (2022) and Bisultanova (2023), who state that Green Bonds provide funding for green projects with long investment cycles, such as renewable energy infrastructure, water management, and sustainable transportation. These projects require time to demonstrate tangible results on sustainable development indicators. On the other hand, research by Nguyen et al. (2023) highlights that the issuance of Green Bonds in Southeast Asian developing countries faces challenges, such as credit risk parity with conventional bonds, the diversion of attention from sustainability issues due to the COVID-19 pandemic, and uncertainties in regulations and green commitment standards, which hinder the further growth of the Green Bond market. Therefore, green bonds require robust regulatory support and time to realize their full impact on the SDGs.

Shocks arising from the Policy Interest Rate variable are relatively volatile across periods. In the 2nd period, shocks from the policy interest rate have a negative impact on the SDG index, followed by a positive impact in the 3rd period. Up to the 10th period, the shocks from the policy interest rate alternate between positive and negative. This occurs because policy interest rates do not have a direct impact on the SDG index but are influenced by various other factors. The fluctuations in the impulse response function (IRF) reflect how sustainable development responds to interest rate shocks within a complex economic dynamic. These responses are not always consistent, as they are tied to both direct and indirect effects of other variables.

In the context of sustainable development, Aguila and Wullweber (2024) explain that policy interest rates can influence investments in the green sector, but their impact is often indirect and requires fiscal policy support to enhance their effectiveness. Additionally, Chen (2024) adds that short-term interest rate uncertainty leads to a rapid decline in investments, including in the renewable energy sector. Hence, the response of the SDG index to interest rate shocks is volatile, reflecting how interest rate changes can either encourage or hinder investment depending on the accompanying economic conditions.

The Foreign Direct Investment (FDI) variable tends to deliver shocks with negative impacts on the SDG index. From the 2nd to the 5th period, the SDG index responds to negative shocks from FDI. However, in the 6th and 7th periods, FDI shocks positively affect the SDG index, although the subsequent periods return to negative impacts. The fluctuating impacts of FDI shocks on the SDG index reflect their complex nature. These fluctuations indicate that the benefits of FDI depend on the investment orientation and the regulations implemented by the recipient country.

Research by Jorgenson et al. (2022) finds that FDI tends to increase CO2 emissions, which can hinder the achievement of sustainable development goals, as FDI often transfers energy-inefficient and environmentally damaging production processes to recipient countries. In contrast, other findings by Demena and Afesorgbor (2020) show the opposite, indicating that FDI can reduce CO2 emissions.

Additionally, findings by Phung et al. (2023) further assert that FDI positively impacts green growth in Southeast Asian economies, particularly with high fiscal development that supports investment in renewable energy or sustainable infrastructure. Therefore, a regulatory framework is needed to ensure that foreign investments are directed toward sectors relevant to achieving the SDGs. Without proper management, FDI risks cause greater negative impacts on the environment and long-term welfare.

4.2 Discussion

This study explores how green bonds, policy interest rates, and foreign direct investment (FDI) influence the achievement of Sustainable Development Goals (SDGs) in four emerging ASEAN nations: Indonesia, Malaysia, the Philippines, and Thailand. The results suggest that all three factors green bonds, interest rates, and FDI contribute to advancing sustainable development, as shown by both their short-term and long-term effects on the SDGs index. The findings highlight that green bonds have a notable and meaningful impact on the SDGs index in both time frames. Over the long term, the positive coefficient associated with green bonds indicates that increasing their issuance significantly supports SDG progress. Green bonds serve as an essential tool for governments and private organizations to raise capital for initiatives that align with SDG goals, including efforts to cut carbon emissions, enhance energy efficiency, and promote the expansion of renewable energy. Economically, the mobilization of green finance channels resources toward low-carbon technologies and infrastructure, which contributes directly to SDG targets related to affordable clean energy (SDG 7), climate action (SDG 13), and sustainable cities (SDG 11).

Prior studies support these findings. Research by Lee (2020), Versal and Sholoiko (2022), and Rasoulinezhad and Taghizadeh-Hesary (2022) confirms that green bonds contribute to reducing carbon emissions and increasing renewable energy production. Functioning both as a financing instrument and a catalyst for the green economic transition, green bonds play a strategic role in advancing sustainable development. Furthermore, green bonds mitigate climate risks amidst economic and environmental policy uncertainties, as highlighted by Mohammed et al. (2024).

In the short run, green bonds maintain a positive and notable effect on the SDGs index, showcasing their capacity to draw international investors eager to finance sustainable initiatives soon after they are issued. The short-term positive impact reflects investor confidence and the immediate liquidity infusion into environmentally beneficial projects, which begins the transition to longer-term developmental outcomes. Flammer (2019) observed that green bonds have gained popularity among investors due to their innovative nature in supporting low-carbon projects. However, their significance diminishes at Lag 4, reflecting the need for additional support to sustain their impact on the SDGs index. Tolliver et al. (2019) noted that such support could come from governments and investors to maintain the strategic role of green bonds in achieving SDGs.

FDI also exerts a positive and significant impact on the SDGs index in both the short and long term. In the short term, FDI contributes to SDG achievement by creating direct employment, raising local income, and improving access to economic resources. The positive coefficient of FDI underscores that increased inflows of foreign capital significantly enhance SDG progress through mechanisms such as technology and knowledge transfer, human capital development, and fostering economic inclusivity. By linking foreign investors with local enterprises, FDI strengthens domestic economic capacity and promotes inclusive, sustainable development. In particular, FDI supports industrial diversification and upgrades production technologies, which are critical for achieving SDG 8 (Decent Work and Economic Growth) and SDG 9 (Industry, Innovation, and Infrastructure).

Over the long term, FDI impact becomes more structural and enduring. One major contribution of FDI lies in the transfer of advanced technologies, including clean technologies critical for climate change mitigation. Parab et al. (2020) emphasized the causal link between renewable energy consumption and FDI, which supports sustainable development. However, Zhang et al. (2023) cautioned that FDI could negatively affect environmental quality if not implemented strategically. Conversely, Demena and Afesorgbor (2020) highlighted that directing FDI toward renewable energy infrastructure significantly reduces environmental emissions. Such allocations improve energy efficiency and yield substantial environmental benefits. Research by Sarkodie and Strezov (2019) further found that FDI accelerates the adoption of clean technologies in developing countries, contingent on regulatory quality and investment orientation. Strengthening human capital also facilitates adoption of cleaner and more environmentally friendly technologies reducing CO2 emissions. Therefore, strategic policies that channel FDI into renewable energy sectors are essential to support sustainable development.

Policy interest rates exhibit a negative but insignificant influence on the SDGs index in both the short and long term, suggesting a tendency for higher interest rates to correlate with a decline in SDG performance. This aligns with studies by Desalegn et al. (2022) and Aguila and Wullweber (2024), which found that rising interest rates increase borrowing costs, reducing investor profitability and discouraging green investments. From an economic perspective, tighter monetary conditions restrict access to capital for sustainability-linked projects, thereby slowing progress in sectors such as clean energy, infrastructure, education, and healthcare, which are crucial for multiple SDG achievements. While variables like green bonds and FDI show more direct contributions to sustainable projects, the role of policy interest rates remains relatively weak. A tight monetary policy can limit green sector investments, but its effects are not significant enough to directly impact SDG achievement. Ferrando and Mulier (2022) emphasized that high interest rates raise borrowing costs, restricting investments in infrastructure, healthcare, education, and employment — all crucial sectors for sustainable development. Alafif (2023) added that higher interest rates could reduce access to credit for businesses and households, lowering consumer spending and hindering SDG progress, particularly in poverty alleviation and quality-of-life improvements.

In conclusion, this study underscores the pivotal role of green bonds and FDI in achieving sustainable development goals in ASEAN developing countries. Green bonds serve as an effective financial mechanism for funding green projects, while FDI provides tangible economic benefits that drive progress. However, managing policy interest rates requires careful consideration to ensure that monetary policies do not impede SDG attainment. The policy implications of these findings include the need to expand green bond issuance, enhance regulations to attract FDI in strategic sectors, and integrate monetary policy with sustainable development strategies.

5. Conclussion

This study investigates how green bonds, interest rate policies, and foreign direct investment (FDI) contribute to the attainment of Sustainable Development Goals (SDGs) in four developing ASEAN countries Indonesia, Malaysia, the Philippines, and Thailand over the 2018–2023 period. Using the Panel Vector Error Correction Model (PVECM), the findings show that these factors each play an influential role in supporting SDG achievement, both in the short and long term.

Specifically, green bonds have demonstrated a significant and positive influence on the progression toward SDGs. As a financial tool geared toward environmental sustainability, green bonds effectively fund projects that promote renewable energy and green infrastructure, aligning closely with the objectives of sustainable development. However, the observed variability in green bond issuance underscores the necessity for more cohesive policies to bolster both domestic and international investment interest.

Second, interest rate policies influence SDGs indirectly by creating a more conducive environment for investment, particularly green investments. Lower interest rates have been shown to reduce funding costs and encourage capital allocation to sustainable sectors, although their effectiveness depends on regulations ensuring that these funds are directed toward projects supporting sustainability.

Third, FDI plays a key role in supporting SDGs through technology transfer, job creation, and enhancing local resource capacity. However, the impact of FDI is highly dependent on the target sectors for investment. If directed toward unsustainable sectors, FDI may lead to environmental degradation and hinder the achievement of SDGs. The interaction between green bonds, interest rate policies, and FDI shows a synergistic relationship. Supportive interest rate policies and a strong green bond market can attract more FDI to the sustainable sector, while well-targeted FDI can accelerate the development of green technologies and strengthen the green bond ecosystem.

This study also supports the Ecological Modernization Theory (EMT), which emphasizes the importance of technological modernization and institutional reforms in achieving sustainability. The study further asserts that policy integration, strict regulatory oversight, and careful investment strategies are crucial to maximizing the role of green bonds, interest rate policies, and FDI in supporting the achievement of SDGs in ASEAN developing countries.

As a policy implication, the governments of ASEAN developing countries need to develop a more mature green financial market ecosystem, one of which is by promoting green bond issuance through fiscal incentives such as tax reductions and subsidies. Regulations ensuring transparency and accountability in green bond issuance must also be strengthened to attract both domestic and international investors. Monetary policies should aim to maintain economic stability while simultaneously encouraging green investments, for example, by facilitating low-interest financing for environmentally friendly projects. Additionally, FDI regulations may be adjusted to support sectors that contribute to a low-carbon economy, such as renewable energy and energy-efficient industries. Taken together, these policy measures can enhance the effectiveness of green finance and foreign investment in supporting progress toward sustainable development goals, while acknowledging the inherent trade-offs between economic growth and environmental sustainability.

6. Study Limitations and Suggestions for Future Research

While this study offers valuable insights into the role of green financial instruments, monetary policy, and foreign direct investment (FDI) in promoting sustainable development within emerging ASEAN countries, several limitations should be acknowledged.

First, the SDG Index used as the dependent variable is an aggregate measure that combines 17 different goals, potentially masking the heterogeneous effects that financial variables may have on specific dimensions of sustainable development. Future research should consider disaggregating the SDG indicators to capture the nuanced impacts on individual goals, such as climate action (SDG 13) or industry innovation (SDG 9).

Second, due to data availability constraints, the study focuses only on four ASEAN countries (Indonesia, Malaysia, the Philippines, and Thailand) over the 2018–2023 period. Although these countries represent major economies within the ASEAN bloc, including all ASEAN member states and expanding the time span could enhance the robustness and generalizability of future findings.

Third, the transformation of the annual SDG Index data into quarterly frequency through linear interpolation may introduce smoothing biases. Future studies are encouraged to employ more sophisticated interpolation techniques or utilize quarterly proxies for sustainable development progress to minimize measurement errors.

Fourth, the study applied second-order differencing to achieve stationarity for all variables. While necessary for model validity, this transformation may have reduced the economic interpretability of the long-term relationships. Future research could explore alternative models that accommodate mixed integration orders without requiring excessive differencing, such as ARDL or dynamic panel techniques like PMG (Pooled Mean Group).

Finally, although the PVECM model captures short- and long-term dynamics effectively, future research could incorporate additional structural factors such as governance quality, regulatory stringency, and environmental policies to better understand the mechanisms through which financial instruments influence sustainable development outcomes.

References

Aguila, N., & Wullweber, J. (2024). Greener and cheaper: Green monetary policy in the era of inflation and high interest rates. Eurasian Economic Review, 14(1), 39–60. https://doi.org/10.1007/s40822-024-00266-y

Ahmed, R., Yusuf, F., & Ishaque, M. (2024). Green bonds as a bridge to the UN sustainable development goals on environment: A climate change empirical investigation. International Journal of Finance and Economics, 29(2), 2428–2451. https://doi.org/10.1002/ijfe.2787

Alafif, H. A. (2023). Interest Rate and Some of Its Applications. Journal of Applied Mathematics and Physics, 11(06), 1557–1569. https://doi.org/10.4236/jamp.2023.116102

Alamgir, M., & Cheng, M. C. (2023). Do Green Bonds Play a Role in Achieving Sustainability? Sustainability (Switzerland), 15(13). https://doi.org/10.3390/su151310177

Aust, V., Morais, A. I., & Pinto, I. (2020). How does foreign direct investment contribute to Sustainable Development Goals? Evidence from African countries. Journal of Cleaner Production, 245. https://doi.org/10.1016/j.jclepro.2019.118823

Azam, M., Ftiti, Z., Hunjra, A. I., Louhichi, W., & Verhoeven, P. (2022). Do market-supporting institutions promote sustainable development? Evidence from developing economies. Economic Modelling, 116(September 2021), 106023. https://doi.org/10.1016/j.econmod.2022.106023

Azhgaliyeva, D., Kapoor, A., & Liu, Y. (2020). Green bonds for financing renewable energy and energy efficiency in South-East Asia: a review of policies. Journal of Sustainable Finance and Investment, 10(2), 113–140. https://doi.org/10.1080/20430795.2019.1704160

Belke, A. H., & Göcke, M. (2019). Interest Rate Hysteresis in Macroeconomic Investment Under Uncertainty. SSRN Electronic Journal, 801. https://doi.org/10.2139/ssrn.3445832

Bhutta, U. S., Tariq, A., Farrukh, M., Raza, A., & Iqbal, M. K. (2022). Green bonds for sustainable development: Review of literature on development and impact of green bonds. Technological Forecasting and Social Change, 175(August 2021), 121378. https://doi.org/10.1016/j.techfore.2021.121378

Bisultanova, A. (2023). Green bonds: historical aspects of implementation. E3S Web of Conferences, 458. https://doi.org/10.1051/e3sconf/202345805013

Borowski, P. F., & Patuk, I. (2021). Environmental, social and economic factors in sustainable development with food, energy and eco-space aspect security. Present Environment and Sustainable Development, 15(1), 153–169. https://doi.org/10.15551/pesd2021151012

Chen, B., & Andrews, S. H. (2008). An Empirical Review of Methods for Temporal Distribution and Interpolation in the National Accounts. Economic Analysis, May, 31–37.

Chen, Y. (2024). The impact of interest rate uncertainty on renewable energy investments: Compared with conventional energy investments. Applied and Computational Engineering, 60(1), 76–82. https://doi.org/10.54254/2755-2721/60/20240840

Chuba, M. A., & Yusuf, L. D. (2022). Monetary Policy and Sustainable Development Goals in Nigeria. International Journal of Advanced Economics, 4(6), 107–115. https://doi.org/10.51594/ijae.v4i6.360

Demena, B. A., & Afesorgbor, S. K. (2020). The effect of FDI on environmental emissions: Evidence from a meta-analysis. Energy Policy, 138(xxxx), 111192. https://doi.org/10.1016/j.enpol.2019.111192

Desalegn, G., Fekete-Farkas, M., & Tangl, A. (2022). The Effect of Monetary Policy and Private Investment on Green Finance: Evidence from Hungary. Journal of Risk and Financial Management, 15(3). https://doi.org/10.3390/jrfm15030117

Dhahri, S., & Omri, A. (2020). Foreign capital towards SDGs 1 & 2 Ending Poverty and hunger: The role of agricultural production. Structural Change and Economic Dynamics, 53, 208–221. https://doi.org/10.1016/j.strueco.2020.02.004

Diaz-Sarachaga, J. M., Jato-Espino, D., & Castro-Fresno, D. (2018). Is the Sustainable Development Goals (SDG) index an adequate framework to measure the progress of the 2030 Agenda? Sustainable Development, 26(6), 663–671. https://doi.org/10.1002/sd.1735

Ferrando, A., & Mulier, K. (2022). The real effects of credit constraints: Evidence from discouraged borrowers. Journal of Corporate Finance, 73, 102171. https://doi.org/10.1016/j.jcorpfin.2022.102171

Flammer, C. (2020). Green Bonds: Effectiveness and Implications for Public Policy. Environmental and Energy Policy and the Economy (1). https://doi. org/10.1086/706794

Friedman, M. (1962). The Interpolation of Time Series by Related Series. Journal of the American Statistical Association, 57(300), 729. https://doi.org/10.2307/2281805

Holzhacker, R., & Agussalim, D. (2019). Political Ecology in the Asia Pacific Region (Vol. 1).

Jorgenson, A., Clark, R., Kentor, J., & Rieger, A. (2022). Networks, stocks, and climate change: A new approach to the study of foreign investment and the environment. Energy Research and Social Science, 87(October 2021), 102461. https://doi.org/10.1016/j.erss.2021.102461

Kwilinski, A., Lyulyov, O., & Pimonenko, T. (2023). Spillover Effects of Green Finance on Attaining Sustainable Development: Spatial Durbin Model. Computation, 11(10). https://doi.org/10.3390/computation11100199

Lee, J. W. (2020). Green finance and sustainable development goals: The case of China. Journal of Asian Finance, Economics and Business, 7(7), 577–586. https://doi.org/10.13106/jafeb.2020.vol7.no7.577

Mahmood, A., Farooq, A., Akbar, H., Ghani, H. U., & Gheewala, S. H. (2023). An Integrated Approach to Analyze the Progress of Developing Economies in Asia toward the Sustainable Development Goals. Sustainability (Switzerland), 15(18). https://doi.org/10.3390/su151813645

Mei, J. C. (2023). Foreign direct investment and relative capacity: Theory and evidence. Economics of Transition and Institutional Change, 31(4), 1175–1214. https://doi.org/10.1111/ecot.12369

Mohammed, K. S., Serret, V., & Urom, C. (2024). The effect of green bonds on climate risk amid economic and environmental policy uncertainties. Finance Research Letters, 62(PA), 105099. https://doi.org/10.1016/j.frl.2024.105099

Mol, A. P. J., Spaargaren, G., & Sonnenfeld, D. A. (2013). Ecological modernization theory: Taking stock, moving forward. In Routledge International Handbook of Social and Environmental Change (pp. 15–30). https://doi.org/10.4324/9780203814550

Mun, H. W., Hook, L. S., Kun, S. S., Mazlan, N. S., & Ahmad, M. N. N. (2023). Does Government and Institution Quality Matter To Sustainable Development Goals? Journal of Sustainability Science and Management, 18(1), 181–197. https://doi.org/10.46754/jssm.2023.01.011

Nguyen, A. H., Hoang, T. G., Nguyen, D. T., Nguyen, L. Q. T., & Doan, D. T. (2023). The Development of Green Bond in Developing Countries: Insights from Southeast Asia Market Participants. European Journal of Development Research, 35(1), 196–218. https://doi.org/10.1057/s41287-022-00515-3

Parab, N., Naik, R., & Reddy, Y. V. (2020). Renewable energy, foreign direct investment and sustainable development: An empirical evidence. International Journal of Energy Economics and Policy, 10(5), 479–484. https://doi.org/10.32479/ijeep.10206

Phung, T. Q., Rasoulinezhad, E., & Luong Thi Thu, H. (2023). How are FDI and green recovery related in Southeast Asian economies? Economic Change and Restructuring, 56(6), 3735–3755. https://doi.org/10.1007/s10644-022-09398-0

Rasoulinezhad, E., & Taghizadeh-Hesary, F. (2022). Role of green finance in improving energy efficiency and renewable energy development. Energy Efficiency, 15(2). https://doi.org/10.1007/s12053-022-10021-4

Ronaldo, R., & Suryanto, T. (2022). Green finance and sustainability development goals in Indonesian Fund Village. Resources Policy, 78(June), 102839. https://doi.org/10.1016/j.resourpol.2022.102839

Sadiq, M., Ngo, T. Q., Pantamee, A. A., Khudoykulov, K., Thi Ngan, T., & Tan, L. P. (2023). The role of environmental social and governance in achieving sustainable development goals: Evidence from ASEAN countries. Economic Research-Ekonomska Istrazivanja , 36(1), 170–190. https://doi.org/10.1080/1331677X.2022.2072357

Sarkodie, S. A., & Strezov, V. (2019). Effect of foreign direct investments, economic development and energy consumption on greenhouse gas emissions in developing countries. Science of the Total Environment, 646, 862–871. https://doi.org/10.1016/j.scitotenv.2018.07.365

Singh, A. K., & Kumar, S. (2022). Exploring the Impact of Sustainable Development on Social-economic, and Science and Technological Development in Selected Countries. Society & Sustainability, 4(1), 55–83. https://doi.org/10.38157/ss.v4i1.405

Singhania, M., & Saini, N. (2021). Demystifying pollution haven hypothesis: Role of FDI. Journal of Business Research, 123(February 2019), 516–528. https://doi.org/10.1016/j.jbusres.2020.10.007

Sinha, A., Mishra, S., Sharif, A., & Yarovaya, L. (2021). Does green financing help to improve environmental & social responsibility? Designing SDG framework through advanced quantile modelling. Journal of Environmental Management, 292(February), 112751. https://doi.org/10.1016/j.jenvman.2021.112751

Tolliver, C., Keeley, A. R., & Managi, S. (2019). Green bonds for the Paris agreement and sustainable development goals. Environmental Research Letters, 14(6). https://doi.org/10.1088/1748-9326/ab1118

Venâncio, A., & Pinto, I. (2020). Type of entrepreneurial activity and sustainable development goals. Sustainability (Switzerland), 12(22), 1–25. https://doi.org/10.3390/su12229368

Versal, N., & Sholoiko, A. (2022). Green bonds of supranational financial institutions: On the road to sustainable development. Investment Management and Financial Innovations, 19(1), 91–105. https://doi.org/10.21511/imfi.19(1).2022.07

Xiong, Y., & Dai, L. (2023). Does green finance investment impact on sustainable development: Role of technological innovation and renewable energy. Renewable Energy, 214(June 2022), 342–349. https://doi.org/10.1016/j.renene.2023.06.002

Ye, X., & Rasoulinezhad, E. (2023). Assessment of impacts of green bonds on renewable energy utilization efficiency. Renewable Energy, 202(November 2022), 626–633. https://doi.org/10.1016/j.renene.2022.11.124

Younis, F., & Chaudhary, M. A. (2020). Sustainable Development: Economic, Social, and Environmental Sustainability in Asian Economies. Forman Journal of Economic Studies, 15, 87–114. https://doi.org/10.32368/fjes.2019150

Yousaf, U., Naqvi, F. N., Nasir, A., Bhutta, N. A., & Haider, A. (2020). Impact of foreign direct investment on economic growth of Pakistan. European Journal of Economics, Finance and Administrative Sciences, 02(32), 95–100. https://doi.org/10.18535/ijsrm/v9i08.em03

Zhang, Z., Zhao, Y., Cai, H., & Ajaz, T. (2023). Influence of renewable energy infrastructure, Chinese outward FDI, and technical efficiency on ecological sustainability in belt and road node economies. Renewable Energy, 205(December 2022), 608–616. https://doi.org/10.1016/j.renene.2023.01.060

Zhao, L., Chau, K. Y., Tran, T. K., Sadiq, M., Xuyen, N. T. M., & Phan, T. T. H. (2022). Enhancing green economic recovery through green bonds financing and energy efficiency investments. Economic Analysis and Policy, 76, 488–501. https://doi.org/10.1016/j.eap.2022.08.019